I took my home loan in 2014 from a public sector bank. Please don't ask me why, everyone is entitled to irrational decisions once in a while. Let us call this bank the Bank of Bunglers and move on with my story.

Among the many accidents that they caused, they once accepted a pre-payment from me, and proceeded to adjust it monthly against my EMIs! To even conceive that such a thing can be done requires some level of aptitude. Anyway, upon discovery, like in the myth of Sisyphus, I embarked on the near impossible journey of getting the transactions reversed. The helplines were anything but helpful; the email ID that belongs to no-one-in-particular, chose to leave my correspondence unanswered; social media tags were met with templated messages. After I finally succeeded, I got fatigued and busy with work but I nursed the intention to move to another bank, soon.

Since 2014, policy interest rates had come down significantly and Bank of Bunglers had unsurprisingly, not transmitted them. At one point, I decided to approach another bank. Their officer gave me the necessary paperwork which included a ‘No Objection Certificate. When I approached Bank of Bunglers in person, the man whom the no-one-in-particular email ID belonged to, emerged and identified himself as the branch manager. My rates were reduced with unusual speed as well. Naturally, I had to return the favour, so I returned home with an unsigned NOC.

You may judge me all you like and I am not particularly proud of myself either. However, this is now case study material for the behavioural finance class I take with management students. So I have lent some dignity to my behaviour after all. In case you didn't know, financial decisions are often irrational in nature and in this situation, I was exhibiting ‘biases', all well documented in the field of behavioural sciences.

In exhibition of this inertia, I am not alone. Here are some statistics.

Financial services customers, all over the world, are unexpectedly sticky. Depending on the industry, the annual customer defection rates in many countries is about 20 percent, that is one-fifth. Financial institutions on the other hand, lose about 10 percent of their customer base every year and in some categories, the figure is less than 5 percent.

For the purpose of my course, I have looked at this information from a marketeer's lens, but imagine what that means to you and me as customers.

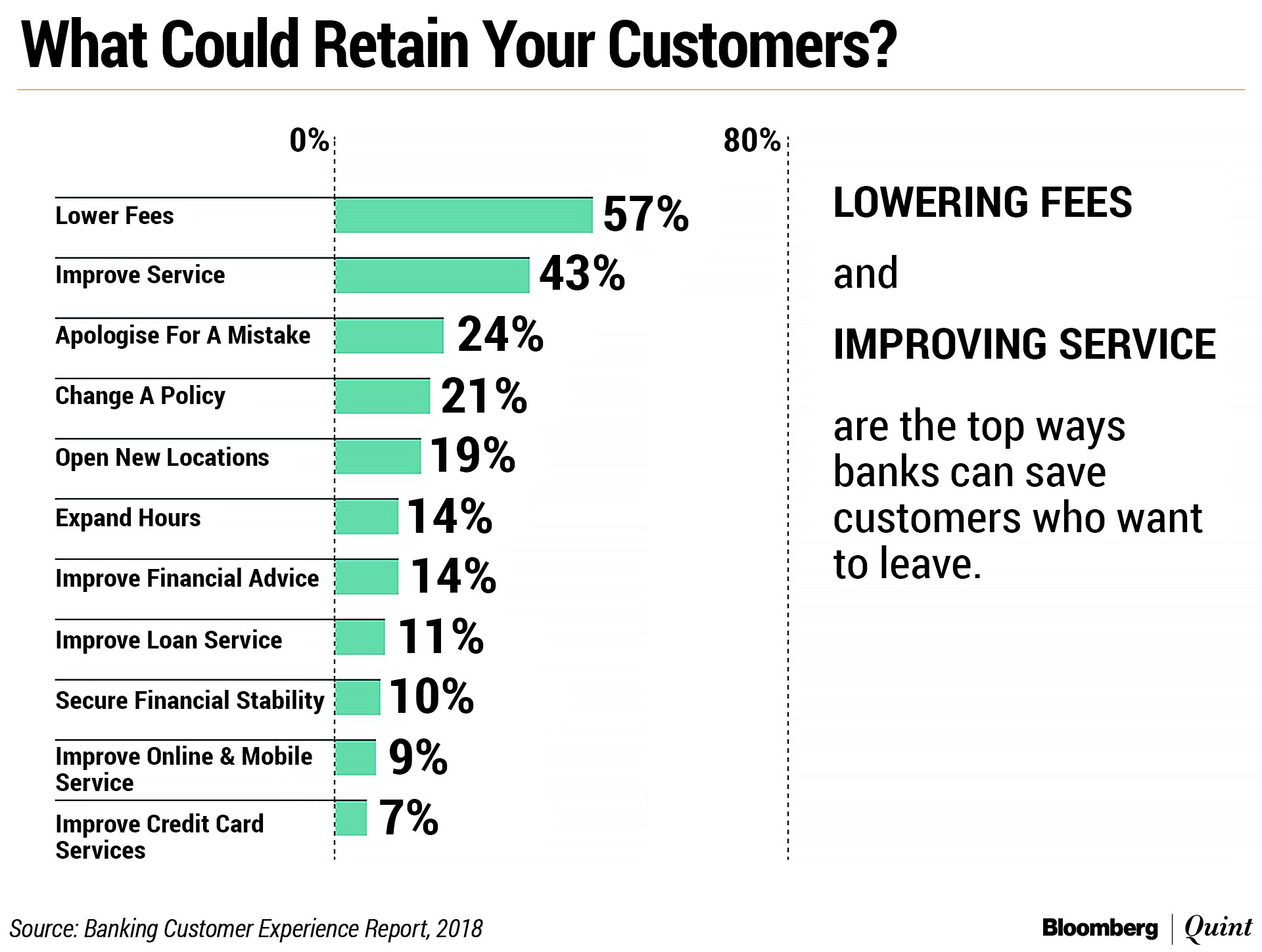

In the Banking Customer Experience Report, 2018, 56 percent of respondents who actually left the bank, answered they would have stayed if the Bank made any effort to retain them. The efforts could be in as many directions as follows:

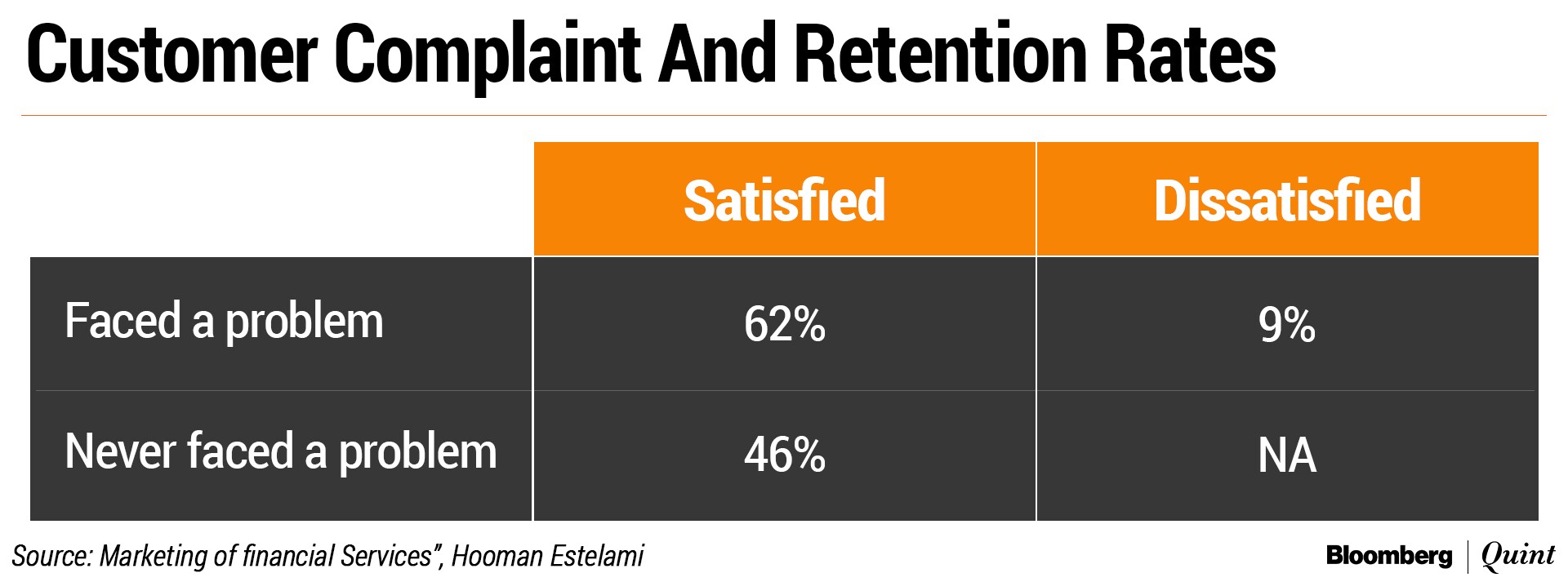

What is more, if they got down to complaining, the chances of retention went up significantly:

Now let us examine why customers have this inertia after all.

1. Shifting Is Overwhelming And Time-Consuming

Related transactions can be intimidating too. Imagine, if you wanted to shift your primary bank, how many steps you would have to take to ensure everything ran smoothly thereafter; from auto debits to signing up new beneficiaries, managing new cards, changing redemption mandates for life insurance policies, mutual funds. It could be a potential avalanche.

Smart marketeers know this well and encourage that you use the bank for multiple purposes.

2. Too Little Differentiation

There are too many price points in a financial product – interest, processing fee, pre-payment fee, average balances, penalties. Then there is a service level which can only be perceived at the time of purchase and lived thereafter. “Is this worth my time and energy” is bound to pose itself as an important question.

3. The Endowment Effect

Familiarity, which psychologists call the ‘endowment effect'. Something that you own attains a certain level of significance for you. If you didn't own it, perhaps you wouldn't care much for it. In this case familiarity breeds possessiveness, with or without contempt!

4. Sunk Cost Fallacy

These are expenditures made, that prompt you to make further expenditures simply because you are not willing to accept that your first expenditure was a mistake to begin with. We are all familiar with how we ignore the costs of inconvenience, time and even money to step out during bad weather if we have bought expensive tickets to a play or concert. The same is at play with our banking relations.

5. Irrational Escalation Of Commitment

This is very similar to sunk costs. Is that not why we keep repairing our old car, no matter how much trouble it gives us? In financial services, this feeling is extremely common, especially in long term commitments like Insurance, home loans and even SIPs!

While you reflect on your own behaviour as a customer, let me end with a small note for marketeers, lest they feel all powerful and start basking in glory after signing people up.

Attrition, when it happens in financial services, is silent and invisible.

There is a vast body of knowledge around this stickiness and how competition works overtime to break customer inertia.

Hooman Estelami, in his scholarly paper, elucidates that the cost of acquiring a new customer may be five times the cost of handling a disgruntled customer. But for that, one must find the disgruntled customer.

This entire subject of customer loyalty is as intricate and tricky for the customer as it is for the financial services brand. So, go along, encourage your clients to complain and leap at every chance to delight and retain them.

Abaneeta Chakraborty has close to two decades of experience in managing money for ultra-HNI families. She founded the firm Abanwill Consultants LLP in 2017 to provide independent views on investing.

The views expressed here are those of the author and do not necessarily represent the views of BloombergQuint or its editorial team.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.