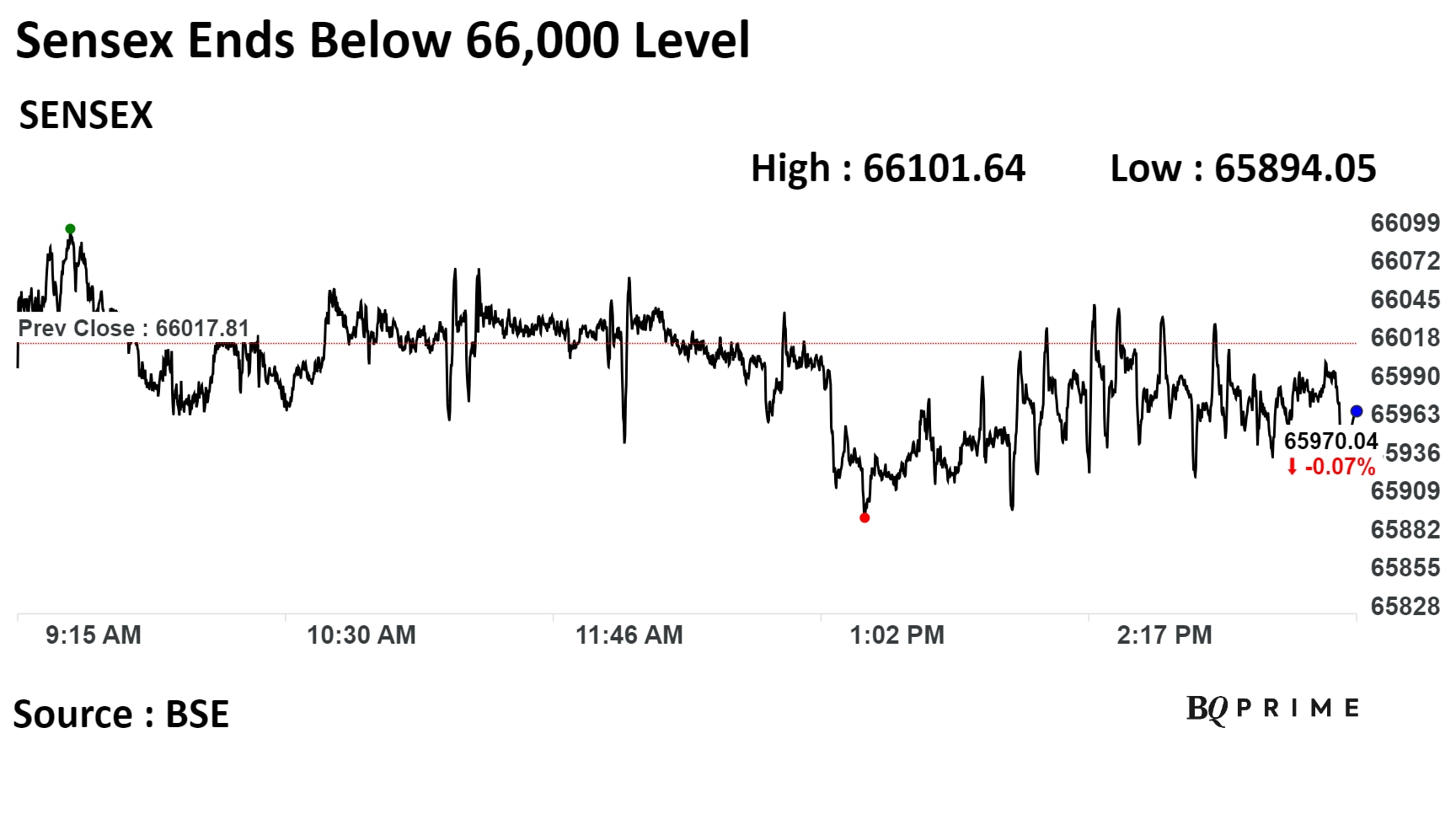

India's benchmark stock indices ended lower for the second consecutive day on Friday, led by losses in Tata Consultancy Service Ltd., Infosys Ltd., and ITC Ltd.

However, on a weekly basis, the headline indices gained for the fourth week, the longest stretch of gains since July 21.

Pharma and healthcare sectors advanced, but information technology was under pressure.

The S&P BSE Sensex closed 48 points, or 0.07%, lower at 65,970.04, while the NSE Nifty 50 fell 7 points, or 0.04%, to end at 19,794.70.

There could be some bout of volatility from current levels with respect to the monthly expiry next week, according to Vikas Jain, senior research analyst at Reliance Securities.

The Nifty reached a peak of 19,875 last week, creating an immediate hurdle, according to Mandar Bhojane, equity research analyst at Choice Broking.

"A crossover is deemed necessary for a fresh upward movement. On the hourly chart, the 19,600–19,550 range is identified as the immediate support zone. Traders are advised to maintain long positions with a stop loss at this level," he said.

Global Markets

European shares wavered after the latest economic data highlighted Germany's struggle to recover from an energy-induced downturn last winter and the mounting impact of higher borrowing costs.

The Stoxx Europe 600 index was little changed at the open, holding onto a modest weekly gain. Hong Kong and mainland Chinese equities dropped, reversing Thursday's rally, inspired by Beijing's widening property rescue campaign. Japanese stocks rose in catch-up play after a national holiday, while those in Australia also gained. U.S. equity futures were steady.

The U.S. markets will open for half a day for Friday.

HDFC Bank Ltd., ICICI Bank Ltd., Axis Bank Ltd., Adani Enterprises Ltd., and Cipla Ltd. positively contributed to the Nifty.

Tata Consultancy Services Ltd., Infosys Ltd., ITC Ltd., HCL Technologies Ltd., and Bajaj Finance Ltd. weighed on the index.

The Sensex rose 0.27% and the Nifty was higher by 0.32% this week. Last week, the Sensex rose 1.56% and the Nifty advanced by 1.72%.

The dominant trend in the market this year is the huge outperformance of the mid and small caps, according to VK Vijayakumar, chief investment strategist at Geojit Financial Services. "While Nifty is up only 8.82% year-to-date, the Nifty midcap index and Nifty Smallcap index are up 33.38% and 41.66% year-to-date."

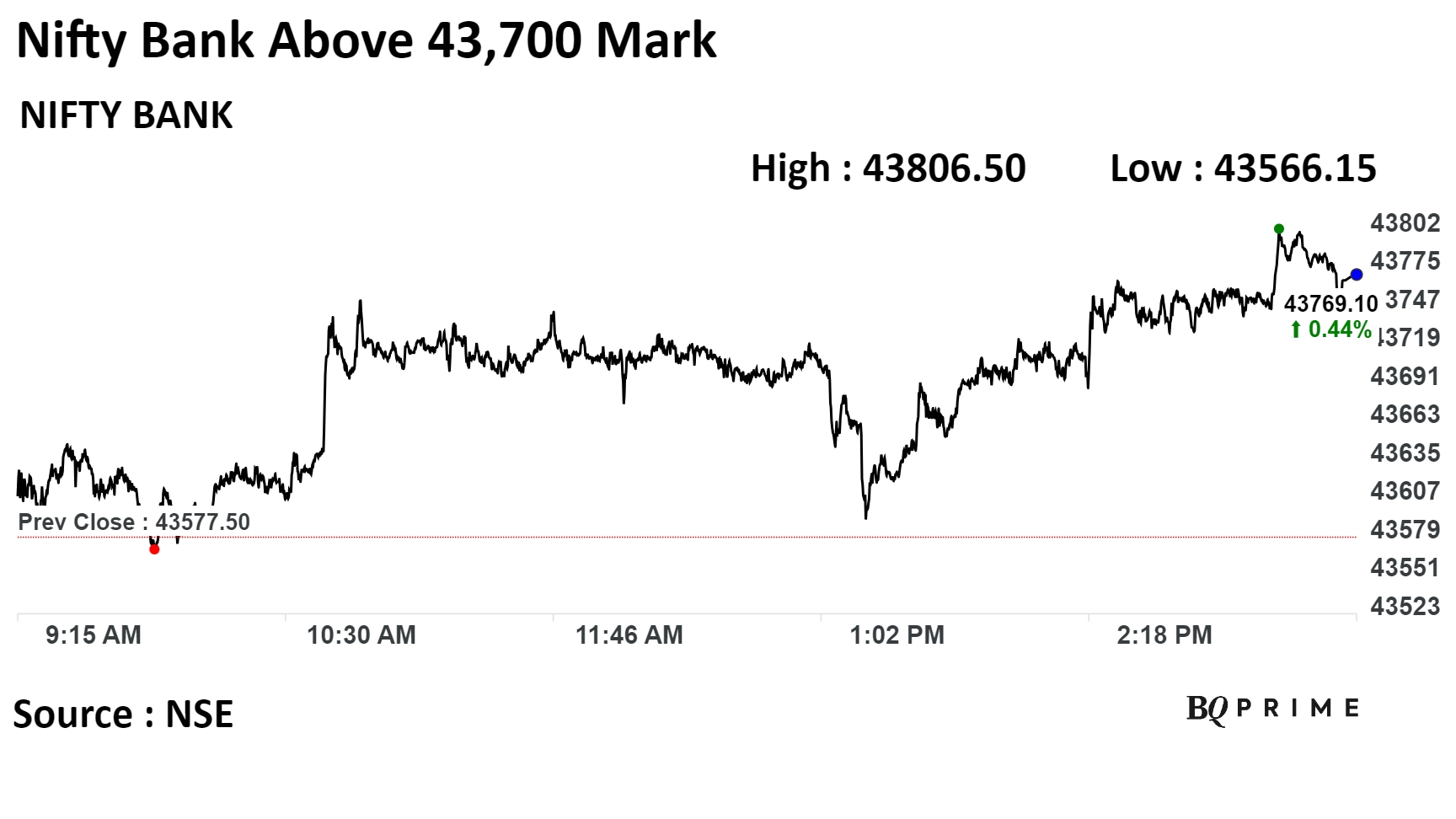

"It is important to understand that the Nifty is depressed by the poor performance of banks, which have the largest weightage in the Nifty. The Nifty Bank index is almost flat this year, with measly growth of 0.87%," Vijayakumar said.

The broader markets outperformed their larger peers. The BSE Midcap ended up 0.13%, while the SmallCap closed 0.14% higher.

Twelve out of the 20 sectors compiled by BSE Ltd. advanced, while eight sectors declined. BSE IT fell the most, while Capital Goods rose the most.

The market breadth was split between buyers and sellers. About 1,805 stocks rose, 1,872 stocks declined, and 137 remained unchanged on the BSE.

Banks are underperforming despite very good results because they are overowned, and sustained FII selling is weighing on bank stocks. Mid- and small-cap stocks are under-owned, and retail exuberance is largely driving these stocks. There is no valuation comfort in the broader market, but valuations are fair in large caps, according to Vijayakumar.

"Therefore, the next leg of the rally, driven by institutional money, both foreign and domestic, will be driven by large caps," he said.

Most sectors advanced this week, with Nifty Realty Index gaining over 1%, followed by Nifty Metal. Nifty IT has fallen the most this week.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.