- India's GDP rose 8.2% in Q2FY26, beating estimates and marking fastest growth in six quarters

- Nominal GDP grew 8.7% in Q2, higher than 8.3% in Q1, driven by manufacturing and services sectors

- Chief Economic Advisor expects full-year growth upward revision to 7% or higher from 6.5% forecast

India's gross domestic product (GDP) beat Street estimates and rose 8.2% in the July-Sept quarter of the current financial year, driven by robust manufacturing and services output. With this, the Indian economy has grown the fastest in six quarters. Despite the strong Q2 show, global brokerage Bank of America Corporation (BofA) believes India's GDP in FY27 will still slow down.

BofA noted that India's Q2 GDP strength is 'unlikely to reduce future anxiety'. According to the brokerage, the moderation represents risks of growth downsides emanating from risks of trade tariffs by US for longer, the effects of tax cuts fading at the margin, and recent consumption frontloading, which can pay back in coming months.

"With the headline GDP growth coming in stronger than ours and Street expectations, we raise our GDP estimate for FY26 to 7.0% from 6.8%, but maintain our relative caution on the GDP growth outlook in FY27, expecting a modest slowdown in growth to 6.5% in FY27," it said.

"While commodity prices and terms of trade remain low, and monetary policy is expected to ease further, we believe GDP growth will have upside risks from removal of tariffs, potential for more expansionary fiscal measures and ongoing stability in domestic spending, while downside risks may emanate from more trade measures," said BofA on India's GDP print.

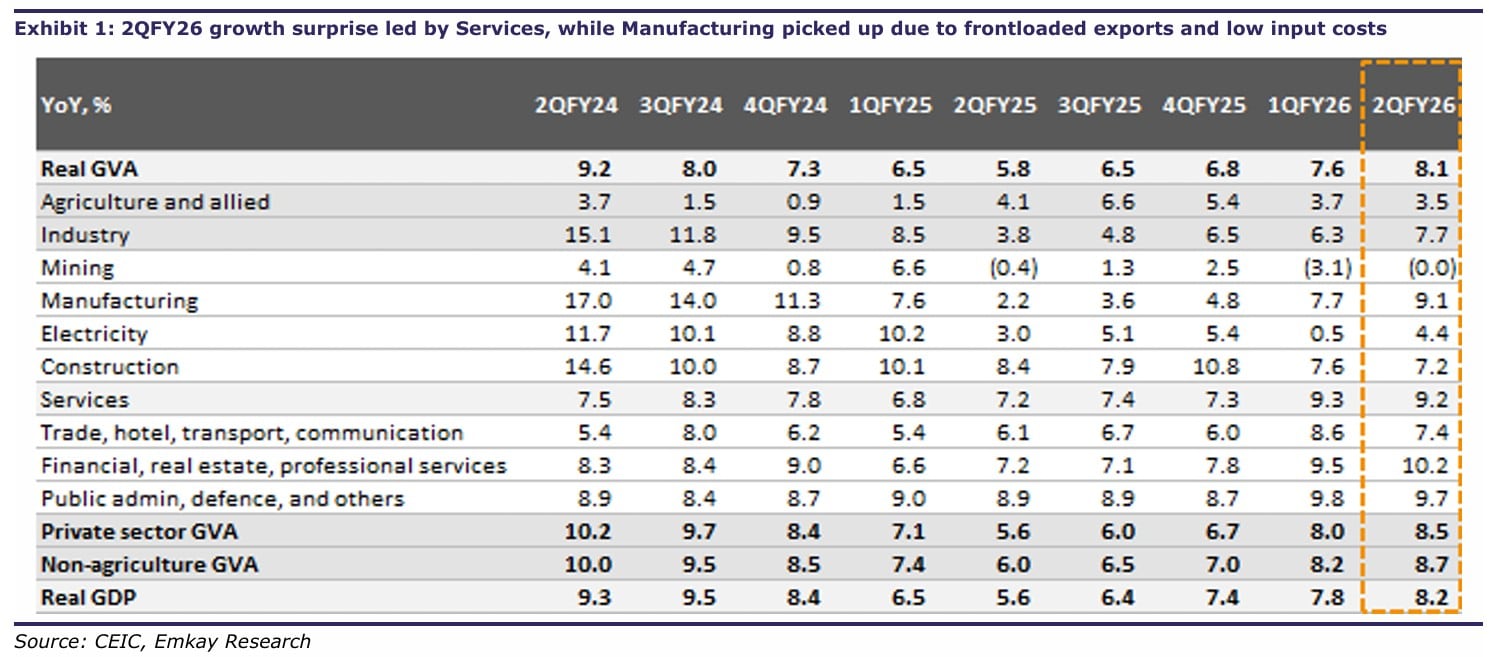

Brokerages revise India's FY26 GDP growth estimate

On the Q2 GDP growth data, domestic brokerage Motilal Oswal Financial Services said, "Given real GDP growth of 8% in 1HFY26, we expect FY26 growth to pick up to 7.5% (base case), up from our earlier expectation of 7%." Despite the adverse impact of US tariffs on India's manufacturing sector, domestic demand has so far managed to hold the growth strong.

As per Motilal Oswal, the GST cut-led pickup in consumption in Q2 and rise in government spending in Q3 should provide the necessary fill-up to offset the weak exports. Low inflation narrowed the gap between nominal and real growth rates.

"For FY26, we expect GDP growth of 7% on favourable monsoon, GST rate rationalization, and easier monetary policy. Headwinds remain from US tariffs and weaker global GDP growth," said Anand Rathi Shares and Stock Brokers Ltd.

Brokerage Equirus Securities said 1H real GDP growth of 8% is higher than RBI's projection of 6.8%. "We revise our FY26 GDP to 7.2%-7.5% vs RBI's estimate of 6.8% with some slowdown expected in 2H with export drag and slower government capex due to revenue constraints and frontloading in 1H."

Emkay Global Financial Services Ltd eyes H2 growth may slow to ~6.7% (vs 1H: 8%), a US-India trade deal would improve the growth outlook. "Nevertheless, nominal GDP growth will remain sub-8%, and slippage here will require recalibration of all macro and market variables," it said.

Street divided on RBI rate cuts

Motilal Oswal said with a strong GDP growth print in 2Q, the possibility of a rate cut looks limited. But what remains to be seen is if the consumption-led pickup witnessed during Oct-Nov fizzles out in Q4. "The global tariff situation also remains a key monitorable," added the brokerage.

RBI lowered its inflation forecast for FY26 to 2.6% from 3.1%. "Technically, inflation would be way lower than the RBI's forecast of 2.6%. The possibility of headline inflation below 2% for FY26 remains quite high," said Motilal Oswal.

"This implies, there is policy space for the last insurance rate cut. The RBI should utilize the policy space and close the final loop. If the US-led tariff uncertainty lingers for longer than anticipated, the adverse impact would be far greater," it added.

"While real GDP numbers are strong (benign inflation print offering a great deal of support), nominal GDP growth trending lower is a worry. Hence, we continue to expect one more cut of 25 bps by the RBI in the Dec meeting," said Equirus Securities.

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.