(Bloomberg Markets) -- For more than 160 years, Credit Suisse Group AG's stone-clad headquarters on Zurich's moneyed Paradeplatz has exuded power, stability and quiet wealth. Those days are over.

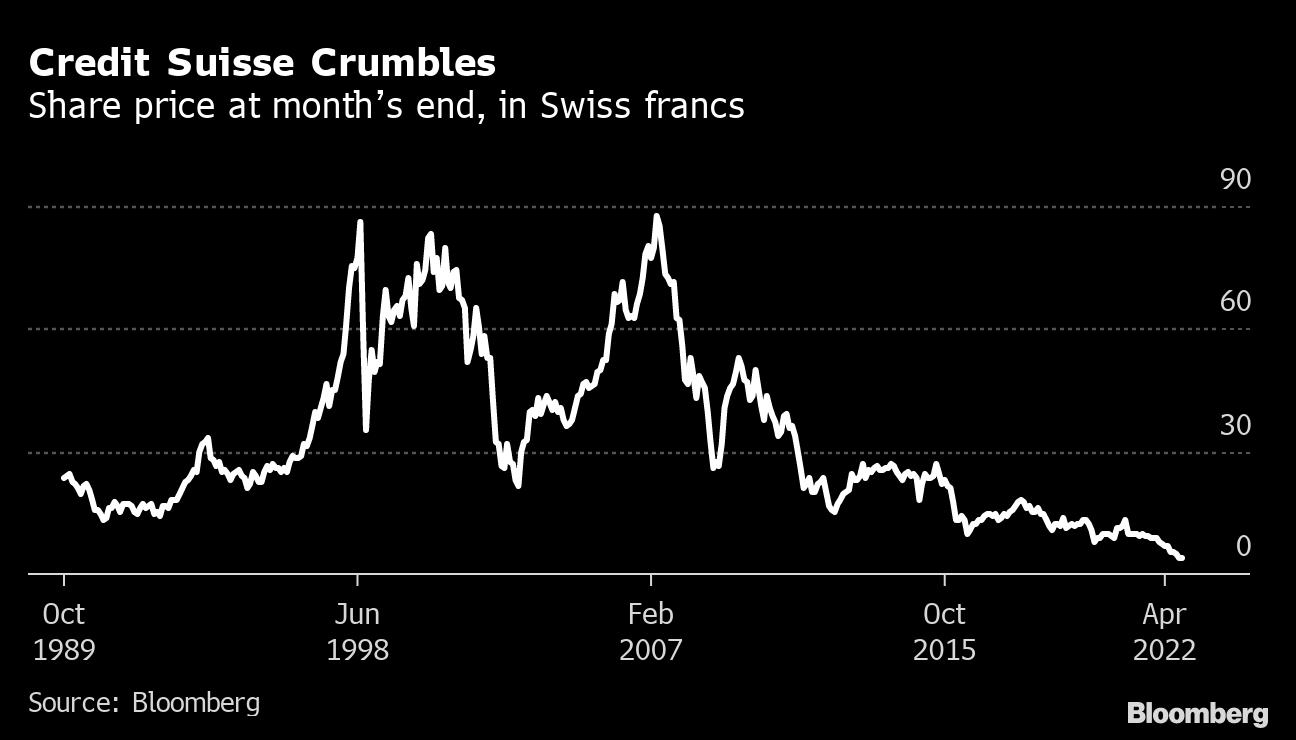

While the building's colonnaded facade is still a sight to behold, the operations inside are suffering deeply, and the bank's ability to bounce back hangs in the balance. Rocked by a steady drumbeat of scandals and management upheaval in recent years, the company that helped position Switzerland as a linchpin of international finance is losing billions of dollars. Key employees are leaving, and some clients have pulled out money. With the stock at record lows—down more than 90% since its peak—investors are angry.

A new leadership duo of Chairman Axel Lehmann and Chief Executive Officer Ulrich Körner is now pitching a return to Credit Suisse's Swiss roots as the best way forward. They are raising $4 billion, with some of it coming from Saudi Arabia, and culling 9,000 jobs. Most important, the company is carving out its investment banking operations to end a three-decade effort to compete on Wall Street.

Beyond capital and costs, a real recovery hinges on the bank's ability to overcome its past. While other companies have also had their share of scandals, what sets Credit Suisse apart is how often it dismissed the episodes as one-offs and quickly pivoted back to business as usual. It's one of the few banks that's in a weaker position today than when it emerged from the 2008 global financial crisis—notably without a state bailout.

delved into four key episodes from Credit Suisse's history to show the underlying issues plaguing the bank. At each turn, the company had an opportunity to fix deficiencies but fell short, revealing a deep-seated hubris.

In buying First Boston, Credit Suisse took on a culture of risk-taking fueled by ambitious profit targets and the pursuit of big bonuses. That ethos spread within the private bank, helping pave the way for a costly fraud perpetrated by an inexperienced employee. Internal tensions erupted into boardroom spying, and a disregard for compliance and controls left the bank exposed to the collapse of a major trading client.

In response to queries from , Credit Suisse said it has taken “significant measures” to “address the deficiencies identified over past years,” and “will continue to evolve strong remedial actions, closely working with key regulators, while actively addressing legacy issues.”

Together these episodes paint a picture of the complex challenges facing Körner and Lehmann as they try to restore the confidence of clients, investors and employees. It may be the bank's last chance to get it right.

I. TAKING ON WALL STREET

On a sweltering summer day in 1990, Archibald “Archie” Cox Jr. arrived at a hotel in Boston's Back Bay neighborhood ready to sketch out the collapse of an American financial powerhouse. The veteran Morgan Stanley banker had been recruited by Credit Suisse some months earlier to assess a Wall Street bank so intertwined with the city's history that it still carried its name: First Boston Corp.

In a meeting room in what was then the Ritz-Carlton hotel, Cox sat across the table from Rainer Gut, the chairman of Credit Suisse, which had held a large minority stake in First Boston since 1978. As problems mounted at its US partner, the Swiss bank was faced with rescuing it or letting it collapse.

The investment bank had embraced high-yield debt markets during the 1980s and lent billions of dollars to fund risky buyout transactions. The once-lucrative industry had imploded, and First Boston was stuck with bad loans.

As Cox scribbled down the most problematic deals on a legal pad, one loomed larger than others: a $457 million loan for the leveraged buyout of Ohio Mattress Co.—an amount equivalent to about 40% of First Boston's equity capital at the time. The failed financing for about half of a $1 billion buyout would go down in Wall Street infamy as “the burning bed.”

Cox and Gut saw an opening for Credit Suisse to take control of First Boston for a modest capital injection of $300 million and backstopping bad loans. The deal allowed the Zurich-based lender to leapfrog European rivals such as Deutsche Bank AG to become a global financial powerhouse with deep ties to Wall Street.

“I believe Credit Suisse did view it as an opportunity but one that came at a considerable cost,” says Cox, who was installed as First Boston's CEO after the takeover.

Gut looked past the Ohio Mattress debacle and decided to bail out First Boston. Buoyed by fresh capital from its Swiss partner, the US bank took over the Cleveland-based bedding company and later sold it off.

“Burning bed became the poster child for a whole sorry episode in the annals of corporate finance, partly because of the headline-grabbing nickname,” says Martin Fridson, chief investment officer at Lehmann Livian Fridson Advisors LLC, who worked in high-yield debt at Merrill Lynch & Co. at the time. “But it was by no means a unique phenomenon.”

In the wake of the takeover, Credit Suisse embraced the same kinds of risky businesses—such as leveraged finance and mortgage-bond trading—that led to the burning bed deal. Subsequent leaders of the Swiss lender pushed through numerous overhauls, eventually dropping the once-proud First Boston name in 2006 in an attempt to create a singular identity at Credit Suisse, and integrated Wall Street staff with its more subdued army of private bankers.

The investment bank made a lot of money, contributing more than half of the company's revenue for years. But it also cost the bank billions of dollars in losses during the global financial crisis.

First Boston's issues “could have been sorted out, but they just didn't have the right people in place and the right discipline in place, and I suspect they still don't,” says Cox, now 82, who stepped down in 1993.

Still, Credit Suisse survived the financial crisis by raising money from shareholders instead of taking a government rescue like peers including Swiss rival UBS Group AG. That fed Credit Suisse managers' confidence in their ability to control risk-taking in investment banking. And so, when post-crisis rules threatened the bank's profit goals by substantially raising the cost of some lucrative lending and trading businesses, Credit Suisse took an ax to expenses, which fell hardest on risk and compliance staff who were seen as less critical than fee-earning bankers.

The company's share price is now far lower than on that fateful day in 1990 when the First Boston takeover began to take shape. After two decades of trying to create a bank that could serve the world's billionaires and corporate giants, Credit Suisse is finally admitting defeat. And ironically, its way forward includes reviving the First Boston name, which is being bestowed on a smaller, separate investment bank that will likely be disposed of in a few years.

II. PRIVATE BANKING FRAUD

In December 2004, Patrice Lescaudron, a slight, soft-spoken Frenchman, walked into Credit Suisse's Geneva offices overlooking the Rhône river for his first day as a private banker. His starting salary was 160,000 Swiss francs ($140,000), modest by the standards of Geneva's bankers but not bad for a 41-year-old rookie. He'd been recruited mainly for his Russian-language skills, which he acquired in Moscow while working for cosmetics company Yves Rocher Group.

At the time, then-CEO Oswald Grübel was restructuring Credit Suisse to link more closely investment banking and wealth management. Commissions from taking care of rich people's money provided a more stable stream of revenue to balance out the roller coaster from dealmaking fees. Grübel was also expanding the private bank just as a burgeoning class of oligarchs emerged from the former Soviet sphere.

With no clients and no banking experience before joining Credit Suisse, Lescaudron initially spent as many as 10 months a year in Russia hustling for business. After a top manager on the Russia desk left, he found himself in the right place at the right time and inherited two clients who kept $1.6 billion of their assets with Credit Suisse. One was Bidzina Ivanishvili, a billionaire and former prime minister of Georgia. Overnight, the novice banker gained power and stature but also enormous pressure to perform.

Then the market turmoil of 2008 led to a huge plunge in investment portfolios. To dig his clients—and himself—out of the hole, Lescaudron started dipping into Ivanishvili's account without his knowledge, using the Georgian's money to try to win back losses for other clients.

The deceptions were shockingly simple. He cut out Ivanishvili's signature from a document, pasted it on trade orders and photocopied them, according to Lescaudron's own admission. Buoyed by his initial success at filling a $60 million hole, his scheme continued and grew.

There were red flags along the way. Lescaudron was given verbal warnings and written cautions by supervisors in 2008, 2011 and twice in 2013 for breaching the bank's compliance policies. Specifically, these infractions included making unapproved payments, disregarding know-your-customer guidelines and engaging in front-running ahead of client orders. And yet Credit Suisse failed to stop him.

He was finally caught in 2015 after a massive investment on a volatile pharmaceutical stock went sour. With tens of millions of dollars in margin calls suddenly due to cover the bad bet, Credit Suisse's lawyers demanded he explain his actions.

“It's one of the mysteries of life,” Lescaudron said, and then told them he could have covered the money with more illicit activity but “had had enough.” He was convicted of fraud in 2018 and took his own life in 2020.

The scandal is still playing out in courts from Bermuda to Singapore. The bank has so far been ordered to pay Ivanishvili more than $600 million in damages for Lescaudron's actions, and the bill could rise to more than $1 billion, making him arguably the costliest hire in the bank's history.

Credit Suisse doesn't believe it's at fault and is appealing a verdict in Bermuda that awarded damages to Ivanishvili. The bank says Lescaudron was a lone wolf who hid his crimes. Half a dozen people close to the supervision of Lescaudron didn't respond to requests for comment.

But throughout the years, the bank had failed to adequately supervise other inexperienced staff, or to catch employees who were later dismissed as rogue actors. In 2020, a private banker for African clients forged documentation on an investment contract and was caught after a loss of about 10 million francs. In 2022, a Swiss court convicted Credit Suisse and a private banker of failing to prevent money laundering by an ex-wrestler-turned-cocaine-smuggler. The banker in that case—a former professional tennis player who was born in Bulgaria—was recruited in 2004 even though she had minimal credentials, much like Lescaudron. She and the bank are appealing the decision, which was the first criminal conviction for a major Swiss lender in the country's history.

As long as money was flowing, the bank indulged Lescaudron's bad behavior, according to an independent investigation into the fraud commissioned by Finma, the Swiss banking regulator. Relations with key clients and large sums of money contributed to a “lack of assertiveness on the part of superiors and inconsistent prosecution of misconduct,” Finma's report said, though it stopped short of concluding that the bank knew of the fraud.

A Bermuda court similarly determined that the bank's local insurance unit turned a “blind eye” to Lescaudron's wrongdoing. Credit Suisse declined to comment on steps taken to avoid a repeat of such fraud.

III. EXECUTIVE SPYING

In January 2019, Iqbal Khan went to a dinner hosted by then-CEO Tidjane Thiam, who was both his boss and his neighbor in a wealthy suburb on Lake Zurich. Khan, who ran wealth management and had his sights set on one day leading Credit Suisse, made a disparaging remark about Thiam's garden. It was enough for a long-festering feud between the two men to break out into the open.

A few weeks later, Khan was passed over for promotion, and in July he quit the bank. When he later accepted a job at UBS, the move caused alarm in Credit Suisse's top ranks that he might poach key personnel.

Driving through Zurich with his wife in September, Khan noticed he was being followed. He stopped the car and took pictures of his pursuers with his mobile phone. That led to a physical altercation with one of the men trying to grab the device away. Police were called in, and the men were detained.

The lurid affair, which eventually included one of the suspects taking his own life, dragged Credit Suisse into the tabloids. The scandal shattered the company's reputation for discretion—the bedrock of Swiss banking—and exposed a culture in which personal vanities outweighed ethical and legal boundaries.

The blame for the surveillance was ultimately pinned on Chief Operating Officer Pierre-Olivier Bouée, who was allowed to resign at first and later “fired for cause.” An investigation by the bank found that the longtime associate of Thiam's had used an encrypted messaging app to collude with Credit Suisse's head of security to hire private investigators to follow Khan. Thiam said he didn't know about the spying.

“The surveillance of Iqbal Khan was strictly an isolated event, and full accountability has been taken by the individuals concerned,” Thiam said in an internal memo in October 2019. “Difficult questions about culture and ethical standards have been raised. The board moved swiftly to address these.”

Although the bank rushed to dismiss the embarrassing incident, it was soon revealed that it wasn't unique. In February 2019, Credit Suisse had also hired a firm to track Peter Goerke, human resources chief and a member of the executive board at the time, for several days.

During this period, Thiam was struggling to implement a restructuring plan after the bank had lost billions of dollars on risky trades, which the French-Ivorian executive said he wasn't aware of. Meanwhile, investigators were uncovering the extent of Lescaudron's fraud, adding to the toxic mix. While Bouée also took the blame for the second spying episode, the distractions were too much for Thiam to shake off.

“We saw a deterioration in terms of trust, reputation and credibility among all our stakeholders,” said Chairman Urs Rohner—himself blamed by some investors for the infighting—when announcing Thiam's exit in February 2020.

But it would get worse. As part of an investigation prompted by the Khan episode, the Swiss banking regulator uncovered five additional cases of surveillance from 2016 to 2019, all outside Switzerland and involving a mix of former employees and third parties.

“In most cases, decisions to carry out observations were taken informally and without comprehensible reasons being given,” Finma said. Worse still, Credit Suisse's statements to the public and the regulator “subsequently proved to be partially incomplete or even inaccurate,” the watchdog said in October 2021, reprimanding two individuals and opening enforcement proceedings against three others.

The bank said it had taken “decisive steps” to prohibit surveillance of employees unless there are compelling reasons such as threats to physical safety. It declined to comment on why it initially dismissed the spying on Khan as an isolated incident.

IV. A TRADING CLIENT BLOWS UP

On March 24, 2021, Credit Suisse's top trader, Paul Galietto, received some terrible news: The trading desk's biggest client wouldn't be able to pay the more than $2 billion it owed the next day.

Archegos Capital Management, the New York-based investment firm that managed billionaire Bill Hwang's personal fortune, had spent the previous two days settling up with other lenders after outsize bets went bad, and there wasn't enough left for Credit Suisse.

What ensued was like a slow-motion car crash, according to people who were there and asked not to be identified because they aren't authorized to speak publicly. Executives in New York, London and Zurich turned on one another as senior management sought to avoid blame for the vast losses.

Shell-shocked traders tasked with selling Archegos's collateral discovered it was a losing battle against rivals that were quicker off the block. On March 29, Goldman Sachs Group Inc. declared it had avoided a hit from the collapse. Credit Suisse, by contrast, was still in the process of surveying its damage.

Over the following Easter weekend, then-Chief Financial Officer David Mathers spent every waking minute calculating the cost, while then-CEO Thomas Gottstein determined which executives would take the fall.

It wasn't until April 6—nearly two weeks after learning of the pending default—that Credit Suisse was able to come up with an initial tally: $4.7 billion. The loss had more than doubled from the margin call as the value of Archegos's assets collapsed, and it would eventually grow to $5.5 billion, obliterating more than a year's worth of profit. It was the blow that tipped the bank into the existential tailspin it's grappling with today.

Executives were already under fire for failing to protect the bank and wealthy clients from the collapse of a $10 billion suite of funds it ran with now-disgraced financier Lex Greensill. The twin episodes shocked the finance world, but in hindsight they were decades in the making.

In the failure of Archegos, a lone risk manager had tried to warn his bosses for six months that Credit Suisse didn't have enough collateral to insulate itself from potential losses if the investor's strategy backfired. But the alarm was ignored, part of a trend of eroding controls.

Starting in 2012, the bank embarked on a drive to cut $4 billion in costs. Within a few years, risk managers were relocated to cheaper locations. A New York team moved to Raleigh, North Carolina; staffing transferred to Poland from more expensive European cities; and a global credit risk group was shifted to an outpost near Singapore's Changi Airport.

After Thiam became CEO in 2015, he embarked on a plan to split businesses regionally, limiting the risk team's ability to get a global view of the bank's exposure, according to people familiar with the operations who weren't authorized to comment.

In 2016 the bank conducted an internal review, dubbed Project Apple, into the reasons for a several hundred-million-dollar loss on a loan made to American Energy Partners LP only a few months before it went bankrupt. The evaluation concluded that risk managers lacked the resources and authority to perform their role of protecting the bank from deals that turned sour.

Meanwhile, regulators in the UK, Switzerland and the US had repeatedly warned Credit Suisse that its procedures weren't strong enough to handle a crisis, people with knowledge of the reports said.

Even as investigations highlighted deficiencies, the bank's leadership team—led by Rohner from 2011 until 2021—reduced spending on risk management to help meet profit goals, people with knowledge of the decisions said. From 2019—Thiam's last year as CEO—through to Archegos's default, about 40% of managing directors on the risk team left, most of them involuntarily.

The bank's complexity, culture and controls were to blame for the massive Archegos loss, according to an independent report into the collapse by law firm Paul, Weiss, Rifkind, Wharton & Garrison. Credit Suisse had a “lackadaisical attitude towards risk” and “failed at multiple junctures to take decisive and urgent action,” the report concluded.

The bank responded to the report with a series of measures to fix the shortcomings and vowed to use the incident as a “turning point for its overall approach to risk management.”

In March 2021, Gottstein declared that “serious lessons will be learned” from the Archegos debacle.

Credit Suisse's future now depends on reassuring investors, clients, regulators and employees that this time the bank won't just go back to business as usual.

More stories like this are available on bloomberg.com

©2022 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.