Traders who hung on during this year's tariff-fueled rollercoaster ride in stocks are facing a conundrum: Bonds may offer more attractive returns in coming years, according to one widely tracked measure.

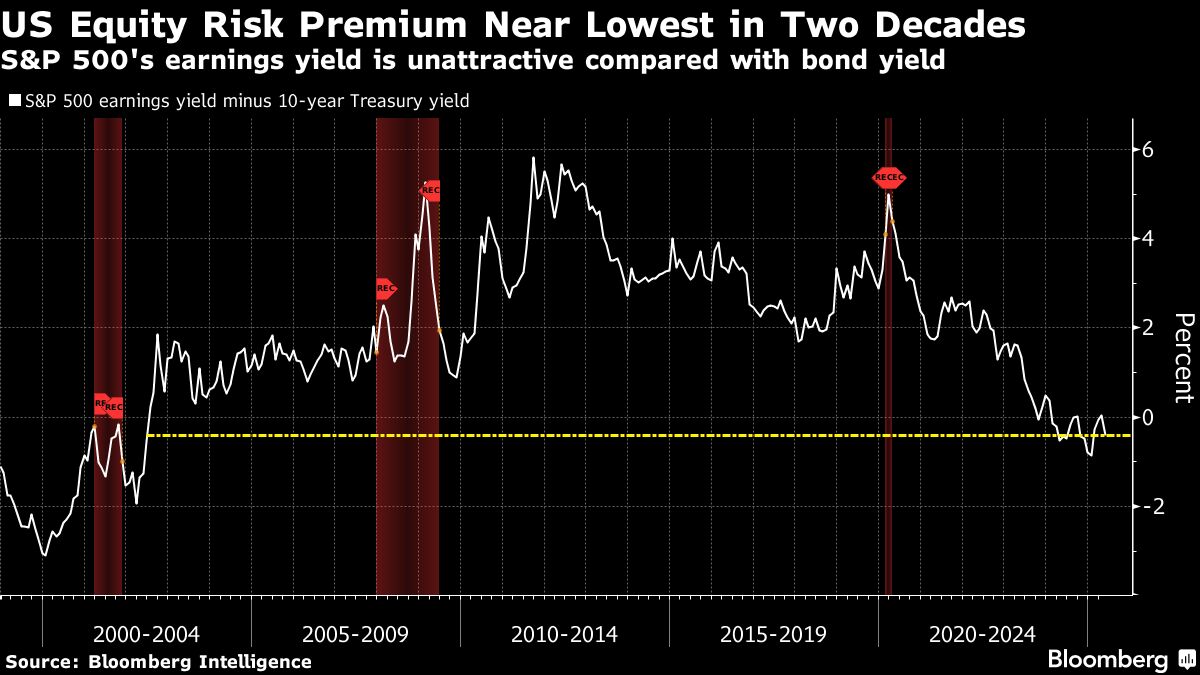

The equity risk premium, which investors use to determine the difference between expected returns on equities and US Treasuries, is hovering around its lowest point since 2002, data from Bloomberg Intelligence showed. That suggests stocks are more expensive relative to bonds than they have been for most of the last two decades, according to Bloomberg Intelligence strategists Gina Martin Adams and Michael Casper.

Calculated by subtracting the S&P 500 Index's earnings yield from the 10-year Treasuries rate, the gauge helps investors decide where to allocate their cash. The case for owning equities becomes less compelling if bonds can earn nearly as much as stocks but with reduced risk.

After the big recovery in stocks since April, the readout is fairly gloomy for equities: The S&P 500 has averaged a 12-month return of only 2.5% over the past three decades when the risk premium has stood around current levels, according to data compiled by investment research firm CFRA. That compares to an average annual return of 8.5% for the period.

“Whenever you see equity risk premium slump this much, it historically tells us that stocks are becoming less attractive,” said Timothy Chubb, chief investment officer at Girard, a wealth advisory firm backed by Univest. “After a massive rally over the past two months, this could take some air out of the recent rebound.”

With the S&P 500 within 2% of a record following a breathtaking surge from the edge of a bear market, investors are seeking fresh catalysts to justify buying stocks at current levels. While a brighter outlook on global trade, robust corporate earnings and resilient economic data have driven that rebound, those factors appear to be largely priced in.

That may be a reason for the comparatively listless trading in equities of late. The S&P 500 hasn't seen a move exceeding 0.6% in either direction for 10 of the last 11 sessions through Wednesday — the longest such stretch since early December, according to data compiled by Bloomberg.

“We know what the rules of the game are now for the trade war, and tariff optimism is no longer a floor for shares with things looking pricey again,” said Scott Ladner, chief investment officer at Horizon Investment.

Higher Yields

Meanwhile, Treasury yields stand near their highest levels in decades. Worries over US fiscal spending are expected to keep borrowing costs high for the foreseeable future, though several months of weaker-than-expected inflation have bolstered the case for the Federal Reserve to cut interest rates.

Not all periods with a negative or low equity risk premium have coincided with poor stock returns. The measure was negative for two long stretches in the post-World War II era, from October 1968 to October 1973, and from September 1980 to June 2002, BI data show. During the first stretch, stocks gained 1.1% annually, but they surged an annualized 10% in the latter.

At the same time, worries over the US fiscal position have dented the appeal of Treasuries, especially longer-dated maturities. DoubleLine Capital's Jeffrey Gundlach was the latest to sound a warning, saying on Wednesday that America's debt burden and interest expense have become “untenable” and could drive investors out of dollar-based assets.

Rich Valuations

Pricey stock valuations — including those of the so-called Magnificent Seven tech megacaps — are one key reason for the low equity risk premium.

Excluding the so-called Magnificent Seven stocks including Nvidia Corp., Microsoft Corp. and Meta Platforms Inc. brings the forward earnings yield up to 5.1%, from its current level of 3.62%, BI data shows. Still, that's just 0.7 percentage point above the 10-year yield.

“The outlook for stocks will ultimately be driven by trade and Fed policy in the coming months,” said Casper, of Bloomberg Intelligence. “The Fed will be a pivotal catalyst for any further upside ahead since monetary easing is historically good for equity gains. But investors need clarity.”

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.