Scan to Download

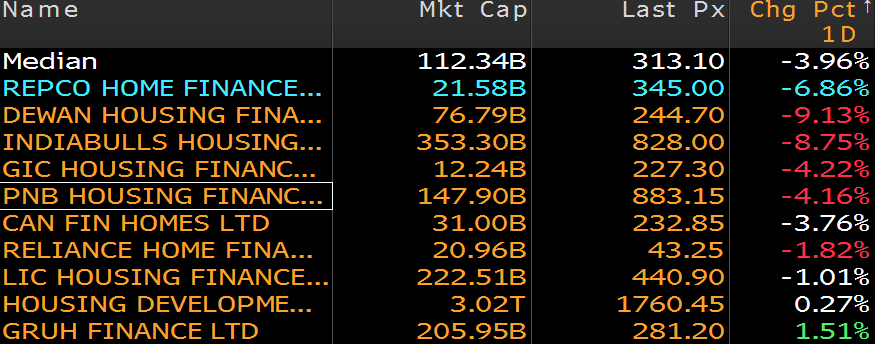

Indiabulls Housing Finance Tumbles On Exposure To Default-Rated SuperTech

Buyers and sellers were not immediately known

Source: Bloomberg

Shares of the Noida-based IT services company swung between gains and losses after it reported July-September quarter earnings.

Key earnings highlights:

Shares of the Mumbai-based non-banking mortgage lender fell as much as 13.26 percent, the most since Sept. 25, to Rs 787 on heavy volumes.

Trading volume was three times its 20-day average, data compiled by Bloomberg showed.

As many as 95 lakh shares changed hands on the National Stock Exchange, according to information on the National Stock Exchange.

Shares of the country's largest two-wheeler maker swung after its profit met Bloomberg consensus in September quarter.

Key earnings highlights:

Buyers and sellers were not immediately known

Source: Bloomberg

Shares of the Coimbatore-based industrial machinery maker rose as much as 8.2 percent, the most in over seven months, to Rs 6,290.

Lakshmi Machine Works informed exchanges that its board will meet on Oct. 22 to consider buy back of equity shares.

Shares of the Mumbai-based private sector lender slumped as much as 8.2 percent to Rs 228.50 underperforming S&P BSE Sensex's 0.6 percent gain.

Trading volume was 24 percent its 20-day average at this time of the day, data compiled by Bloomberg showed.

Shares of the Mumbai-based auto parts maker rose as much as 5.5 percent to Rs 272 after its profit jumped 74 percent to Rs 43 crore.

Key earnings highlights:

Shares of the Srinagar-based private sector lender rose as much as 18.5 percent to Rs 49.70 after its profit rose 31 percent to Rs 94 crore.

Key earnings highlights:

Q2 Results: Infosys Scores $2-Billion Large Deals, Margins Flat Despite Rupee Boost

The Mukesh Ambani-led oil-to-telecom conglomerate will report its July-September quarter earnings later in the day. Here’s what to expect from the company in second quarter of current financial year.

Estimates compiled by BloombergQuint

A sale of treasury bills and RBI's Rs 12,000 crore open market operation to buyback bonds will be in close focus in the sovereign debt market.

A series of positive news and data has helped yield on the 10-year bond to decline 20 basis points in the last five sessions. It fell 5 basis points on Tuesday to 7.87 percent. The positive momentum may continue, and the yield may stay in a range of 7.85-7.90 percent in the day.

In the currency market, rupee is set to gain further tracking gains in Asian equities. The closely-tracked South Korean won rose 0.3 percent against the dollar. Implied opening from forwards suggest the pair may open at around 73.3668 and trade in a range of 73.20-73.60 a dollar in the day.

BofAML

Nomura

CLSA

Macquarie

UBS

Credit Suisse

Morgan Stanley

CLSA

UBS

BofAML

Credit Suisse

Deutsche Bank Research

UBS

Kotak

CLSA

Macquarie

Goldman on Industrials

HSBC on Maruti Suzuki

(As reported on Oct. 16)

Mahindra CIE Automotive (Q3, YoY)

CRISIL (Q2, YoY)

Shakti Pumps (Q2, YoY)

Here are some key events coming up this week:

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.