On September 22 1998, a senior Goldman Sachs executive telephoned the then Chairman of the Federal Reserve Bank of the United States, Alan Greenspan. He sounded a warning about an impending collapse of a large hedge fund called Long Term Capital Management (LTCM) which could trigger a ripple effect on the stock market and the broader economy. The Federal Reserve immediately dispatched a set of officers to the LTCM office who parsed every transaction in its books and concluded that LTCM needed an additional $4 billion for a smooth landing. The Fed then summoned the heads of sixteen banks that were creditors to LTCM. To their utter dismay, the banks were categorically told to drum up an additional $4 billion in loans to LTCM. The Fed even oversaw the haggling process of how to divvy up the amount among these 16 banks and finally ensured a safe landing for LTCM and the economy.

This incident is worth recalling in the context of the recent ordinance of the Government of India that gives the Reserve Bank of India more powers to resolve the non-performing assets (NPA) crisis in the banking sector. Essentially, the ordinance grants powers to the RBI to intervene and resolve the problem of NPAs. One could argue that the RBI had such broad powers already but in the context of India's new Bankruptcy Code legislated last year, this ordinance specifically grants powers to the RBI to initiate such bankruptcies of banks, in cases of default. More philosophically, the ordinance puts the onus of resolution of NPAs on the RBI. The government is urging the RBI to take a leadership role in resolving the NPA crisis that has festered for so long.

As an example, if there was a distressed loan of the State Bank of India that needed to be sold at twenty paise to the rupee to be taken off SBI's books, the SBI board, today, is reluctant to sign off on this sale since it is unsure of the price of the impaired asset and the “fit and proper” character of the buyer.

In other words, the SBI board is wondering if the asset is being sold too cheap and to someone who is potentially colluding with the current borrower to buy back this asset at the cheapest price possible.

This can be a fit case for investigation by the “C Trinity” – Central Bureau of Investigation, Central Vigilance Commission, and Comptroller and Auditor General. Now, with the ordinance, potentially a RBI empowered committee or team can certify the price and the buyer, which would insure the SBI board against future claims of negligence or mala fide intent and help it approve the resolution process.

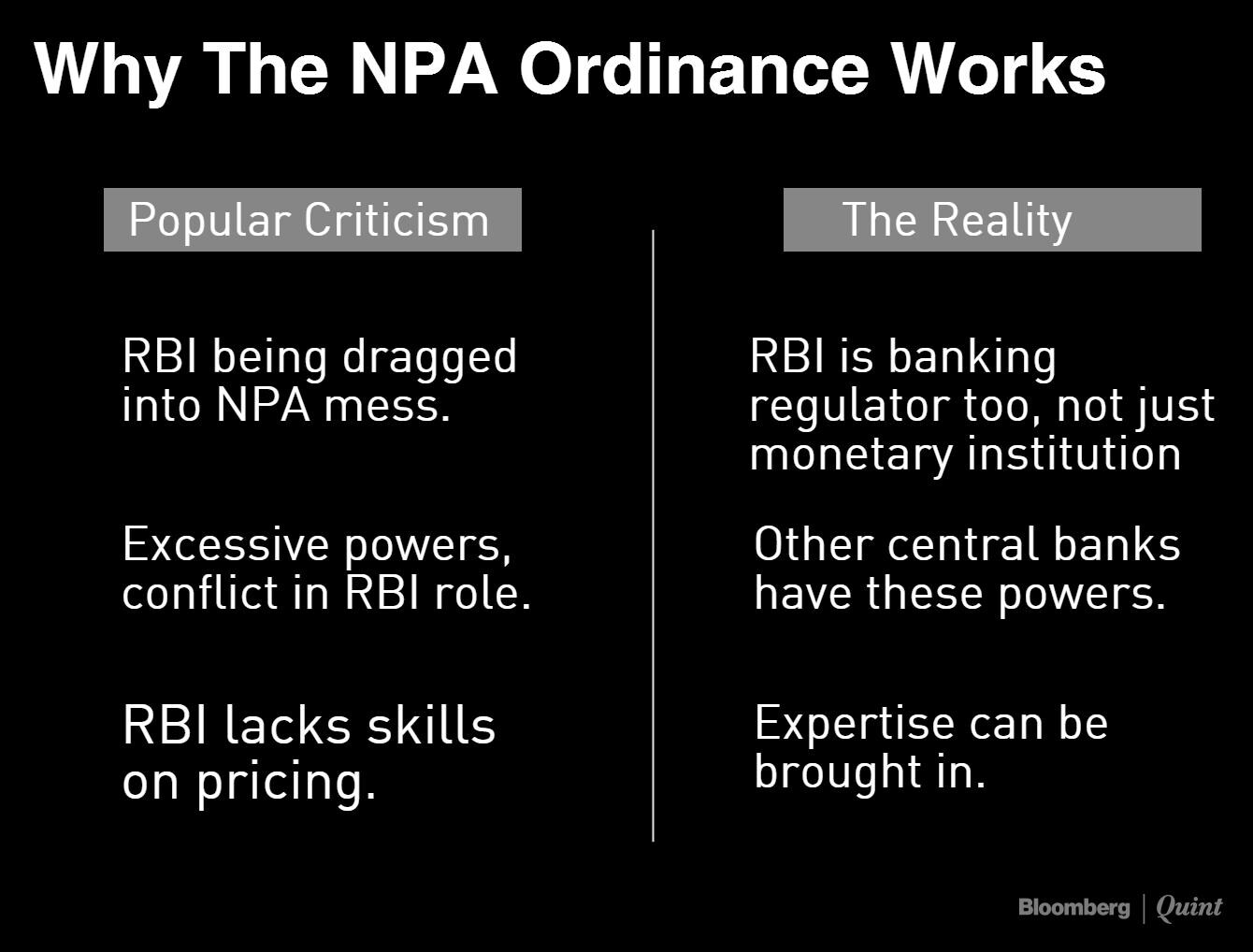

The ordinance has attracted criticism from several quarters. The criticisms broadly fall in three buckets:

- The RBI is being needlessly dragged into resolving NPA problems.

- The RBI is now being given excessive powers to intervene in commercial and operational decisions of the banks which presents a conflict with its supervisory role as a banking regulator.

- The RBI does not have the skills to price distressed assets and make commercial decisions.

Also Read: RBI Steps Into The Bad Loan Minefield

Central Banks Lead From The Front During Crises

The first criticism carries an underlying premise that the RBI is too pristine and should not sully its hands in nuisances of bad loans but rather stick to dictating interest rates for the country and leave the handling of these bad loans to others. The RBI is the banking regulator of the country. The banking system is in a crisis. The RBI should be at the forefront of the resolution of this crisis and not a mere bystander. As the LTCM example cited above shows, central banks across the world have a history of leading from the front in resolution of asset crises in the banking sector. So, the criticism that the RBI is being “dragged in” does not hold water.

Powers That Other Central Banks Have Exercised For Decades

The second criticism of RBI being granted excessive powers is also misleading. This is an emergency measure and the ordinance clearly states that the RBI can recommend insolvency only in the case of a default. If the RBI were to take the initiative in bringing various stakeholders together and use its powers to force a decision on resolution of NPAs, it is still a far cry short of the practices of central banks globally in times of crises, as we saw in the LTCM story. If it is indeed true, as is widely believed, that the RBI's institutional credibility and integrity is of the highest order, then this process leverages that reputation to resolve India's NPA crisis. The RBI with its stellar reputation can now oversee a process to price and sell impaired assets of banks. What the RBI has been empowered to do is in no way any more egregious than what most central banks across the world have been empowered to do and exercised for many decades. It should also be remembered that the government is the owner of most of the banks that are saddled with massive NPAs.

So, it is in fact better for the RBI to be the resolution agency for these NPAs than the government, which would then present a principal – agent conflict.

Also Read: Empowering RBI To Clean Up The Bad Loan Mess. Will It Work?

Bringing In The Required Skills

The third criticism that the RBI does not possess the skills to price distressed assets and make commercial decisions is perhaps a valid one. But skills can always be brought in laterally through expert groups and committees set up under the auspices of the RBI. Presumably this is a temporary measure until the NPA crisis is resolved and hence the RBI can always supplement skills through outside experts temporarily.

All in all, India's NPA crisis has remained unresolved for so many years not for lack of desire or ideas or technical solution but for the problems posed by the “C Trinity”. This ordinance is clearly aimed to circumvent the “C Trinity” deadlock. It remains to be seen if this will break that deadlock but it is certainly a laudable attempt. To be sure, this is just the first step in the actual resolution of India's banking crisis. If this works, then the big question still remains about recapitalization of the banks once impaired assets have been taken off its books. But for now, this ordinance is a welcome step, perhaps an extraordinary measure but we also live in extraordinary times.

Praveen Chakravarty is a Senior Fellow at IDFC Institute, a Mumbai-based think/do tank. His work focuses on financial sector legislation & political economy.

The views expressed here are those of the author's and do not necessarily represent the views of BloombergQuint or its editorial team.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.