Let's play a game.

If any of the following situations seems like a narration from your life, raise one hand. If two situations seem familiar, raise both hands and if all three are stories from your life, please stand up.

Situation 1

Your childhood memory of money-talk with your parents runs like this – “we belong to the middle class, education is everything to us. Money is important but never chase money. Too much money isn't good. It brings with it many problems and chances are, you may lose your human values or become evil, even.”

Situation 2

At a job interview, not your first, somewhere around your mid-life, you have been asked what motivates you and you say many things – your contribution to the firm, the learning curve, the sheer joy of being a part of an ace team etc., but not ‘money'. Money is important but it is not the main driver, not even among the top three – whoever says that!

Maybe, after ‘recognition', ‘respect', ‘pride', ‘satisfaction'...

Situation 3

You work in an industry connected with the financial services, or at least, make it a point to read a pink paper every day. If you are on social media, you follow ‘experts', know where the markets are at currently, engage in a tweet or two, but what about your own financial plan? You don't exactly know how much you need and how to get there, or if at all, you will get there. Your assets vis-à-vis your liabilities, a personal balance sheet perhaps? No?

If you meant to stand up, please don't. I would rather, you avoided the confusion at your workplace. You are only exhibiting qualities of the ‘scripted' Money-Avoider, and you my friend, are not alone.

Before we dive into who a money-avoider is, let us give credit where it is due. Two individuals, Bradley T Klontz and Sonya L Britt, have worked for several years in the field of financial psychology and given shape to what is today, popularly known as ‘money scripts' – little conversations in our head that are unconscious, often learnt in the childhood or even transgenerational.

It turns out, that each of us have a money avoider, a money status seeker, a money worshipper or a money vigilante hidden inside us. When either of the first three are more prominent, we have issues with money.

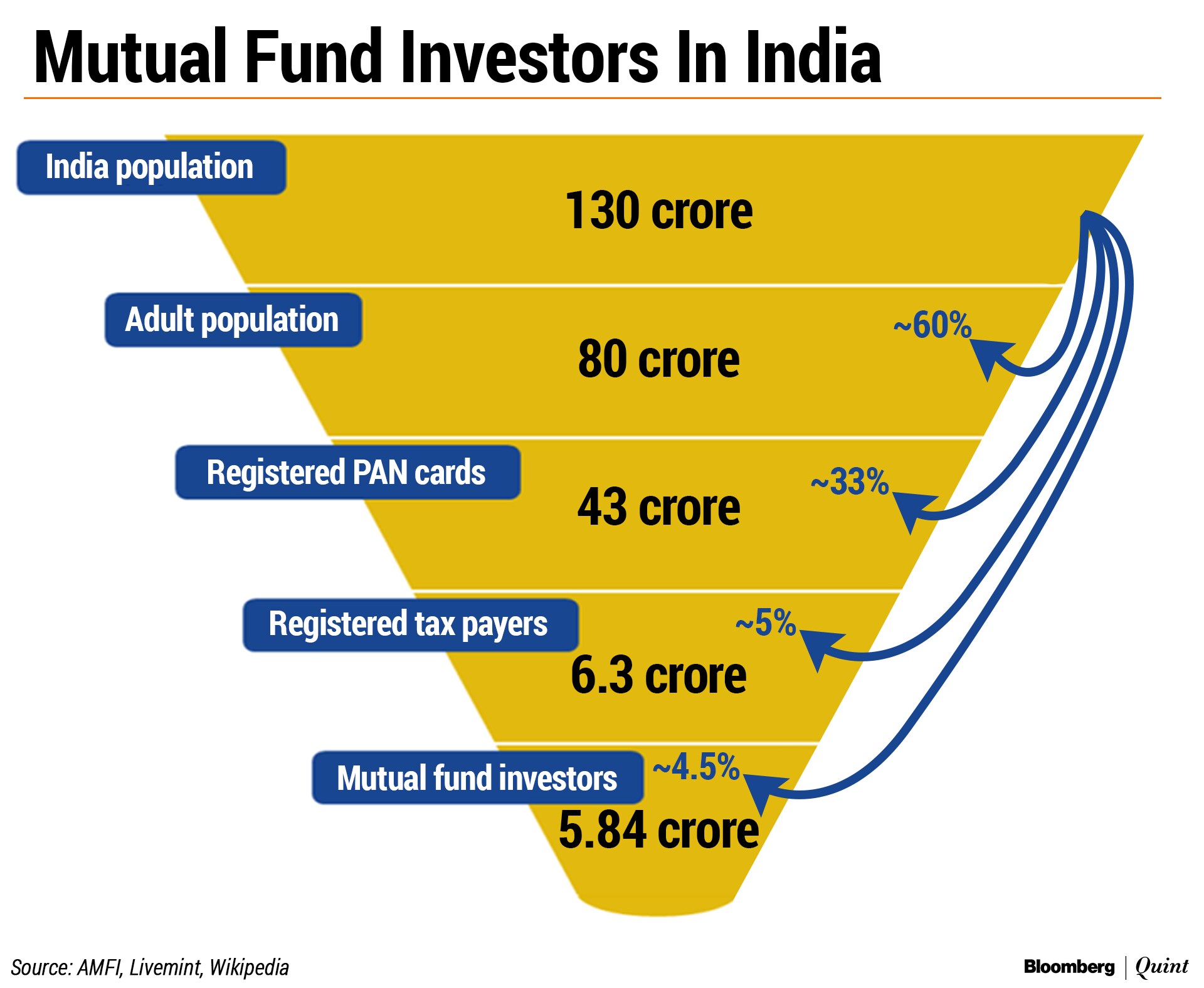

Now, what made me elaborate the script of the avoider in particular? We seem to be a nation of full of them. Don't believe me? Look the infographic below:

India is rich, they say. Even our invaders thought so. But only 4.5 percent of Indians are mutual fund investors.

As a generation, we are in a bit of a spot.

On the one hand, we have grown up learning that earning more or investing may not be a priority but we have just started seeing disposable incomes soaring. Now, we are spending more on goods whose prices are steadily going up (non-tradeable services like restaurant bills, hairstylist bills etc.) If you take interest in economic theory, you may want to read more about the Balassa Samuelson Effect.

Net net, we don't invest enough, we spend sufficiently and we don't wish to discuss this very much – our incomes will have to keep pace for this to have a happy ending.

No one debates the basic premise that money is required and that we don't have social security so, retirement has to be provided for. However, the number of investors are for all of us to see.

Is There A Way Out?

Is there a way out at all, from such a situation? For that, let us attempt to understand why we fail to invest in the first place.

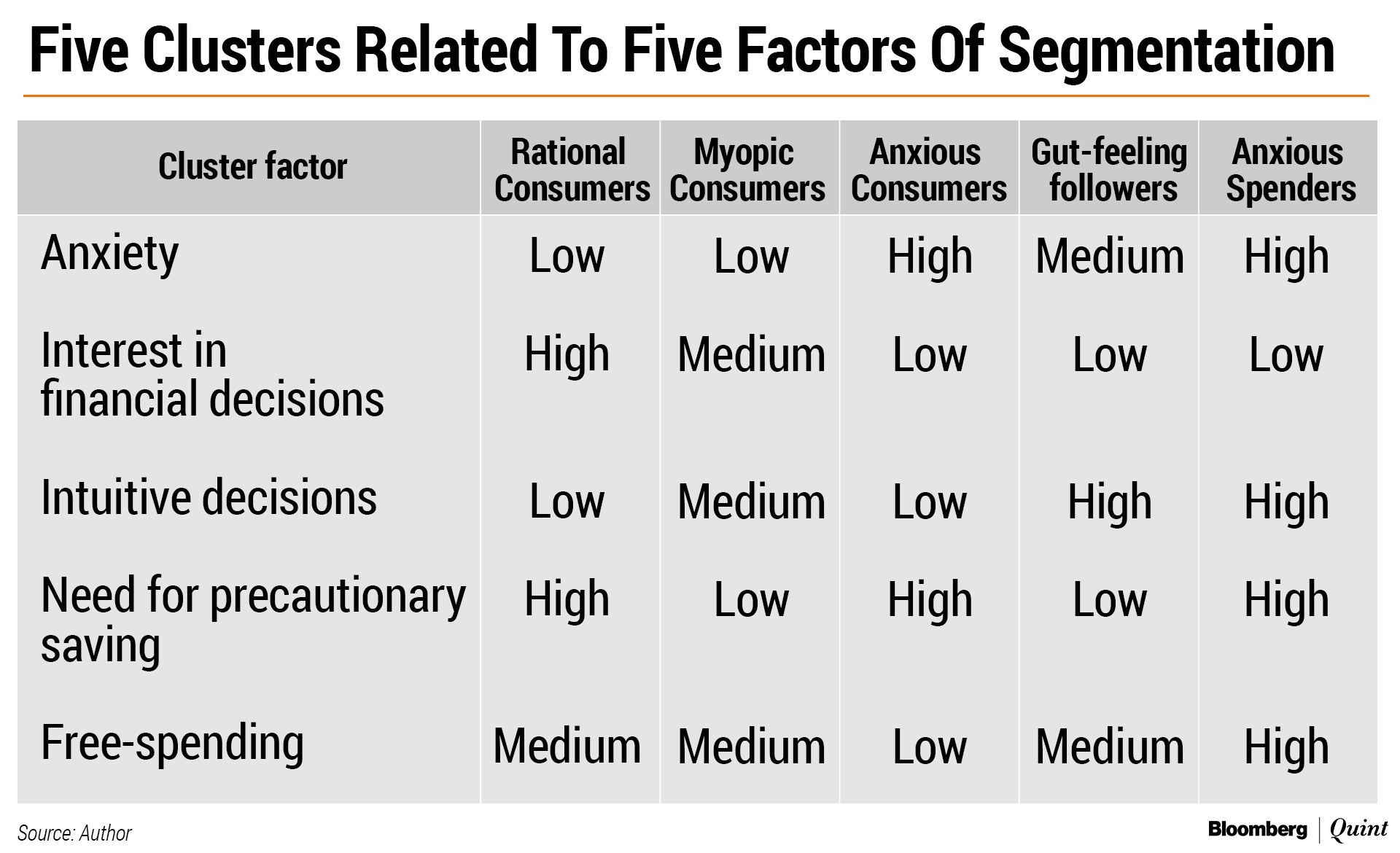

I teach a course called ‘Marketing of Financial Services', at Praxis Business School. When we discuss segmenting and targeting, we use the case of a certain financial services firm that takes a behavioural approach. I mention it here because this is completely connected to how people are wired and may even have answers on how to tackle our personality types.

So, the case leads to the following.

On the basis of the questionnaire that the firm makes participants fill up, people are categorised as per five behavioural dimensions –

- Anxiety,

- Interest in financial issues,

- Decision styles,

- Need for precautionary savings,

- Spending tendencies.

Once these five clusters of behaviour are put together, investor types emerge:

After this, students in the class reach peak participation and often come up with some great, innovative ideas.

I will discuss a couple of personality types here and you will get the drift:

You don't care how much your savings yield you, you hardly act in a hurry but that bank balance, is directly proportional to your heart beat. What is great about your attitude however, is that you probably take your decisions in an analytical way, feel the need to diminish your anxiety on your own. All you need, is a few nudges – to max out your EPF contribution, to invest in ideas that reduce your taxes, and sign up for anything that has automated payments deducted from your account. Home loan EMIs do not qualify but that is a topic for another day!

If you are an anxious spender, well. You are probably a hoarder – a watch hoarder, a handbag hoarder, shoes, clothes you have too much and little space to contain them. Something about the ‘here and now' of life has got into your head in a slightly dysfunctional way and you probably have little left in your bank account at the end of any month. It is possible that you quarrel with your partner should she or he bring this up and then make up by going out for dinner and spend some more – the ‘one life' argument etc. For you, taking that first step is most important –sign up for anything at all, even if it is an evil, high brokerage paying insurance plan, a non alpha generation mutual fund, a PPF, anything that is mandatory, less flexible and restricts access.

Not only do you need an advisor, you must work with a fee-only advisor and ensure that coaching you on your financial behaviour is part of the contract she/he signs with you.

Explaining all the personality types would be digression. But if you are interested in knowing them, feel free to write to us.

A lot of us seem to think that ‘more telling' will lead to action. There is enough and more evidence from different walks of life where we do not necessarily ‘adhere' to even the best plans suggested to us – be it in nutrition, exercise or other matters of health. World over, psychologists are working on how there is a similarity between adherence (or lack of it) to health advice and financial advice. It is time that we in India unleash this discussion as well.

Abaneeta Chakraborty has close to two decades of experience in managing money for ultra-HNI families. She founded the firm Abanwill Consultants LLP in 2017 to provide independent views on investing.

The views expressed here are those of the author and do not necessarily represent the views of BloombergQuint or its editorial team.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.