(Bloomberg Opinion) -- In the community of professional money managers, no one is more vilified than Cathie Wood, who runs the $6.81 billion ARK Innovation ETF, which focuses on the technology sector. Her detractors criticize Wood for making big calls — the price of Bitcoin will reach $1 million by 2030, and by then autonomous vehicle sales will bring in around $10 trillion, for example — without the research to back them up. Her ETF's jaw-dropping gain of about 150% in 2020? That was more due to circumstance than skill, they say.

Regardless, Wood has started to make big, contrarian calls on the economy in addition to her musings on technology, giving her critics even more fodder. One of her more controversial statements came in June, when she said that rather than inflation, “the greater risk by far is deflation.” And on Wednesday, she sent a series of tweets saying the Federal Reserve is making a “serious mistake” with its monetary policy.

You can quibble with Wood's views on inflation, but she's onto something with the Fed. Central to her thesis is the yield curve, as represented by the gap between two- and 10-year Treasury yields. Normally upward sloping, the curve has inverted, with yields on longer-term notes falling below those of shorter-term notes. This is an ominous sign for the economy, as every recession since the 1950s has been preceded by an inverted yield curve.

What's concerning to Wood is that the curve is not just inverted, but the inversion is the deepest since the early 1980s at around 80 basis points, or 0.8 percentage point. “I'm wondering why economists are not highlighting that an 80bp inversion of the Treasury yield curve is much more a red flag for the Fed today than it was in the early '80s,” Wood tweeted. She went on to explain that the inversion represents about 23% of the current 3.5% yield on the benchmark 10-year Treasury note, compared with about 5% of the prevailing yields of the early 1980s.

It's true that central bank officials and Chair Jerome Powell are relatively sanguine about the economic outlook, expressing optimism that they can steer the economy to a so-called soft landing, raising interest rates to levels needed to get inflation under control without inflicting broader damage. But that almost never happens. As longtime economist Gary Shilling has noted, in the last 14 periods when policymakers tightened credit, a recession has followed 13 times.

Some market participants, and probably Fed officials as well, are downplaying the yield curve. They say the Fed's purchases of trillions of dollars of bonds over the last decade through a policy known as quantitative easing and now its unwinding of those holdings via quantitative tightening has distorted the message being sent by the yield curve.

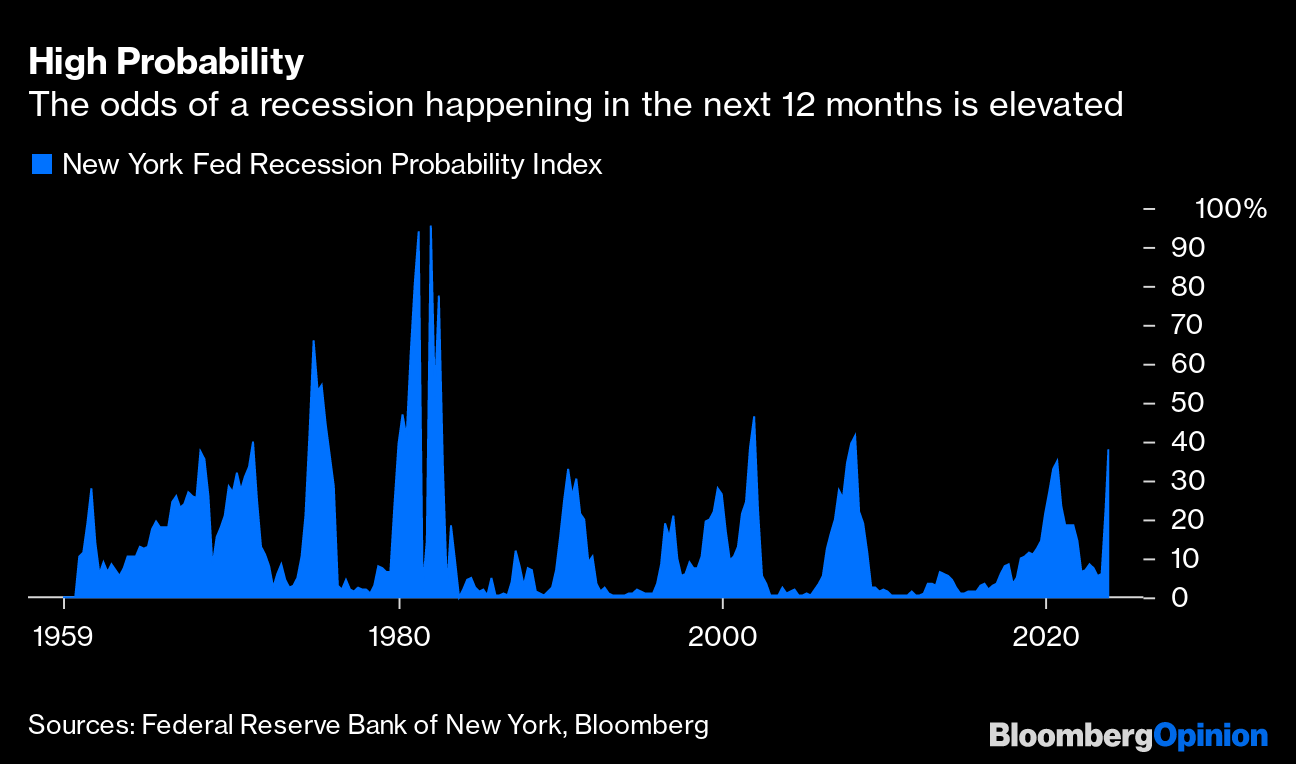

Indeed, the Federal Reserve Bank of New York's recession probability model, which uses the yield curve as the primary input, is giving 38% odds of a recession in the next 12 months. Put another way, there's a 62% chance that the economy avoids a downturn.

To be sure, this shouldn't be reassuring. DataTrek Research wrote in a report to clients that in all but two of the nine recessions since 1960, a 30% probability of a contraction signified that a downturn was either already underway or would come in the next 12 months. And with the Fed signaling it expects to continue to raise short-term rates, the yield curve inversion is likely to get even deeper. So, in reality, 38% odds of a recession are really almost 100%, according to DataTrek. Wood's critics have the upper hand these days. After those big gains in 2020, her ETF is down by more than 70% since its peak. An ETF designed to take the opposite side of Wood's bet — the AXS Short Innovation Daily ETF — has doubled since debuting in November 2021. But if Wood can position her fund to benefit from the “serious mistake” she says the Fed is making, she may soon have the upper hand again.

More From Bloomberg Opinion:

- Service Wages Keep Bedeviling Powell and Markets: Jonathan Levin

- Be Careful, Here Come the Predictions for 2023: John Authers

- What the Yield Curve Says About the Next Recession: Aaron Brown

Want more Bloomberg Opinion? {OPIN }. Or you can subscribe to our daily newsletter.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is the executive editor of Bloomberg Opinion. Previously, he was the global executive editor in charge of financial markets for Bloomberg News.

More stories like this are available on bloomberg.com/opinion

©2022 Bloomberg L.P.

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.