Economy watchers in India will remember vividly the constant debate over the multiple inflation indicators in India and which one should be the focus of policy action. Often in the past, these indicators have diverged, leaving room for interpretation of what the right policy prescription is.

When India formally picked the consumer price index as the nominal anchor for monetary policy in 2014, and then went on to lay down a formal flexible inflation target, it was believed that those debates would end. Policy direction would be clear and based on the level of headline CPI, which the Monetary Policy Committee is mandated to target. In the current cycle that target is set at 4 (+/- 2) percent.

But the debate has come right back, in a direction that most didn't anticipate.

As we head into the monetary policy review on Thursday, the discussion is divided over whether the MPC should focus on high core inflation or low headline inflation, both of which are sending different messages.

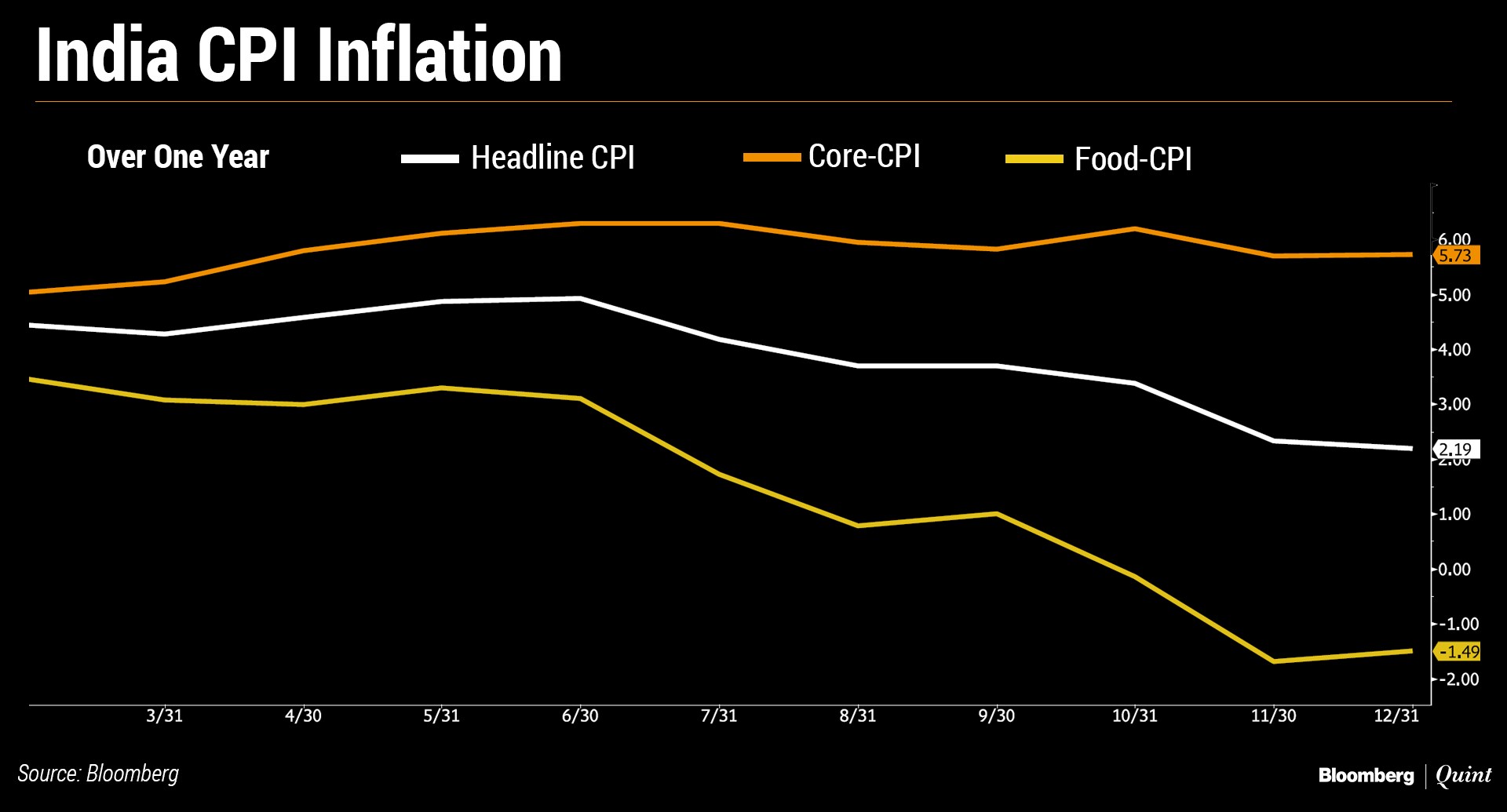

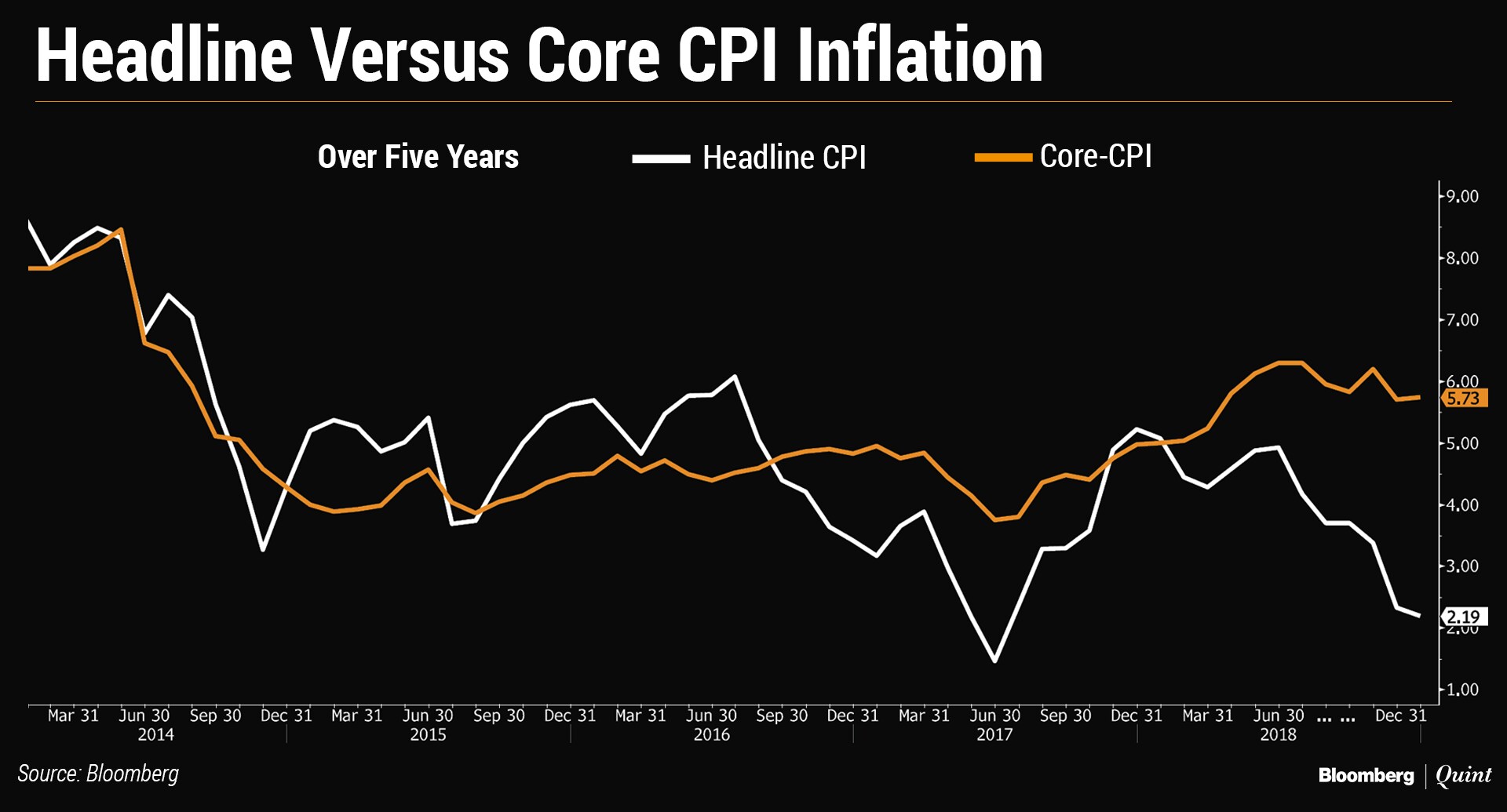

Headline CPI inflation has fallen to 2.2 percent, below the mid-point of the Monetary Policy Committee's target. It has stayed below that mid-point for five consecutive months. Future projections, which are the determinants of policy actions particularly in an inflation targeting framework, also remain modest. Retail inflation is projected at 2.7-3.2 percent in the second half of FY19 and 3.8-4.2 percent in the first half of FY20.

Since the MPC and its members have reiterated a number of times that the intention is to anchor inflation at a level close to the mid-point of the target band, it seems reasonable to expect that the committee could chose to change course and cut its benchmark policy rate. The policy rate, after two consecutive hikes in 2018, stands at 6.5 percent and the monetary policy stance is one of ‘calibrated tightening'.

Headline retail inflation is low almost entirely because of falling food prices. The persistent food disinflation has led to a belief that rural demand conditions are subdued. But if you take out food and the volatile fuel prices, inflation levels tell a different story. This indicator, referred to as core inflation and considered the best gauge of demand in the economy, is still running high at between 5.5-6 percent. In fact, in the last available data for December, core inflation, particularly in the services segment showed an uptick.

Does that suggest that demand conditions are not that soft after all? And if demand is strong and the decline in food prices is due to factors other than demand conditions, then should the MPC keep rates on hold?

Will They? Won't They?

Economists are divided. Not just on the read of the inflation data but also on the strictness with which the MPC will interpret its inflation target linked to headline CPI.

“We have consciously chosen headline CPI as our target, not core inflation. This is unlike other central banks, like the U.S. Federal Reserve that categorically targets the core personal consumption expenditure deflator. For the RBI, it would be difficult to justify a decision that ignores the target and focuses instead on a component of it,” Abheek Barua, chief economist at HDFC Bank wrote in an op-ed published by BloombergQuint on Monday.

Sajjid Chinoy, chief India economist at JPMorgan agrees. “We believe the headline undershoot will be too compelling for the MPC to ignore, given its mandate of keeping headline inflation close to 4 percent on a durable basis,” he said in a note on Saturday following the interim budget announcement. Chinoy's base case expectation is that a rate cut will be announced this week but he admits that it is a close call given the high core inflation.

Pranjul Bhandari, chief India economist at HSBC sees it differently. She expects a change in stance to neutral but no change in rates for now. Over at Nomura, India economist Sonal Varma is also in the camp that believes that current conditions may warrant a change in stance but no rate cut.

On the sidelines of the World Economic Forum, when BloombergQuint put the question about the divergence over core inflation and headline inflation to former RBI governor Raghuram Rajan, he seemed to lean towards the view that caution on rates may be warranted.

The view of course is that core inflation will eventually feed into headline. So someone looking at headline inflation will also look at core and try to understand why it's high. But this is a technical discussion. Broadly speaking, there are still concerns whether we have killed the inflation beast completely. We've come a long way but with core at 5.6-5.7 percent, it's saying something about whether we're at the limits of capacity and whether we can afford to stimulate even more without seeing higher inflation.Raghuram Rajan, Former RBI Governor

So Did We Pick The Wrong Target?

Incidentally, a similar debate had played out in the 2013-2016 period but in a different way.

At that time, food inflation was running high. Some stakeholders argued that monetary policy cannot impact food inflation and hence should not hike rates due to higher food prices. But the RBI was of the view that food inflation feeds into generalised inflation via inflation expectations.

The same case had been argued in the monetary policy framework report of 2014.

“The choice of the inflation metric cannot ignore food and fuel shocks and must, in fact, react to them to avoid a more generalized inflation spiral that influences household expectations lastingly. Not a single EME inflation-targeting central bank targets core CPI – other than Thailand – all of them target headline CPI ,” the committee had argued while recommending that headline inflation be picked as the nominal anchor.

“When we set the inflation target our view was that we did not want to fudge by taking an easier target. We wanted the harder target which at that time was the headline inflation,” Rajan told Bloombergquint in Davos.

The question that the MPC should answer now is whether lower food or fuel inflation has a similar but opposite impact on headline inflation, i.e, will a prolonged period of low food inflation dampen inflation expectations and future inflation? It would also do well to debate a recent paper by MPC member Ravindra Dholakia which questions whether inflation dynamics in India have changed.

For now though, the RBI's decision to target headline inflation will put the MPC in a spot.

“The MPC will have a very difficult time trying to decide whether they should stick to the headline inflation of 2 percent, which would suggest that inflation is under control versus the fact that core inflation has been rising relentlessly,” said Jahangir Aziz, chief emerging market economist at JPMorgan in a recent interview with BloombergQuint.

The MPC cannot be giving out a message that it is targeting core inflation when its target is headline inflation, added Rajeev Malik, strategist at River Valley Asset Management. While there are a lot of different aspects to inflation at this stage, “the bottomline that the MPC needs to understand is that its legally mandated target is the headline CPI,” Malik said.

Ira Dugal is Editor - Banking, Finance & Economy at BloombergQuint.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.