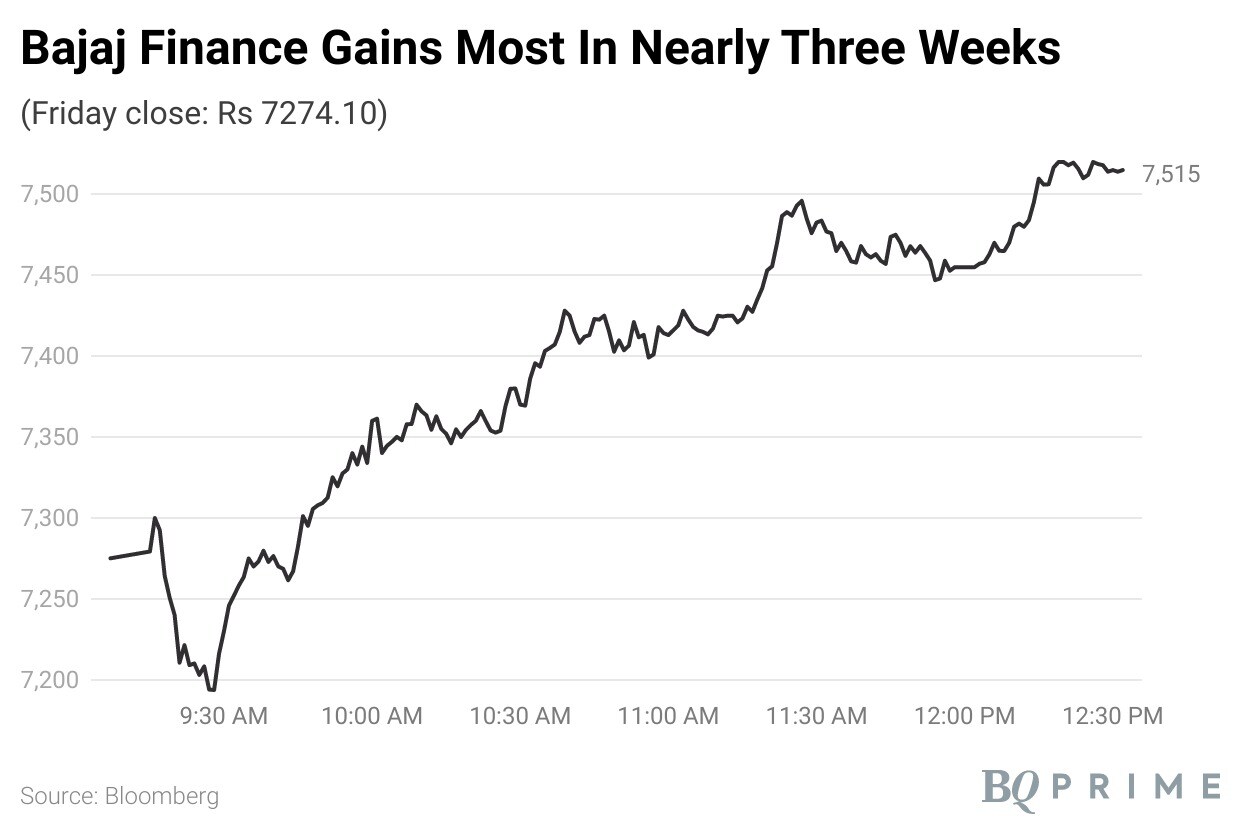

Shares of Bajaj Finance Ltd. rose the most in nearly three weeks as Jefferies expects higher growth realisation if the Reserve Bank of India approves in-house card programme, making it the first non-banking financial company to launch a credit card in India.

The brokerage, in a note dated Sept. 18, said this would enable Bajaj Finance to take product to deeper markets as against the top 100 towns where it sells cards of RBL Bank Ltd. and DBS Bank Ltd. and where majority of players operate.

"India has around 8 crore credit cards and is much less penetrated than larger markets," the brokerage said. "If Bajaj Finance gets approval to foray here, it would be able to leverage its network of over 3,500 branches, 1,40,000 merchant relationships and 6 crore customers to ramp-up," it said

Jefferies said if the company achieves 20-40% cross-sell to non-delinquent client base of 4 crore and even at lower transaction values, it could make Rs 900-1,700 crore in profit in three years. This is 5-10% of FY25 profit and would add growth drivers."

Despite this, the brokerage maintained its "hold" rating, saying that the prospective growth will "support its premium valuations." However, it raised the company's price target to Rs 8,000, from the earlier Rs 7,300.

"An in-house credit card programme can expand opportunity set to deeper markets where Bajaj Finance is already present," Jefferies said. "Credit card market would add new leg of profit pool and deepen client engagement."

"The current credit card partnerships for Bajaj Finance are primarily sourcing arrangements and it doesn't get upsides from growth in transactions and revolver/EMI products," it said.

It also raised earnings marginally and sees 28% annualised profit over FY23-25, with FY23 seen growing faster due to low base.

Shares of the company gained as much as 3.1%, the most since Aug. 30. Of the 31 analysts tracking the company, 20 maintain 'buy', six suggest 'hold' and five recommend 'sell'. The return potential of the stock is 2.3%.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.