Weak macros failed to dent markets’ enthusiasm, as November figures were expected to be on the weaker side, and with budget announcement expected in just a month, sentiment remained positive. However, with U.S. market back after holidays, global cues will have more weightage in the coming days especially with jobs data scheduled this week.”Anand James, Chief Market Strategist, Geojit BNP Paribas Financial Services

Infosys CEO says employees need to innovate and bring out their best to survive challenging times. https://t.co/1o12I9ytD0 pic.twitter.com/rHo4a2L9Sn

— BloombergQuint (@BloombergQuint) January 3, 2017

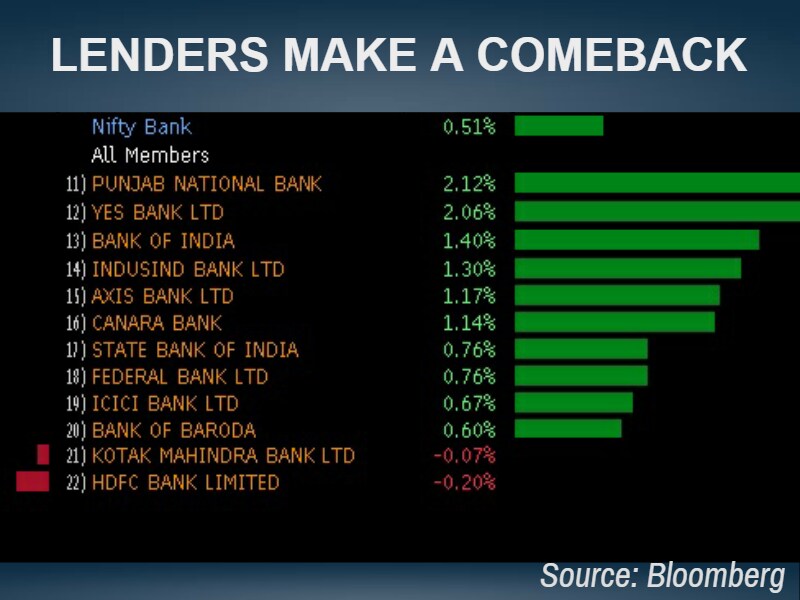

The Nifty Bank Index is under pressure. Where will it end today?

— BloombergQuint (@BloombergQuint) January 3, 2017

Must Read: How To Value The Bombay Stock Exchange?

#BQSpotted by @shraddha_babla | Donear Industries rallies 25 % in 5 days.https://t.co/q7ldKCejbO pic.twitter.com/E2PY1LBndU

— BloombergQuint (@BloombergQuint) January 3, 2017

First part of the Budget Session of Parliament may be held from January 31 to February 9. pic.twitter.com/cPEFv8iWd4

— BloombergQuint (@BloombergQuint) January 3, 2017

Read the full report HERE

GTN Industries: Extends Gains For Second Day

- Rallies as much as 17 percent today after gaining 19.85 percent yesterday

- Rises over 39 percent in two sessions

- Volumes at 7.6 times previous 20-day moving average

- Vertically integrated textile company; market cap of Rs 32 crore

Top Gainers

- Snowman Logistics (+5.7% to Rs 54.7)

- Transport Corporation of India (+6.5% to Rs 156)

- Patel Integrated Logistics (+6% to Rs 79)

- Gati Ltd. (+5.8% to Rs 123.5)

- Container Corp of India (+3% to Rs 1,175)

- VRL Logistics (+2.6% to Rs 265)

With inputs from PTI

#BQSpotted by @soumeet_sarkar | Gokaldas Exports is on a 6-day winning streak.https://t.co/HIb3dRqa1b pic.twitter.com/fUfmUFPx1Q

— BloombergQuint (@BloombergQuint) January 3, 2017

Movers & Shakers: Tata Motors, ICICI Bank, Hero MotoCorp And More

Foreign institutional investors are trading with caution in the futures & options markets, reports @AgamVakil. https://t.co/V6SMxRb3Ic pic.twitter.com/KPCgXdgUOa

— BloombergQuint (@BloombergQuint) January 3, 2017

How can ‘base rate’ borrowers switch to a lower home loan rate? https://t.co/VKQKpyvN3p

— BloombergQuint (@BloombergQuint) January 2, 2017

ICICI Bank joins a handful of other banks in offering cheaper loans, reports @alexandermats. https://t.co/HV0G7ey8uW pic.twitter.com/Er9I7knhJO

— BloombergQuint (@BloombergQuint) January 3, 2017

A Bloomberg survey shows that India's GDP grew at less than 7 percent compared to an early estimate from government advisors of as much as 7.75 percent. For bond bulls, the surprise good news is that the government has cut its FY17 borrowing by Rs 18,000 crore, which will help maintain the positive momentum and yields are bound to fall.

In currencies, the dollar has retreated from its New Year rally and Asians currencies like the won are trading stronger. The rupee, which declined in the last session could recover some lost ground today.

Reports on Sunday showed China’s official factory gauge stabilised near a post-2012 high while services remained robust, capping a year of steady improvement in both indicators. A private factory gauge released Tuesday also came in better than anticipated. Swaps contracts show expectations that the Federal Reserve will raise interest rates twice this year, after increasing them once in each of the past two years.

Back home, impact of the note ban seems to be weighing on industrial output with core sector growth decelerating to 4.9 percent in November 2016 as against 6.6 percent in the previous month. However, on an annual basis, the eight core sectors reported healthy growth over November 2015 figure of 0.6 percent.

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.