The Monetary Policy Committee of the Reserve Bank of India today announced its decision to unanimously hold key policy rates steady, an outcome that was along expected lines. To recall, all key rates of the Liquidity Adjustment Facility Corridor—Repo Rate, Reverse Repo Rate, and Marginal Standing Facility Rate—were last changed (lowered) in May 2020.

Key highlights of the policy review include:

- The decision of the MPC to continue with the accommodative stance as long as necessary, at least during FY21 and into FY22.

- Forecasts for Consumer Price Index inflation saw an upward revision to 5.2-5.8% for H2FY21 (from 4.5-5.4% provided earlier) and further to 4.6% in H1FY22 (from 4.3% provided earlier for Q1FY22).

- FY21 Gross Domestic Product growth forecast saw an upward revision to -7.5% from -9.5% projected earlier.

- The RBI extended the on-tap Targeted Long Term Repo Operations (announced earlier on Oct. 9, 2020) to cover other stressed sectors of the economy (in line with the recommendations of the KV Kamath Committee) with the credit guarantee available under the Emergency Credit Line Guarantee Scheme 2.0 of the government.

With the central bank having frontloaded its policy accommodation via the trifecta of monetary, liquidity, and regulatory channels since the spread of Covid-19 pandemic in India, we believe the near-term policy outlook will entail nudges and fine-tuning of the desired policy signals with the likelihood of a prolonged status quo like scenario.

However, sooner rather than later, market participants will focus on some of the pertinent issues with respect to factors determining the policy trajectory in FY22. We outline our opinion on some of the critical macro policy challenges facing the central bank.

Is Inflation Being Relegated At The Cost Of Growth?

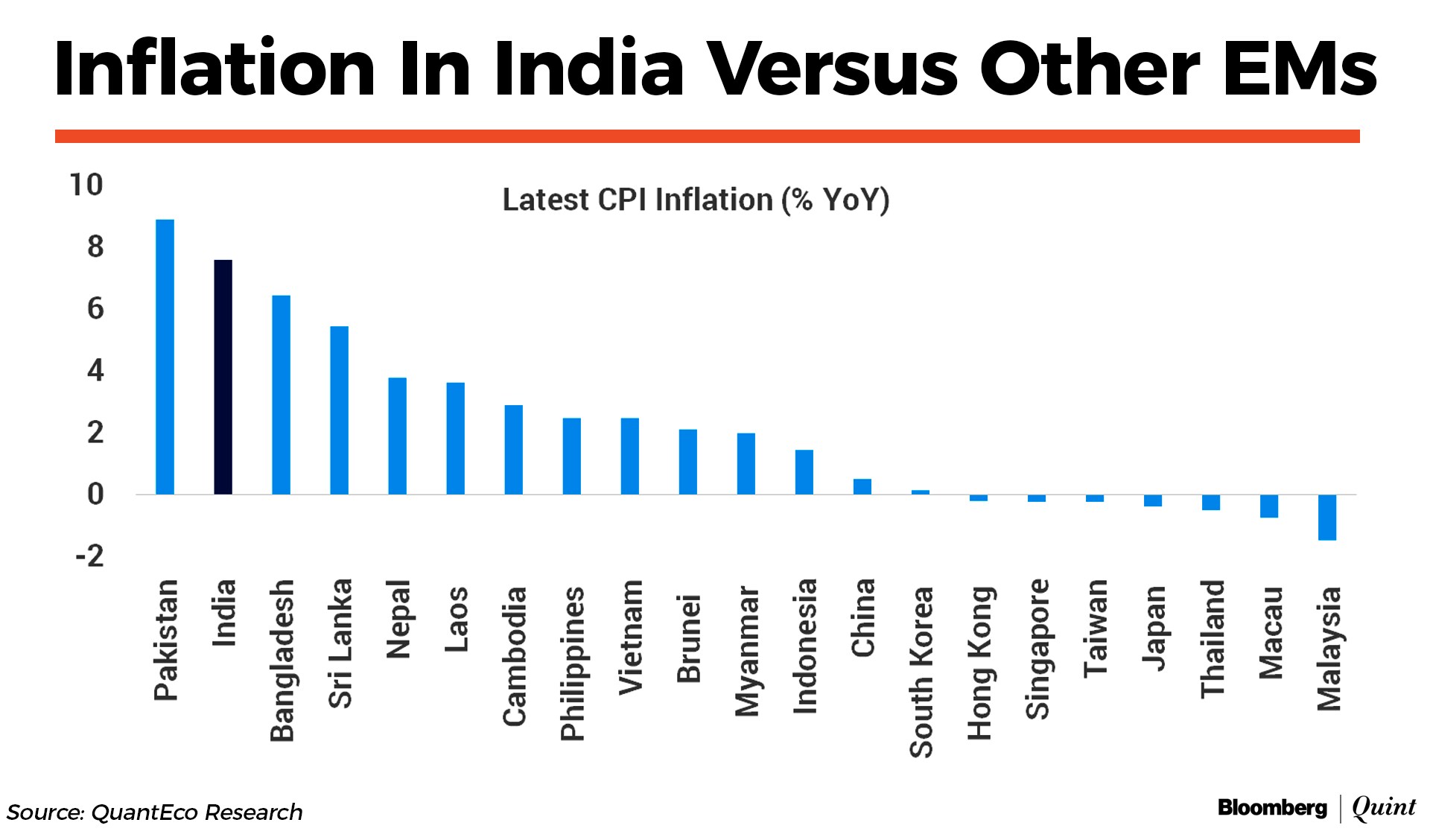

Average annual CPI inflation is projected to be at 6.5% in FY21, piercing the tolerance threshold of 6% for the first time in India's inflation targeting history. India's inflation also happens to be the second-highest in the Asian region currently. While moderation is expected, CPI inflation is still projected to remain above target in H1FY22 at 4.6%.

So why is the central bank ignoring persistent and elevated inflation? There would be no disagreement on the need to support and revive growth from the unprecedented economic and financial shock imposed by Covid-19. Of late, looking-through the phase of elevated inflation by the MPC highlights our belief that the current inflation metric is not a good reflection of on-the-ground price pressures. Past disruptions in the supply chain, phased unlock with consequences for competition, weather idiosyncrasies, and fiscal pressures (duty hikes on fuel) have complicated the conventional inference.

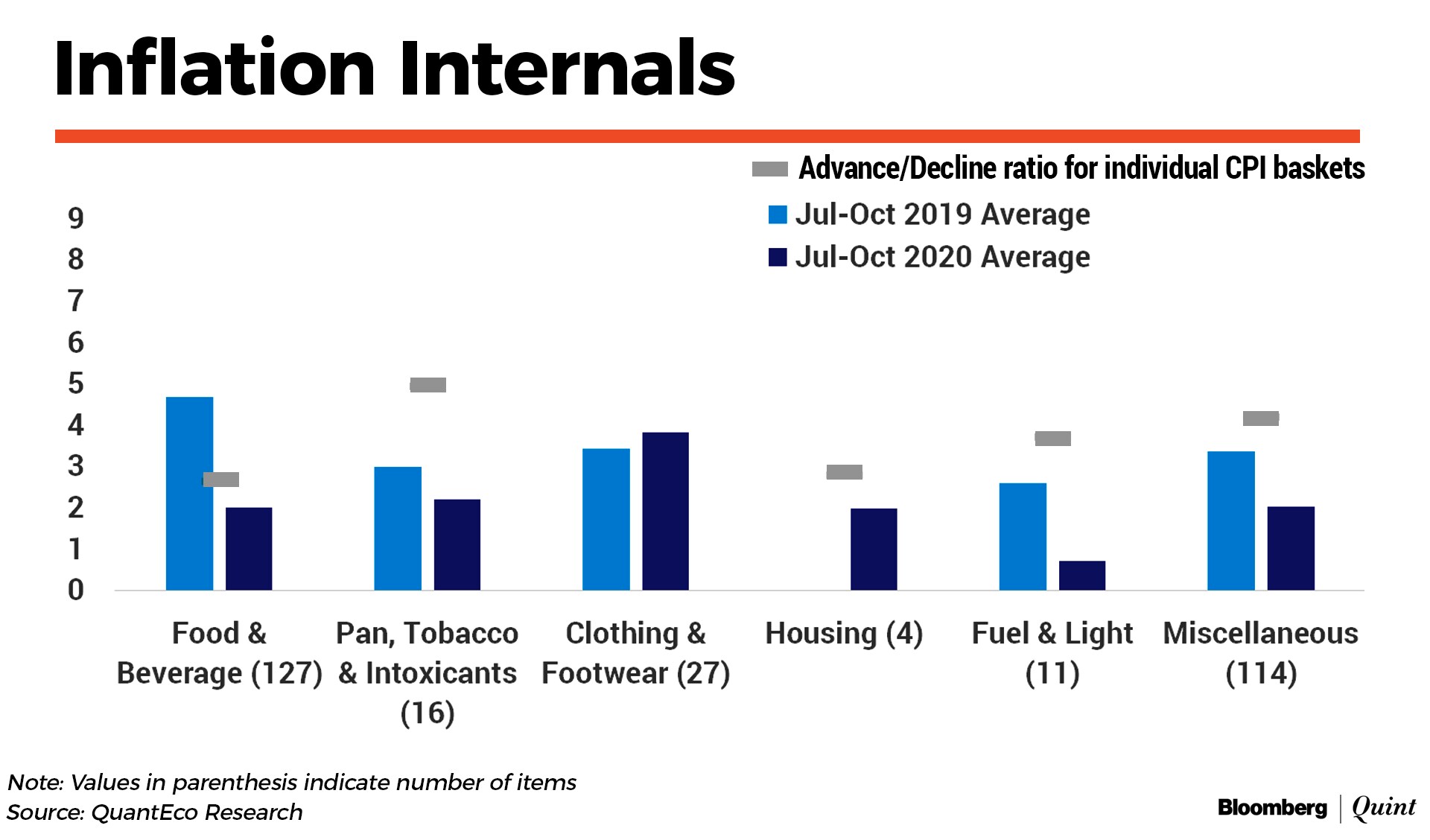

Our analysis indicates that while key metrics of inflation (headline, core, food) are clearly elevated, it is being driven by a few items with overall price pressures still not yet broad-based.

The contraction in private consumption and a rare trade surplus is supporting evidence of the lack of generalised price pressures in the economy.

This resonates with RBI's view of current inflation being idiosyncratic in nature with supply-side factors in the driver's seat. As supplies get normalised in the coming quarters, inflation can be expected to move towards the 3.5-5.5% band in FY22.

Is The Liquidity Glut Distorting Monetary Policy Signal?

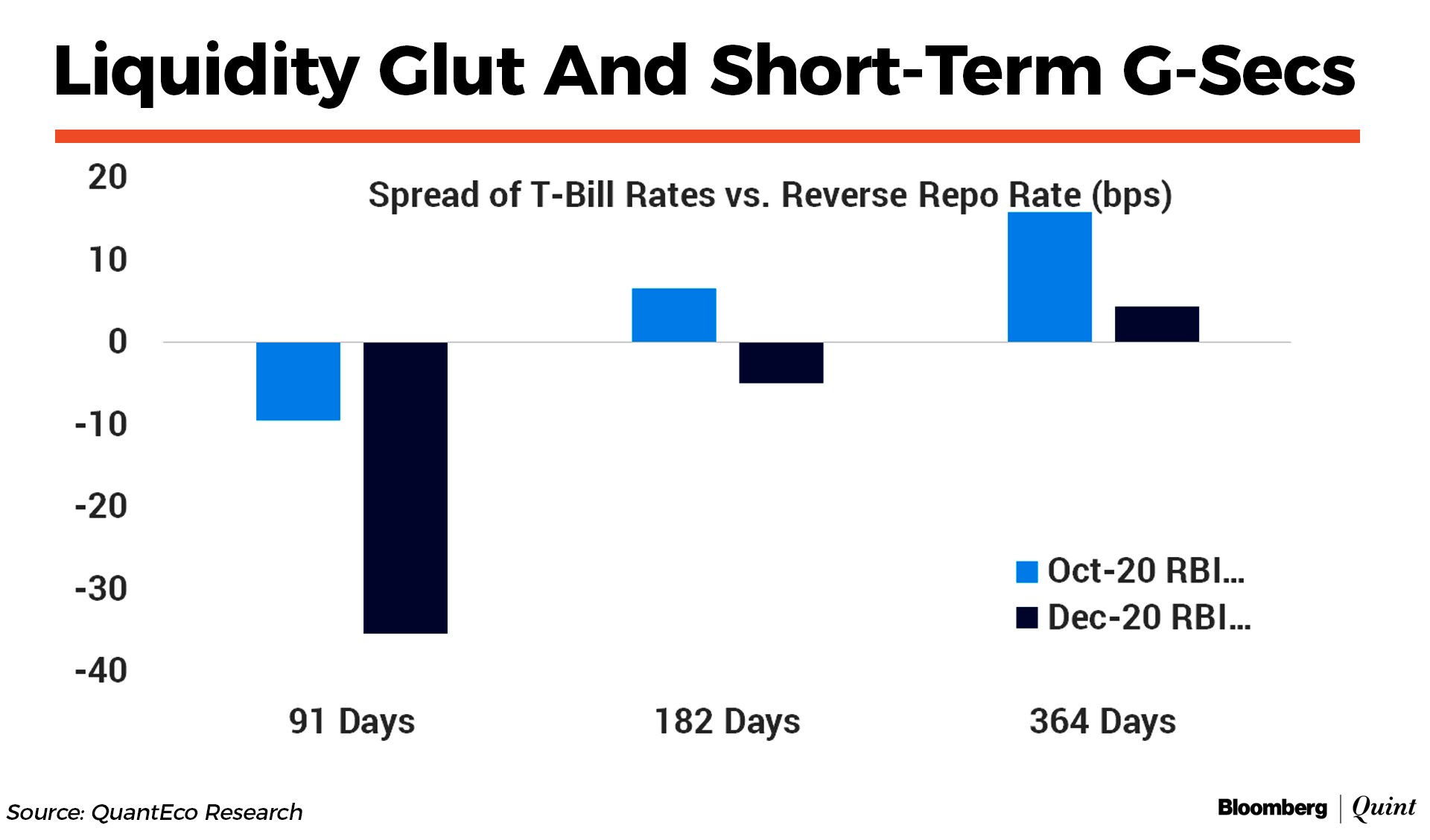

The current liquidity surplus of over Rs 6 lakh crore has created an anomalous situation with few short-term money market rates slipping below the reverse repo rate. The RBI is using the current uncertain backdrop—in terms of growth-inflation-fisc—to maximise its accommodative policy stance and also to ensure that the borrowing pressure from the central and state governments is absorbed in the least disruptive fashion. While we empathise with this objective, the undershooting of short-term rates vis-à-vis the policy corridor if allowed to persist for long is bound to create perverse systemic implications for risk management while also undermining the monetary policy stance, per se.

Although it is early to talk about exit strategies, we believe in the entire policy spectrum, normalisation of liquidity would take precedence for the RBI. The accommodative monetary policy stance can coexist with fine-tuning of liquidity operations calibrated to ensure short term money market rates stay within the policy LAF corridor. The modus operandi could be via a mix of MSS issuances and early normalization of Cash Reserve Ratio. Passive strategies of letting the rupee adjust (appreciate) in line with emerging-market peers and allowing normalisation of trade deficit and cash leakage via currency in circulation to absorb excess liquidity can also be an option, albeit a time consuming one.

In the current uncertain environment, especially with respect to the outlook on capital flows (around 75% of net foreign direct investment flows in H1FY21 is on account of one entity; portfolio flows are dominated by equity with the ultra-loose policy of systemically important central banks providing a push factor), it would be prudent to not rely on one particular strategy and use a mix of all available instruments at disposal.

Would Review Of Inflation-Targeting Framework Alter Monetary Policy Stance?

The government is expected to review the current inflation-targeting framework in March 2021. There are passionate arguments on both sides of the camp, one with respect to the need for tightening the framework in light of the recent experience of slippage, and the other, questioning the framework itself—in light of the shift in the U.S. Fed's embracement of average inflation targeting—and its applicability for emerging market countries like India.

We need to note that since the inception of the inflation-targeting framework, the central bank has delivered consistently, barring FY21, where inflation will see a marked departure vis-à-vis the policy goal.

However, there is room for fine-tuning it by

- Shifting the focus on average inflation rather than point inflation to get rid of inflation volatility emanating from short term factors;

- Refining the CPI basket by incorporating the latest consumption survey weights that are lower for food and consequently higher for non-food items; and

- Including rural housing in the CPI basket.

Riding It Out

In a country like India with sectors at various stages of leverage/linkages/exposure to demand conditions, maintaining a uniform policy environment has always been challenging. The current Covid-19 episode exacerbates some of these challenges including policy dilemmas like the impossible trinity. Hence it is critical to stick to an unambiguous policy goal, ensure adequate degrees of freedom for unknown risks, and ride out uncertainties with minimal disruptions.

With this belief, we would expect the RBI to opt for a prolonged pause while working towards normalising liquidity conditions in sync with the accommodative policy stance. This ought to be followed by restoration of the width of the LAF corridor with the spread between repo and reverse repo rate at 25 basis points. All of this can be achieved in FY22 without an explicit change in the policy stance.

Vivek Kumar is Economist, and Shubhada Rao is Founder, at QuantEco Research.

The views expressed here are those of the authors and do not necessarily represent the views of BloombergQuint or its editorial team.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.