The concept of ‘promoters', or controlling shareholders, has acquired a pivotal status in the Indian corporate governance discourse. Promoter status is not permanent, but transient. A promoter that cedes control over the company is expected to shed both the privileges and burdens of the status. Some questions have come into sharp focus in such a circumstance. Who enjoys the power to trigger the reclassification of a promoter as a non-promoter (or public) shareholder? Is it the company or the promoters themselves?

While the company earlier had considerable latitude, upon a loss of promoters' control, in initiating the process to reclassify them as public shareholders, the current dispensation transfers this power into the hands of the promoters themselves. This has stirred up a hornet's nest as promoters who have involuntarily lost control of their companies are clutching at straws by refusing to shed their promoter status, thereby calling into question the efficacy of the current legal regime.

Power To Companies: Subjectivity

The Securities and Exchange Board of India governs promoter reclassification through regulation 31A of the SEBI (Listings Regulations and Disclosures Requirements) Regulations, 2015. This provision specified a series of scenarios where a promoter could be reclassified as a public shareholder. More importantly, companies, as well as their promoters, enjoyed the power to initiate a reclassification. However, snags soon surfaced. Companies and promoters flooded SEBI with requests for informal guidance.

It turned out that regulation 31A was under-inclusive.

- It did not encompass all situations pertaining to a promoter's loss of control, such as when a designated promoter—for example, a family member of a key shareholder-director—was simply not involved in the affairs of the company and only held a minuscule number of shares.

- Not all types of reclassification required the approval of the shareholders. SEBI too adopted a rather liberal approach in granting informal letters. It began approving reclassifications on grounds extraneous to those specified in the legal provision. Moreover, it allowed reclassifications without shareholder approval.

There was a sense that it was simply too easy for promoters to be reclassified as public shareholders. Either the company or the promoters could initiate the process, that too on a range of somewhat subjective grounds that exceeded the regulatory prescription and bypassing the shareholders. One can fathom the resultant consternation.

Reform Process

This caught the attention of the Kotak Committee that undertook corporate governance reform. Taking a cue from the uneasy experience until then, it recommended a comprehensive set of circumstances in which promoter reclassification can occur, all of which necessitated shareholder approval. Most relevant for purposes of this discussion, there was a suggestion that reclassification be initiated only upon request from the promoters. A subsequent SEBI consultation paper on the reclassification of shareholders observed that unilateral action on the part of the companies without a specific request from the promoters was “prone to misuse”. Hence, SEBI received vociferous recommendations that reclassification be permitted only upon the request of the promoter to the listed entity.

Accordingly, in November 2018, SEBI put regulation 31A to a major overhaul. It comprehensively set out the circumstances in which promoters can apply to be reclassified as public shareholders, thereby seeking to eliminate the erstwhile subjectivity. It made shareholder approval by ordinary resolution mandatory for all types of reclassification. Promoters can seek to be reclassified only if the following conditions are satisfied:

- Promoters together do not hold more than 10 percent voting rights;

- They do not exercise direct or indirect control over the listed company;

- They do not have any special rights through a formal or informal arrangement, such as through shareholders agreements;

- They are not represented on the board by nominee directors;

- They do not act as a key managerial person;

- They are not ‘wilful defaulters' under relevant guidelines of the Reserve Bank of India;

- They are not a fugitive economic offender.

Note that all of these requirements are attributes of the promoters, and must be satisfied cumulatively.

The promoters' own status measured against these criteria would help determine whether they can rid themselves of the promoter tag.

Finally, regulation 31A now clearly states that the reclassification process can commence only if the promoter requests the listed company to do so. The procedure is entirely promoter-driven, and incapacitates the listed company, acting through its board, from initiating a reclassification of its promoters.

Unduly Restrictive Regime

If the erstwhile position was that regulation 31A was too liberal in facilitating promoter reclassifications, the pendulum has indeed swung, and that too far afield, in that the current dispensation makes promoter reclassifications rather cumbersome.

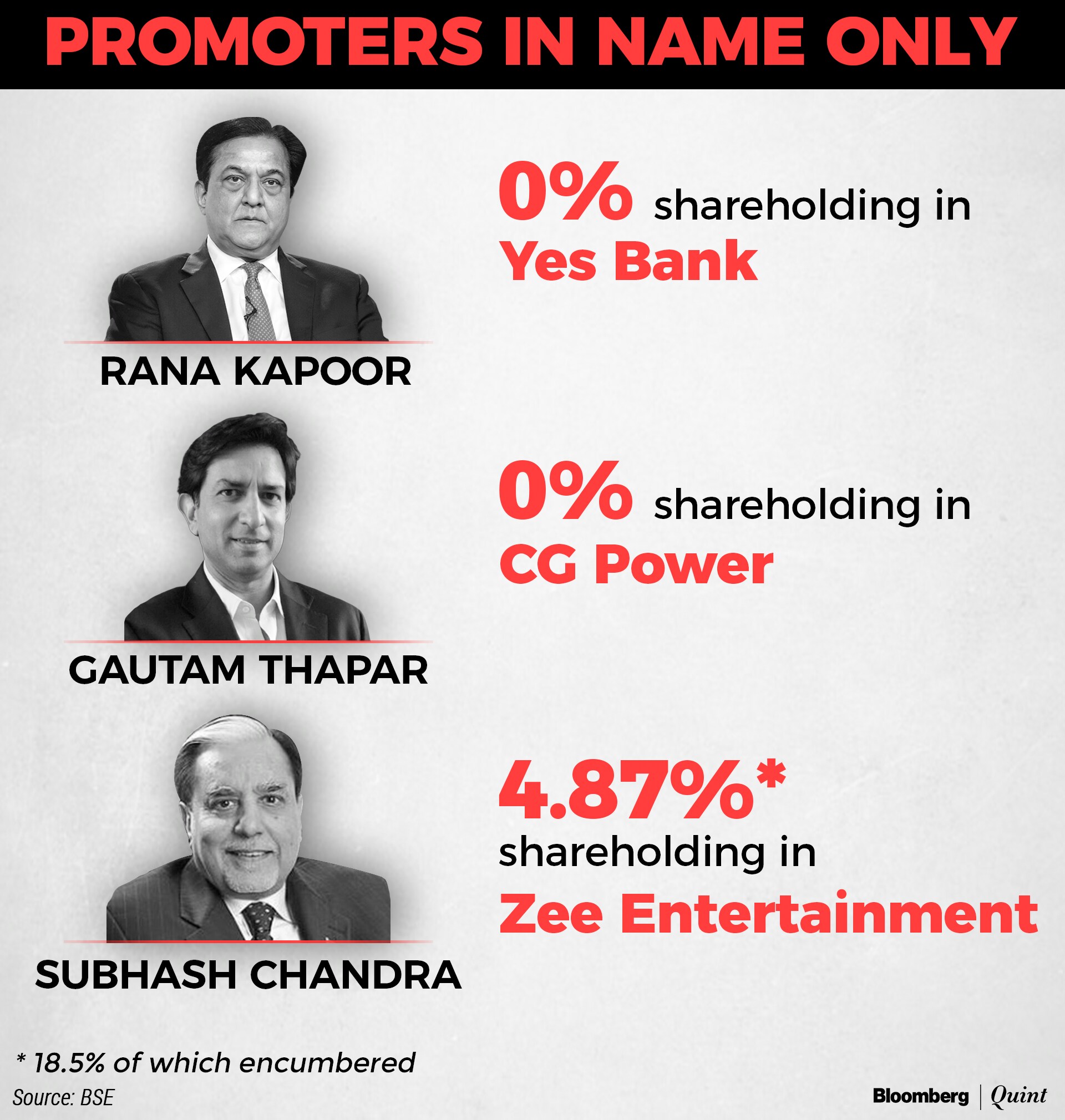

Promoters therein have suffered substantial dilution of their shareholding for a variety of reasons, including the fact that they had pledged a large portion of their shareholding to banks and financial institutions, who enforced their security interest. Although these individuals and entities now hold only an infinitesimal number of shares, the law continues to treat them as promoters, thereby leading to an abject incongruity.

The present regulation 31A rests on two assumptions, which appear unfounded.

First, the current reclassification process rests on the footing that promoters will be keen to go out of the company's door once their role becomes marginalised in terms of both shareholding and management control. However, that may not be true when the relegation of promoters in their company's architecture occurs involuntarily for reasons beyond their control. The recent cases involved promoters losing control due to the enforcement of pledges on their shares, or because of a boardroom coup.

An ostracised promoter hardly has an incentive to go through the motions of reclassification, without which the process stands stymied.

Second, since being a promoter is associated with significant legal burdens and associated liabilities, there is an expectation that a diluted promoter will want to exit from that status, and hence a reclassification will work itself out. Although there is some merit in that line of thinking, such a sequence is unlikely. Promoters relegated to the fringes in an endgame scenario would be less concerned about the legal burdens of promotership. After all, they have no skin left in the game and they suffer from moral hazard. On the contrary, the company will be keen to dissociate itself from such a promoter, but its hands are tied, leaving it in a vulnerable position.

This conundrum is evident from the plea of the new chairman of CG Global to his shareholders in a letter accompanying the annual report for 2018-2019: “your Company considers any further association with … the promoters, as prejudicial to the interests of your Company and its stakeholders”. The regulations as they currently stand do not provide a clear escape route for the company.

Additionally, since the conditions relate to the promoter's status rather than the company's, peculiar situations could ensue.

A marginalised promoter who is a wilful defaulter or a fugitive economic offender cannot reclassify as a public shareholder, leaving the company to bear the adverse reputational consequences.

This discussion demonstrates that the current measures for promoter reclassification make it extremely difficult to achieve a change in status, a far cry from the earlier scenario where it was too easy. Perhaps the answer lies somewhere in between.

Way Forward

Cognisant of the prickly issues at hand, SEBI has indicated that it is reviewing the regulations pertaining to promoter reclassification. The review process must incorporate these and other lessons. It calls for a well-considered long-lasting solution as opposed to the flip-flop we have witnessed overall. The current rigidity calls for some moderation. For example, it should be open to a company to initiate reclassifications in cases where the promoter suffers an involuntary dilution or does not satisfy one of the conditions that are attributable to the promoters' acts and not the company's.

SEBI's chairman has also announced a broader review of the concept of promoter as a whole and suggested a shift to “controlling shareholders” instead. One hopes that the reform underway is holistic in nature and not merely a superficial rebranding exercise, lest the concept of promoter becomes more of an untameable beast than it already is.

Umakanth Varottil is an Associate Professor of Law at the National University of Singapore. He specialises in company law, corporate governance and mergers and acquisitions.

The views expressed here are those of the author and do not necessarily represent the views of BloombergQuint or its editorial team.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.