(Bloomberg Opinion) --

When to Recede?

There are plenty of decent recession indicators out there to alert you to a slowdown before it happens. The problem is the lead time. Even after the alarms flash, it can take a while for growth to subside. Let's start with the yield curve, the scariest indicator at the moment.

The following chart, produced by Jonathan Golub, US equity strategist at Credit Suisse Group AG, shows the spread between three-month and 10-year yields has been foolproof, but that in every incident in the last half century the recession didn't start until the curve began to steepen. Usually it was no longer inverted by the time the recession began:

Using futures, Golub illustrates that the market is currently braced for the curve to invert a little more, and then stay inverted next year and for much of 2025. That in turn implies minimal risk of a recession this year. Given that inflation is still uncomfortably high, Golub suggests that we shouldn't expect one to start until the latter half of 2025:

This version also implies something like the no-landing scenario, in which the economy continues to heat up, bringing price rises with it, before a recession sets in. This is Golub's chart on the likely course of the yield curve:

Another leading indicator much discussed of late is the Conference Board's composite Leading Economic Indicators index. As this chart from Joe Lavorgna of SMBC Group shows, every recession in the last half century started after the LEI peaked and began to fall — and it started falling last year:

This is an indicator dangerous to ignore. But if timing is what matters, its signal isn't that strong. As time has gone by, the economy has pegged on for longer and longer after the LEI peaks, before dropping into recession. The average from the last eight cycles has been 11 months, but it topped 21 months before the Great Recession began at the end of 2007. To quote Lavorgna:

One final plausible recession indicator comes from profit margins. When companies don't make a fat margin, they are less likely to invest and more likely to lay people off. As Albert Edwards of Societe Generale SA shows below, recessions tend to start when operating profit margins peak and start to fall:

Profit margins are a tricky concept to measure, made more complicated by the fact that the profits reported for tax purposes, that show up in the national accounts, are different from those under Generally Accepted Accounting Principles, which companies publish. If we use the official data produced in the course of calculating gross domestic product, however, margins look to have stalled:

According to Edwards, the evidence from profit margins suggests a more imminent recession, because in an accounting sense, “declines in the business investment cycle (including inventories) account for each and every recession.”

Tightening of margins has historically been driven more than anything else by the cyclical struggle between capital and labor. When unemployment is low, and labor's negotiating position is strong, margins tend to come down. And of course the labor market looks strong at present. Ultimately, that gives yet another reason to brace for excitement when the latest US non-far payrolls are announced on Friday.

A Beige Labor Market

On that subject, there are more runes to read. Jerome Powell of the Federal Reserve managed to get through another day of questioning, this time from the House of Representatives, without creating any news. Meanwhile, those who don't trust the official quantitative data from government statisticians in general, and disbelieved January's remarkably strong employment report in particular, could instead read the latest edition of the Fed's Beige Book, which culls together impressions from the Fed's regional branches.

But how do you synthesize collated opinions into something investable? Bloomberg's headline suggested — correctly — that it gave no useful fuel for anyone hoping that the Fed would soon have to desist from hiking rates. But neither was it strong enough to keep market interest rates moving upward. Peter Tchir of Academy Securities was honest about not reading the whole thing — and it's unlikely going through every word would change this judgment significantly:

That assessment seems fair. There's been such a swing to cover the risk of a hawkish Fed since the beginning of last month that even a little weakness in the forthcoming employment and inflation releases could help risk assets lurch back.

Quantitative data, meanwhile, also seemed to come in a shade of beige. The JOLTS (Job Openings and Labor Turnover Survey) for January showed there are still more than 10 million job vacancies in the US, which yet again is more than economists had expected:

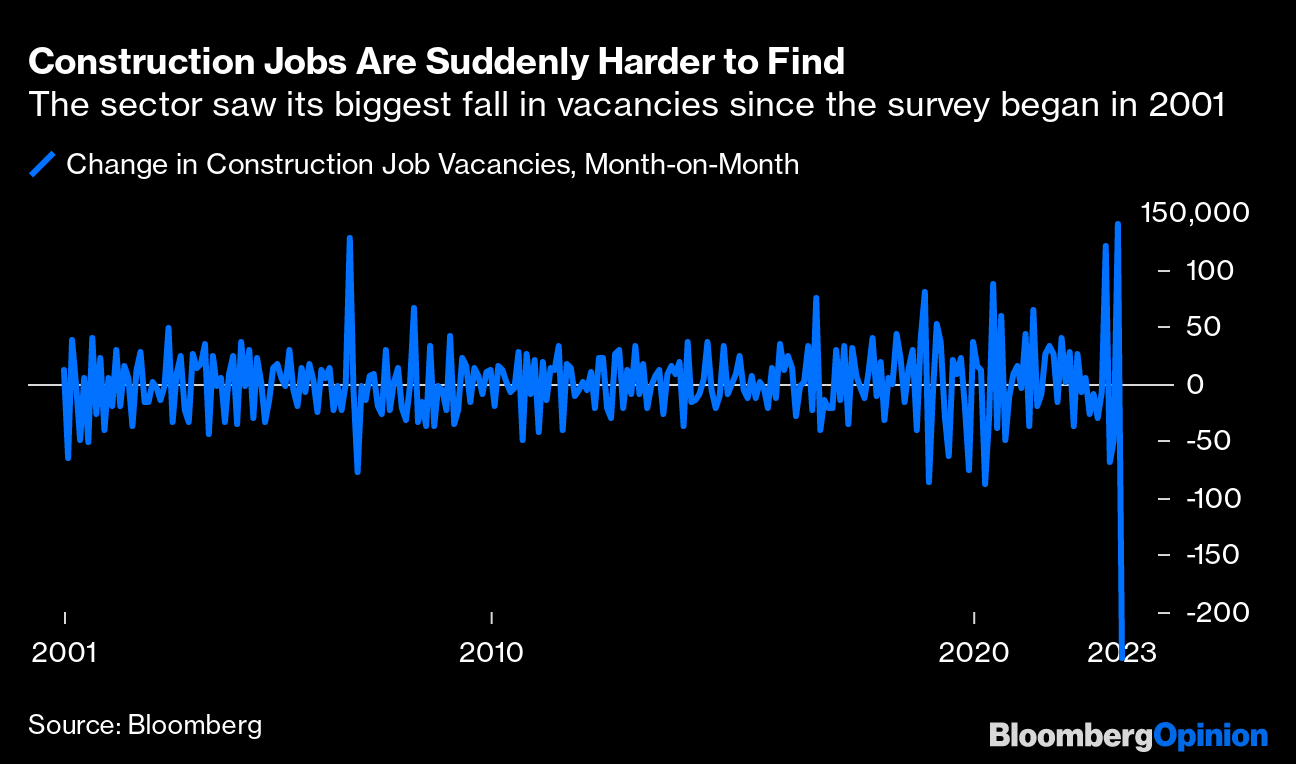

However, there was one startling detail in the breakdown. Vacancies in the construction trade plummeted in January by the most since the survey started in 2001:

This stunning number possibly helps to answer one of the more difficult conundrums in recent US data. Last month, Ajay Rajadhyaksha of Barclays Plc pointed out an odd disconnect between demand for housing (which was dropping predictably) and demand for construction workers, which was unaffected. How could this be, he asked?

He might well have been right. Adding fuel to the fire, mortgage rates briefly appeared to be falling in January. They've since resurged with a vengeance, in a way that's bound to have an impact on demand for housing (and therefore demand for construction workers):

Friday's employment numbers should be very useful, but the JOLTS give a strong hint that the Fed's hiking cycle may at last have given the desired jolt to a corner of the economy that is more rate-sensitive than most, and which the central bank can reach more directly. It'll be interesting to find out if that's right.

Who Cares?

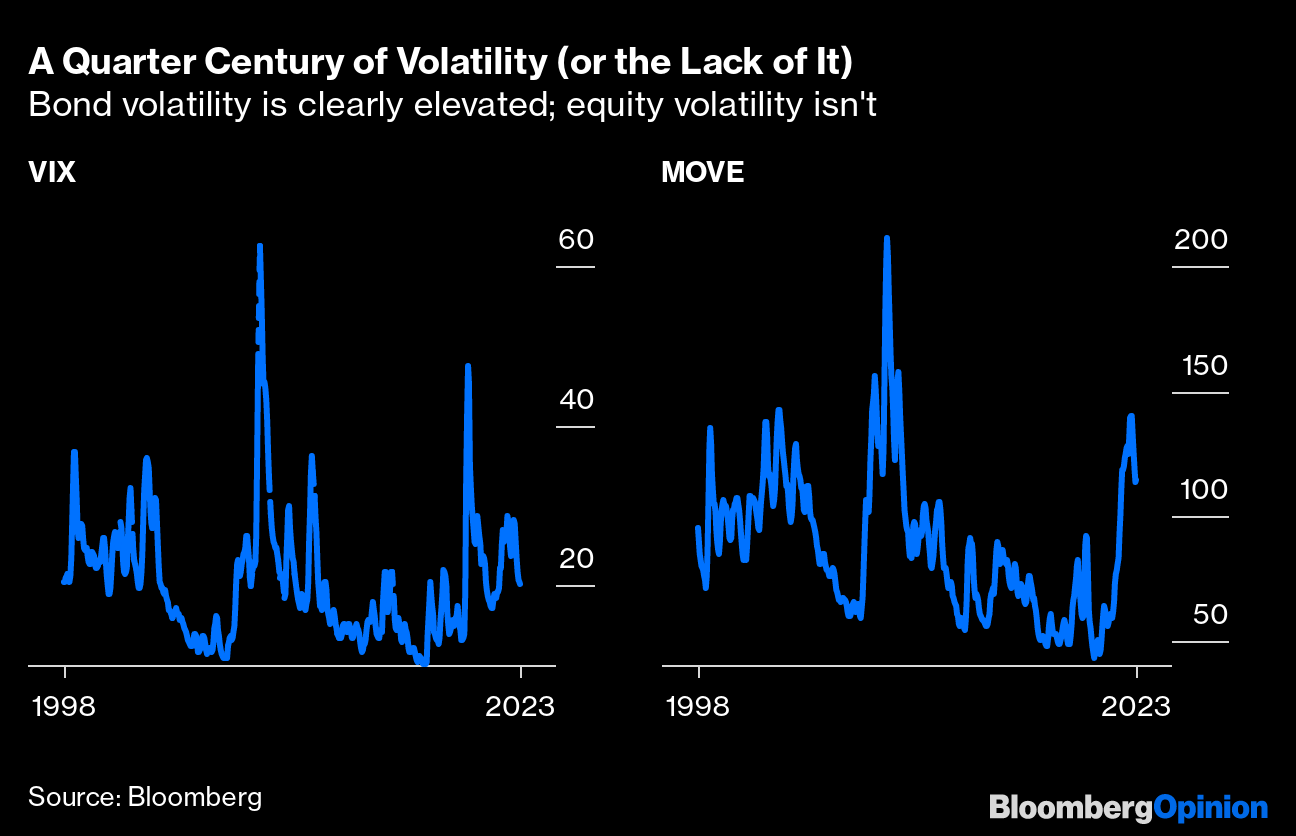

There's been an epic reset of rate expectations since the beginning of last month. But the titanic moves in bond markets have been coupled with relatively mild turbulence in stocks. The MOVE index, a popular measure of volatility in bonds, is near the top of its historic range (outside the Global Financial Crisis), while the VIX index of equity volatility is wholly unexceptional. The following charts use 50-day moving averages to avoid daily spikes that can make trends harder to spot:

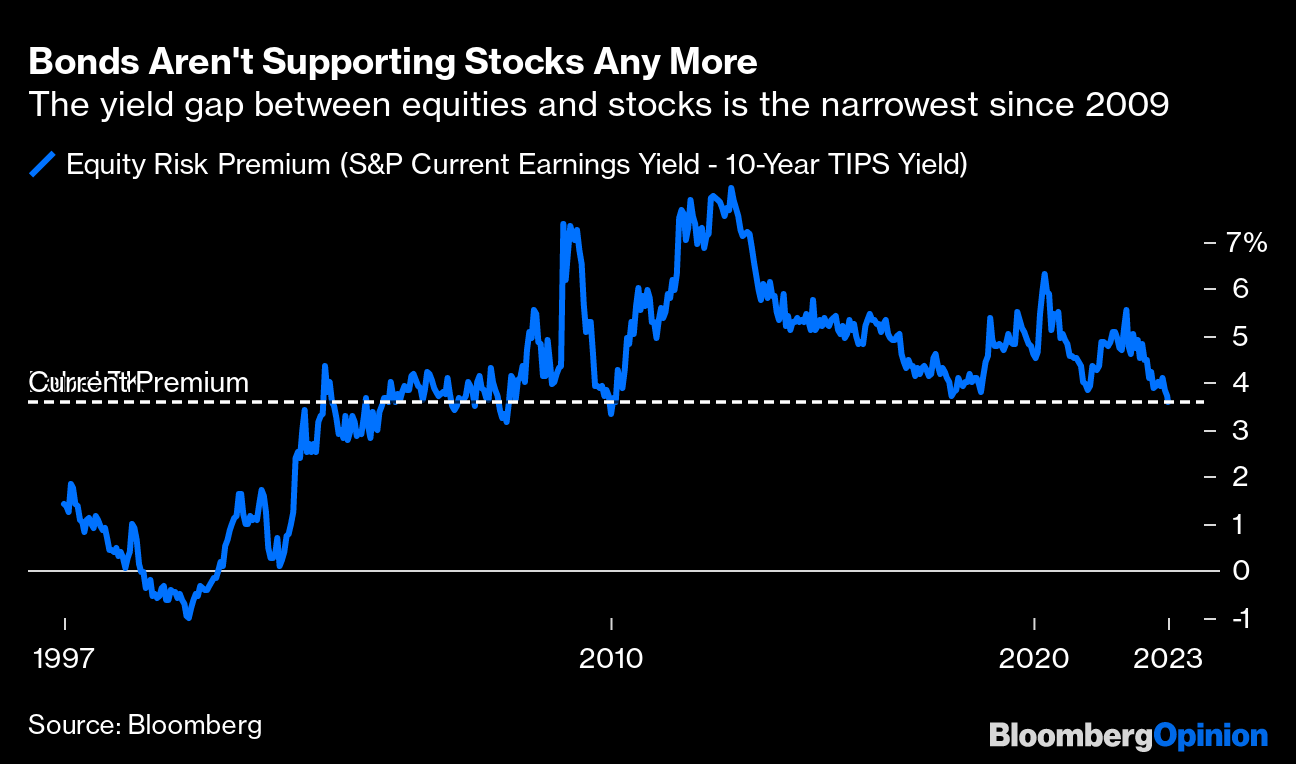

To view this another way, equity-risk premia suggest the stock market is its least attractive in a while. In the following chart, Oliver Allen, senior markets economist at Capital Economics, compared the forward earnings yield (the inverse of the price/earnings ratio) for the S&P 500 with the 10-year TIPS yield. This is a simple version of the equity-risk premium — the more the yield on stocks exceeds the yield on bonds, the more you are being paid to take the risk of holding shares. The two have gone in different directions of late, with the S&P 500 growing more expensive even as bond yields approach last year's highs:

To express this a different way, here is the spread between the S&P 500 current earnings yield and the 10-year TIPS yield going back to 1997, using Bloomberg data. On this measure, stocks are their least attractive relative to bonds since the end of the crisis year 2009:

This seems a very strange way to react to the dose of anxiety that sparked the rise in rates in the first place. One defense is that any recession looks much more distant now (the so-called no-landing scenario). But Allen of Capital Economics suggests that this is an erroneous belief:

China Wakes

It's been roughly three months since China announced it was walking away from its restrictive and long-held Covid-Zero policy. That easing of controls, from testing requirements to mobility constraints, happened slowly then all at once beginning in December. Many were extremely bullish about the reopening of — by some measures — the world's biggest economy. But after a steep run-up in November, the rally has lost momentum. The chart below shows the ratio between the MSCI China Index relative to MSCI Emerging Markets ex China and the picture is clear: China, based on the downward direction of the line, is underperforming again:

What gives? The downtrend started toward the end of January, around the time millions of Chinese celebrated their first Lunar New Year since the Covid-Zero exit. While travelers swarmed to destinations, box office sales jumped and hotel bookings exceeded the comparable period in 2019, the CSI 300 Index of A-shares listed in Shanghai and Shenzhen failed to breach its recent peak from last July. And since then, it's been a trudge:

Of course it's hard to make sense of complex, nuanced movements, especially in unprecedented circumstances. But it certainly wasn't helped by the 5% economic growth target for 2023 — combined with a supportive spending plan — that the National People's Congress announced earlier this week. Traders were disappointed. Bloomberg Intelligence economists led by Chang Shu called the figure “conservative:”

The growth target is lower than 2022's 5.5% goal, which Shu had also expected this year. (At just 3%, China missed its GDP goal last year for the first time in decades.) Shu added that 2023's growth could outperform — a post-pandemic rebound and a low base for comparison should drive a 5.8% expansion.

To be sure, the latest Chinese inflation data, published Thursday, came in well below expectations and suggested the economy wasn't as lively as hoped. It showed signs of life via its upbeat PMI data. Services activity rebounded strongly in February as the faster-than-expected reopening helped lift consumer confidence and demand. The Caixin China services purchasing managers' index — a private gauge that focuses on smaller firms compared to the official PMI — hit its highest level since August 2022.

For Kristina Hooper, chief global market strategist at Invesco, China's “revenge living” (spending like there's no tomorrow to relieve the Covid frustrations) that she has long anticipated has begun:

It may not be what bulls hoped for, but TS Lombard's Skylar Montgomery Koning and Andrea Cicione say upside remains, as China'seconomic backdrop sharply contrasts with much of the rest of the world. Its “relatively subdued inflation” allows policymakers to stimulate more than its rivals, which should make it one of the best-performing economies, at least in the first half of this year. “Spillovers” from Chinese growth are likely to be more limited than in the past, as this expansion will focus more on services rather than investments that sucked in imports. Thus, Koning and Cicione conclude that it probably makes sense to buy MSCI China relative to MSCI EM ex-China.

Survival Tips

When times are tough, sport can get you through — particularly, for many of us, soccer. And there is nothing more reassuring than a dog. Put them together and you get moments like Tuesday night's match between the Philadelphia Union and Alianza of El Salvador, when a dog interrupted play (and demonstrated some impressive ball skills). Dogs, it turns out, are good at football. This wasn't the first time an animal had interrupted play; there's a lot of examples over the years, in some of the world's biggest leagues. But it's not always a cause for laughter when a dog comes on the pitch — as this tragic scene from Ted Lasso should remind us. And by the way, Ted Lasso's third and last season comes out next week. It will be worth watching.

More From Bloomberg Opinion:

- Putin and Saddam Hussein Have a Lot in Common: Leonid Bershidsky

- Wagamama's Hedge Fund Spat Is Poised to Escalate: Matthew Brooker

- Retailers Know Consumers' Shopping Spree Won't Last: Leticia Miranda

--With assistance from .

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

John Authers is a senior editor for markets and Bloomberg Opinion columnist. A former chief markets commentator and editor of the Lex column at the Financial Times, he is author of “The Fearful Rise of Markets.”

More stories like this are available on bloomberg.com/opinion

©2023 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.