(Bloomberg Opinion) -- When Richard Branson's Virgin Orbit Holdings Inc. filed for Chapter 11 bankruptcy earlier this month, the satellite-launch firm joined more than half a dozen businesses that went public during the “Everything Bubble” of 2020-2022 only to run out of money this year.

Once, hurrying to join the stock market by merging with a listed special purpose acquisition company seemed like a good way to raise heaps of cash and for insiders to get rich. But SPACs have become a poisoned chalice, above all for the retail investors who went along for the ride.

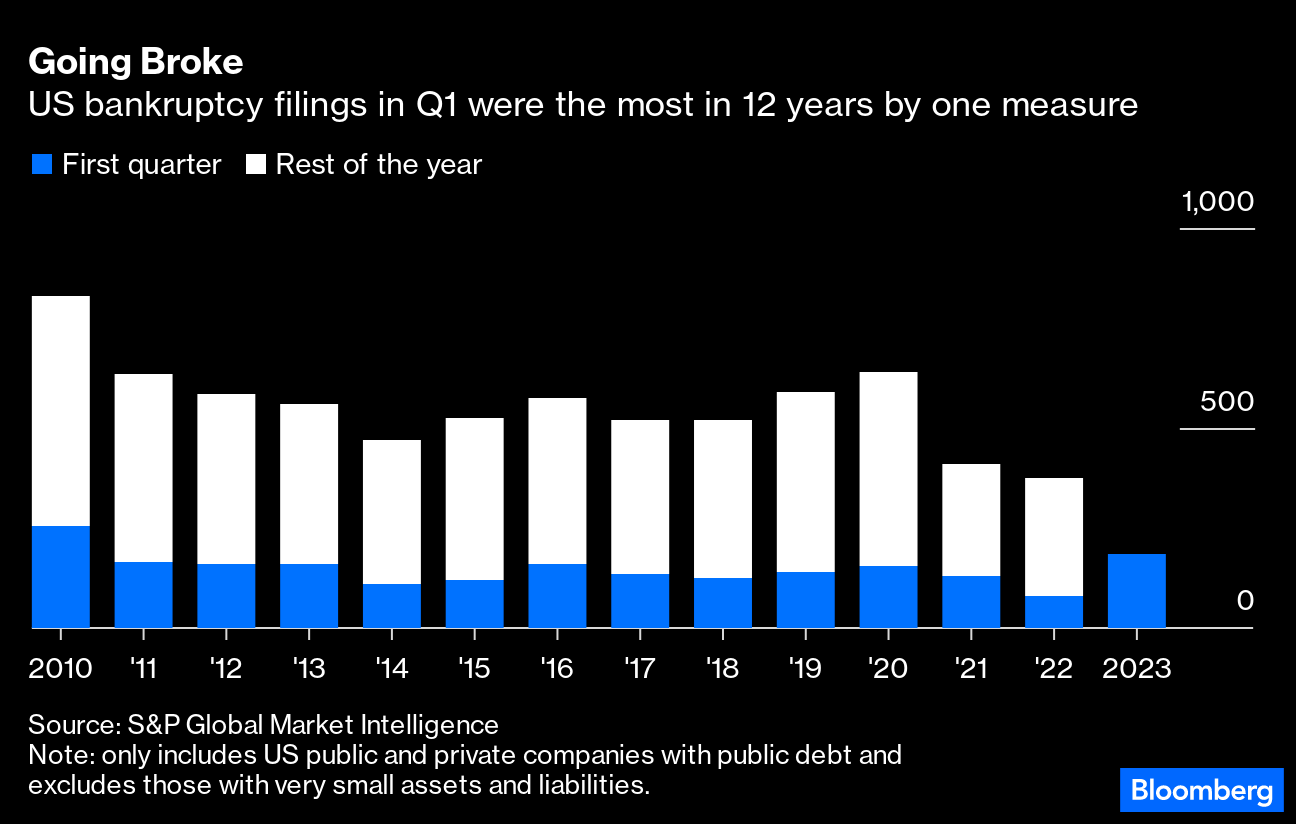

Ex-SPACs still standing are having to adopt a variety of ugly financial contortions to keep the lights on, including merging with a special purpose acquisition company .

For those unable to quickly become profitable or find a buyer, the path to salvation is narrow; external funding is often only available on very onerous terms, if at all.

Virgin Orbit won't be the last of its ilk to face a financial reckoning so it's worth considering what led to its downfall and that of other ex-SPACs.

A big reason why so many ex-SPACs faced financial problems is their listings didn't raise anywhere near the amount of capital that they needed. That's because shareholders exercised their right to ask for their money back, a process known as redemption.

Activities like space rockets, crypto mining and automotive tech are very capital intensive and early-stage companies can't easily borrow to plug a post-listing funding gap.

Quickly pivoting from pursuing growth to profitability is hard for speculative businesses with little revenue and can't be achieved just by cutting jobs (though many have tried that too).

Hot sectors like space and autonomous driving birthed multiple public companies, but intense competition was a further impediment to breaking even. Virgin Orbit had the misfortune to take on Elon Musk's better-capitalized and more experienced Space Exploration Technologies Corp. (aka SpaceX, which remains private).

Cash-strapped businesses are acutely vulnerable when misfortune strikes, as happened in January when Virgin Orbit's UK launch ended in failure, deterring potential rescuers and capital providers.

While a sale is often the best way to salvage value, finding a buyer can be tricky. A Boxed Inc. executive conceded in a bankruptcy filing that four months of efforts had failed to attract a single offer to purchases its retail e-commerce operations, which are now being wound down.(1) Internet service provider Starry Group Holdings Inc. contacted 79 parties prior to its bankruptcy but none submitted “actionable” bids. No wonder ex-SPACs have resorted to merging with one another.

The pain likely isn't over. “Going concern” warnings – a formal declaration that the company's cash reserves might not last another 12 months – have become worryingly common in SPAC-land and the shares of dozens of former SPACs have collapsed by more than 90%.

Many were egregiously overvalued and their revenue projections proved far too optimistic as they often failed to attract big institutional investors who might have been persuaded to back an additional equity offering. Being a little fish in a big pond is tough; UK companies still mulling listing in New York instead of London should remember that.

Low trading volumes and a low stock price limit the ability to raise money via at-the-market share offerings and equity lines of credit, which involves trickling new shares gradually into the market. The big US exchanges also threaten to delist companies with a stock price below $1.

A reverse stock split – when a large number of shares are exchanged for a much smaller number -- can remedy this problem by artificially boosting the stock price, but such announcements tend to create even more selling pressure.

Hence the pickle that businesses like Arrival SA find themselves in. Its shares have collapsed by 99% since a SPAC listing in 2021 valued the UK electric-van manufacturer at $13.5 billion. Last week, Arrival said it would seek to replenish its coffers by merging with yet another SPAC in a deal could that see current Arrival shareholders left with just 13% of the combined company. In February, Arrival also secured a deeply discounted equity injection and debt for equity swap from Antara Capital Master Fund LP, requiring the issuance of several hundred million new shares. A proposed 1-for-50 reverse stock split hasn't fooled investors about the massive dilution they're facing.

Arrival's Re-SPAC plan is similar to one being pursued by British connected vehicle-data company Wejo Group Ltd. Yet, Wejo's efforts to raise up to $100 million have already run into difficulties. Most of the shareholders of its second SPAC partner, TKB Critical Technologies I, asked for their money back in January, leaving just $57 million in the trust account. Wejo is in discussions with vendors about paying for services with its shares instead of cash and has warned it could run out of money as soon as this month unless it can obtain bridge financing.

Some former SPACs have been forced to take even more desperate measures. E-scooter-sharing company Helbiz changed its name to Micromobility.com Inc. last month to help revive the share price, which has declined 99% since 2021, valuing it at just $10 million. The new name hasn't stemmed the decline.

The company held less than $1 million of cash at the end of December and has warned of its ability to remain a going concern but has tried to attract retail investors by blaming nefarious short-sellers for its woes. Excessive dilution may be the bigger problem: Prior to a 1-for-50 reverse stock split in March, its share count had increased 17-fold in 12 months, chiefly as a result of securities it sold to Yorkville Advisors Global.

If you ask me, “Helbiz” is an apt name not just for this company but an entire universe of ailing SPACs.

More From Bloomberg Opinion:

- Another Crack at Chamath Palihapitiya's SPAC Letter: Ed Hammond

- SPAC Pipes Sometimes Leak: Matt Levine

- SPACs Slap Some Lipstick on Their Penny-Stock Pigs: Chris Bryant

(1) Boxed's Spresso software business continues and is being sold

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Bryant is a Bloomberg Opinion columnist covering industrial companies in Europe. Previously, he was a reporter for the Financial Times.

More stories like this are available on bloomberg.com/opinion

©2023 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.