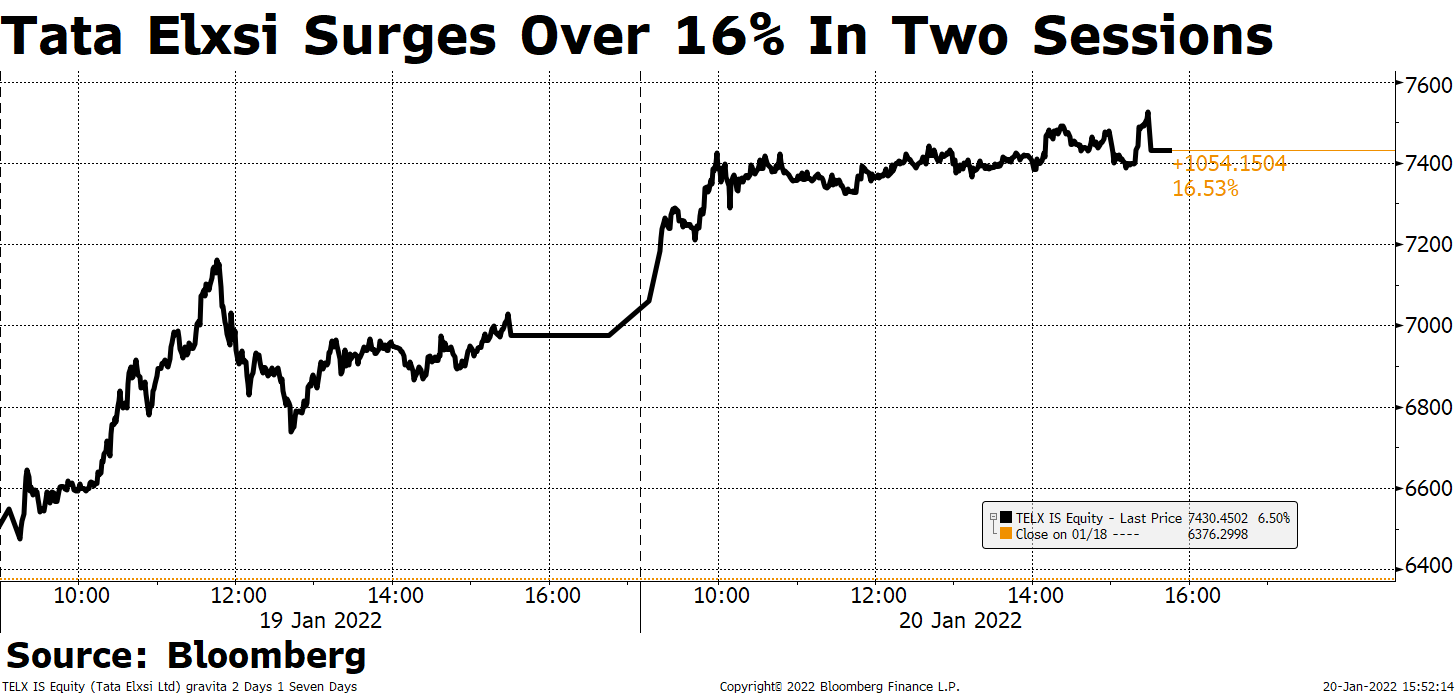

Shares of Tata Elxsi Ltd. surged for the second straight day as analysts raised target prices citing digital capabilities and deal wins after the design and technology services provider's third-quarter profit rose.

The stock jumped as much as 7.85% to Rs 7,525 apiece in intraday trade on Thursday and closed with 6.5% gains. It has risen 16.53% over the last two sessions.

The company reported a sequential rise in net profit and revenue in the quarter-ended December. Analysts cited presence in fast-growing verticals such as medical and healthcare businesses, strong digital engineering capabilities and strategic deal wins in embedded product design and digital projects as growth triggers.

Tata Elxsi's continued focus on emerging technologies would support revenue growth in the medium term, according to analysts at KR Choksey Research and Sharekhan.

The relative strength index on the stock is at 80, suggesting it may be overbought. Of the five analysts tracking the company, one maintains 'buy', one suggests 'hold', and three recommend 'sell', according to Bloomberg data. The average of 12-month target prices implies a downside of 27%.

KR Choksey Research

Reiterates 'accumulate' with the target price raised to Rs 7,504 from Rs 6,684; an implied return of 1.41%.

Quarterly performance was in-line with estimates and operating margin witnessed a sharp uptick.

Growth likely to be aided by digital and platform-led deals.

Higher offshoring, utilisation and operating leverage led to margin stability, despite an ongoing talent crunch.

Medical and healthcare businesses are experiencing traction and would likely have a multi-year tailwind.

Strategic deal-wins in EPD and design-led digital projects are likely to aid growth.

Expects strong deal momentum across verticals to continue.

Assigns P/E multiple of 82.4x to the FY24 estimated earnings per share.

Sharekhan

Retains 'buy', with the target price raised to Rs 8,160.

Presence in fast-growing verticals, superior margin profile, strong digital engineering capabilities and robust demand are key growth drivers.

Expects limited room for margin expansion in subsequent quarters.

Long-standing client relationships, rising focus on long-term deal contracts and huge addressable market augur well for the company's growth prospects.

Ebitda margin expansion in the December quarter was backed by rapid growth in medical devices vertical, high offshore, rising utilisation and quality of revenue mix.

Continued investments in emerging technologies have helped the company align itself to fulfill demand of global enterprises.

Focus on media, healthcare business and emerging technology areas are likely to aid revenue growth in the medium term.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.