(Bloomberg Opinion) -- Chances are if your cat or dog required veterinary care recently, you visited a practice owned by a private equity firm and got handed a big bill. Vets are now in the crosshairs of antitrust authorities, but pet owners shouldn't count on prices declining.

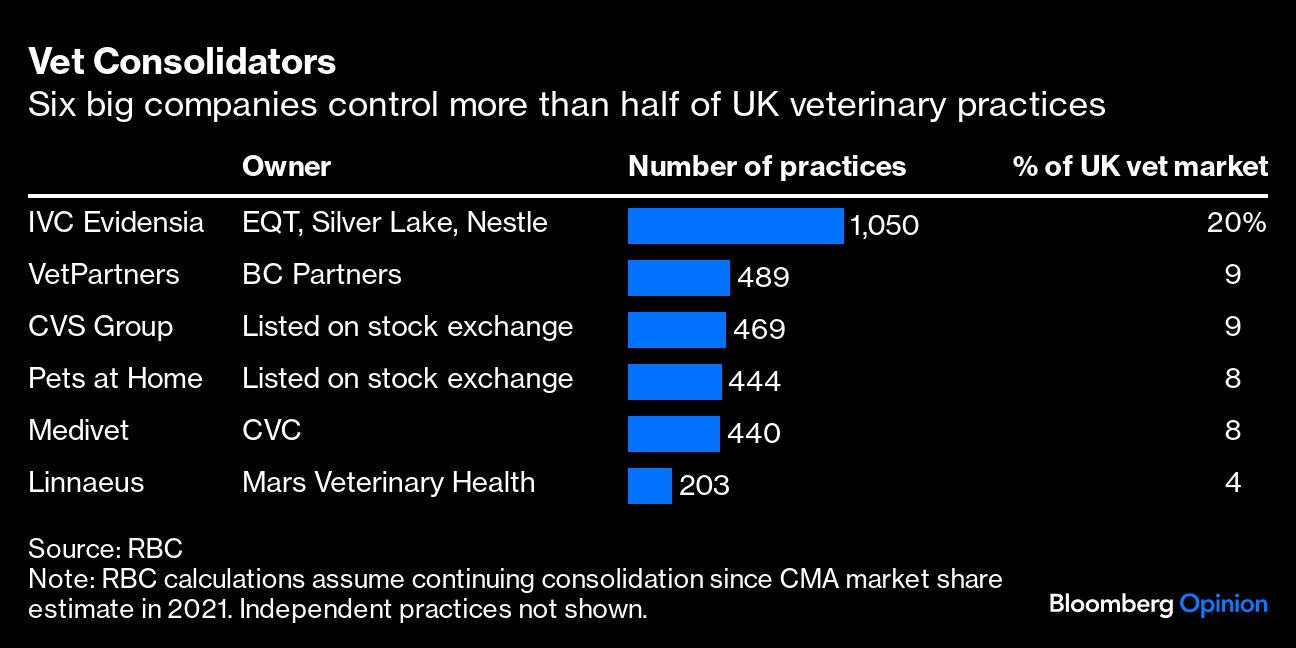

PE firms and corporate consolidators such as Mars Inc. have quietly “rolled up” individual veterinary clinics into massive international conglomerates with hundreds or even thousands of clinics. The proportion of independent UK vets, for example, shrank to around 45% in 2021 from 89% in 2013; six large chains currently control the bulk of the market.

In the US, where there have been $45 billion of deals in veterinary care since 2017, around 25% of vets are owned by big groups, notwithstanding laws prohibiting corporate ownership in some states.

Now, these serial acquirers have run into a regulatory wall. Amid concern that consolidation is pushing up prices, Britain's Competition and Markets Authority last month announced a sectoral review, driving shares in listed UK veterinary group CVS Group Plc down by around 25%. (CVS said its prices are “appropriate and reflect fair value.”)

In the US, private equity rollups — whether of vets, nursing homes or anesthesiologists — have become a big focus for Lina Khan's Federal Trade Commission. And in France, the country's highest administrative court in July ruled against corporate ownership of vets.

This backlash has coincided with the pet-care boom losing some of its bark amid the cost-of-living crisis and as PE-owned vets cope with higher interest rates.

There are several reasons why vets make such attractive targets for PE. Because people started spending more time at home during the pandemic, the proportion of pet-owning households is much higher than it was a decade ago.

Nowadays, people dote on their fur babies as they would on a family member — a trend the industry refers to as pet “humanization.” We're willing to spend more to ensure beloved animals receive the best treatment. “Spending on pets is generally the penultimate item people cut, second only to baby food,” notes the annual report of UK vet group Medivet, which is backed by CVC Capital Partners.

Pets are also living longer, meaning they may require treatment for chronic conditions such as diabetes. And because surgery can cost thousands of pounds, many pet owners now have insurance; when someone else is picking up the bill, customers are typically less price-sensitive.

IVC Evidensia, the UK's biggest vet group, was valued at €12.3 billion ($13 billion) in 2021, or an eye-watering 29 times the adjusted earnings before interest tax depreciation and amortization it generated that year. Backed by EQT Private Equity, IVC completed 284 acquisitions during its 2022 fiscal year and now has around 2,600 locations in 20 countries.

The CMA's review hasn't come out of the blue. The watchdog had already intervened on at least four occasions in the past two years to block or unwind veterinary takeovers amid growing transatlantic concern that corporate roll-ups curtail competition.

But regulators are playing catch-up: Britain has a voluntary merger-control system, meaning there's no obligation to notify the regulator about deals, while US transactions valued at less than $111 million don't have to be flagged to the FTC.

“Companies were going around buying up practices and these transactions weren't coming to the regulator's attention,” says Andrew Taylor, a partner at competition consultancy Aldwych Partners. “It's quite likely the CMA review will lead to a formal investigation and there's a risk that some firms will ultimately be asked to sell some of their practices.” In a note on CVS, Berenberg analysts said forced divestments were “extremely unlikely.”

It's not just the regulators who've may have been blindsided by PE's newfound enthusiasm for pet care. When big groups acquire a practice, they often keep the old practice name and branding, potentially leaving customers unaware of the change of control. IVC told the CMA this naming convention helps preserve the identity and culture of the practice. IVC “is open with customers when a practice joins our network” including by displaying posters and writing to them, a spokesperson told me.

I don't think PE ownership is bad per se: larger groups are better able to fund modern clinical equipment and drive harder bargains with drug companies. By centralizing finance, IT and administrative activities, vets and nurses should have more time to treat animals.

But if the nearest non-corporate clinic is miles away, customers can't shop around for a better deal. These conglomerates also tend to offer adjacent veterinary services such as diagnostic laboratories, crematoria and emergency care; the CMA is worried customers might be referred to a business owned by the same firm without them knowing. IVC said vets are not incentivized to sell treatments or refer within the group, pricing is determined by the local practice and vets have a duty to inform customers of any conflict of interest.

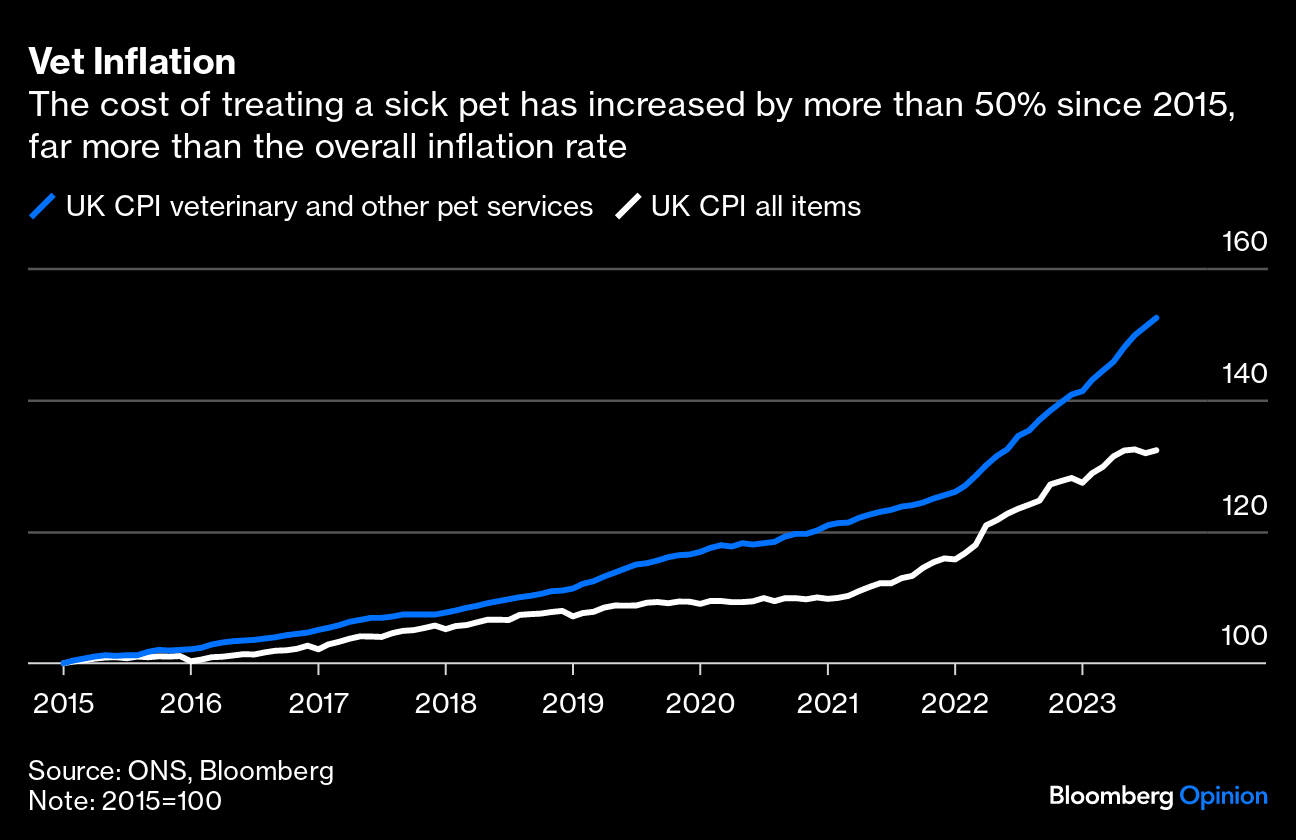

There's no doubt consolidation has coincided with soaring prices — UK veterinary services costs have increased more than 50% since 2015.

But that doesn't doesn't necessarily mean acquirers are overcharging. The costs of running a practice have also increased due to a global shortage of staff — a function of higher veterinary education costs, work-life balance issues and, in the UK at least, Brexit.

And if some corporate-owned veterinary practices are price gouging, so far it hasn't translated into sky-high profits. Ebitda margins across the UK veterinary sector sector are around 20%, which is hardly egregious. “We do not believe that the evidence supports a theory that CVS has taken advantage of its customers with consistent above-inflation prices increases,” Berenberg told clients last month.

IVC's ebitda margin declined to 18.6% from 21% last year, and like-for-like sales growth was just 6%, which it blamed in part on “economic pressures suppressing demand” — a sign perhaps that spending on pets is somewhat cyclical after all. The group is in the process of cutting hundreds of non-clinical staff and the cost of servicing its more than £4.5 billion of bank borrowings has increased.(1)

While IVC received an £800 million ($981 million) capital injection from its owners earlier this year, Standard & Poor's expects IVC to raise prices to offset rising costs, so customers may not see any relief. (2)

The results of the CMA's review won't be known for months, but I'd encourage vets to be more transparent about who owns them and any adjacent services they recommend. Antitrust officials should also demand more information from serial acquirers, as the FTC is pushing for, because that way consolidation won't go under the radar.

With large veterinary groups now looking to consolidate other international markets, more scrutiny can help ensure doting owners everywhere get a fairer deal for their pets.

More From Bloomberg Opinion On Our Furry Friends:

- Puppies and Rolexes Have Had It Tough Since Covid: Andrea Felsted

- Even Dogs and Cats Can't Escape Inflation: Andrea Felsted

- Did You Buy Your Dog a Christmas Present? Join the Club: Andrea Felsted

(1) IVC hedged 84% of its interest rate exposure following board approval in October 2022.

(2) IVC's owners have committed an additional £400 million of capital over the next two years.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Bryant is a Bloomberg Opinion columnist covering industrial companies in Europe. Previously, he was a reporter for the Financial Times.

More stories like this are available on bloomberg.com/opinion

©2023 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.