The Central Board of Direct Taxes unveiled new Income Tax Return forms for Assessment Year 2018-19 on April 5. Although the manner of filing returns remains the same as compared to last year, certain changes have been incorporated in the new ITR forms. The fields in the ITR forms have undergone changes in many places, seeking more details from taxpayers than they did in previous years.

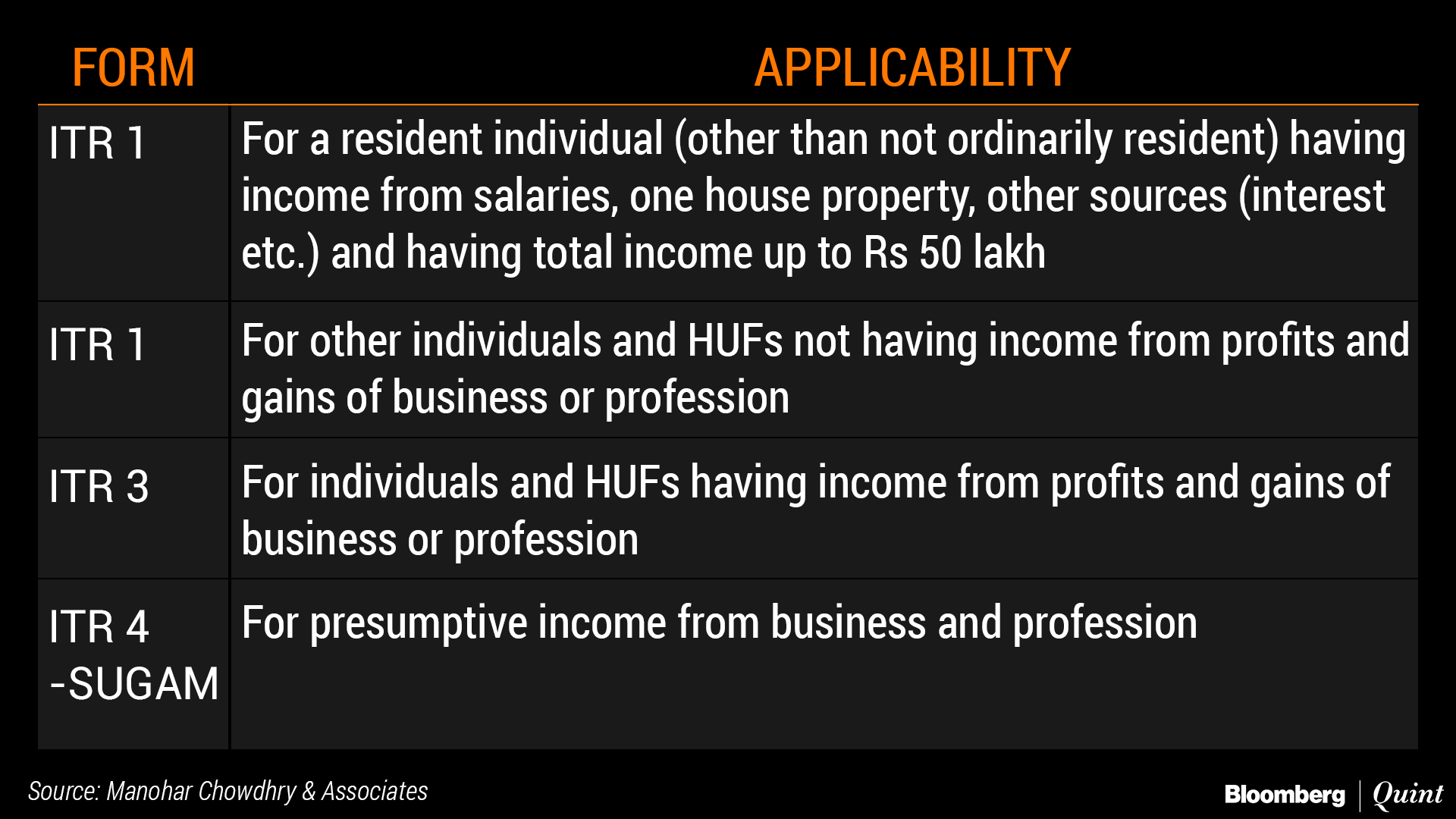

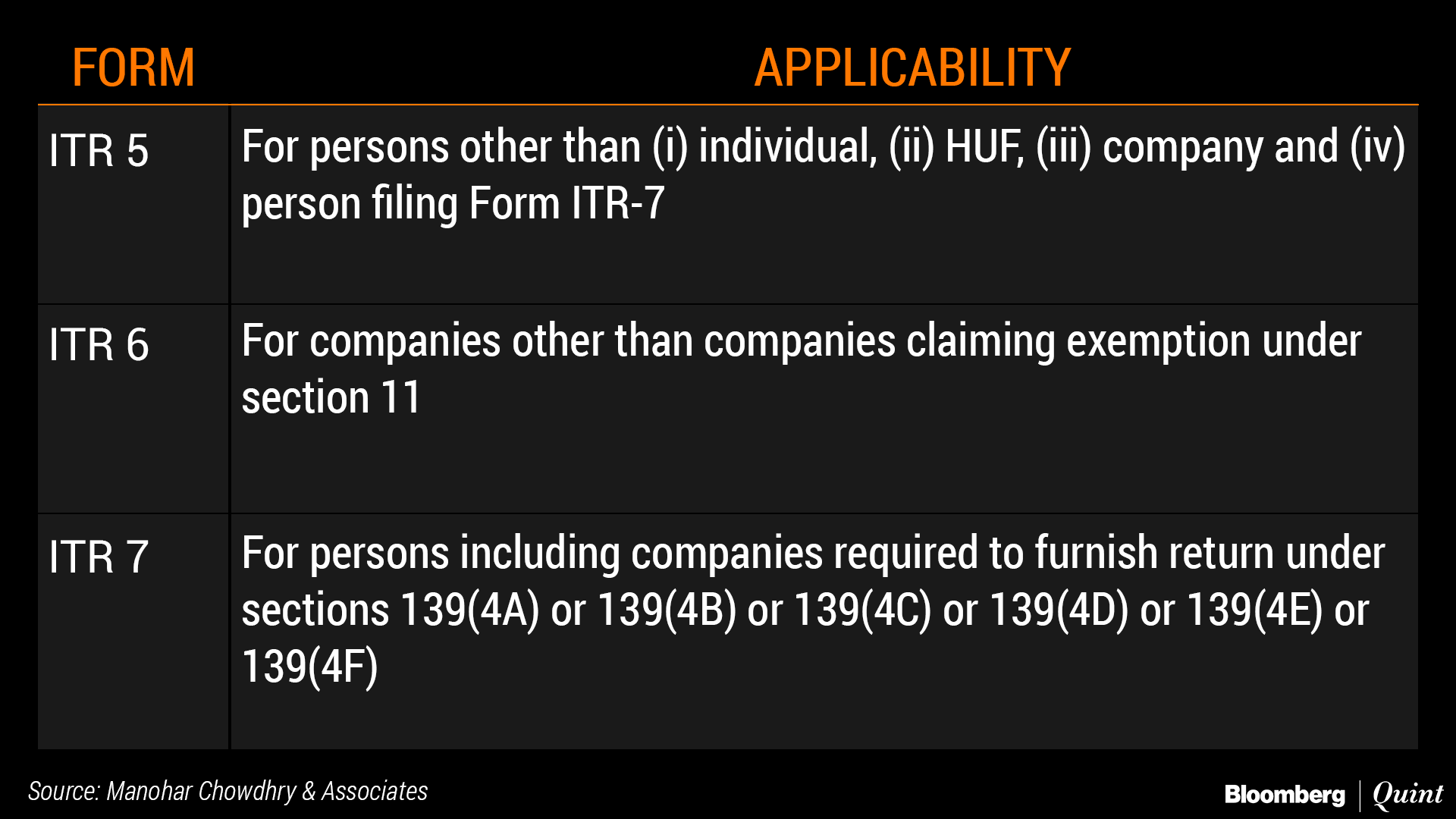

In terms of applicability, the following table lists out the different forms and to whom each category is applicable:

Here are key changes in the ITR Forms for Assessment Year 2018-19.

Gender Under Personal Information

The ITR forms 2,3 and 4 for the previous year required the taxpayer to specify their gender i.e. Male, Female or Transgender. However, the field for the same has been withdrawn from the current ITR forms.

Bank Details Under Details Under Other Information

Information regarding cash deposited—subsequent to demonetisation—which was introduced in the ITR forms in AY 2017-18, has been withdrawn from ITR 1 to ITR 7 for the current assessment year as that information pertained to the specific time period of Nov. 9 to Dec. 30, 2016. Further, non-residents are allowed to furnish details of any one foreign bank account for the purpose of payment of income tax refund. Earlier they were allowed to provide details only pertaining to bank accounts in India. This change pertains to ITR 2 to ITR 7.

Detailed Reporting Of Salary And House Property

ITR 1 and ITR 4 require taxpayers to furnish a break up of income from salary and income from house property as against the previous year where only the final taxable figures were to be specified.

Consequently a few additional rows have been added to report the value of perquisites, profit in the lieu of salary, taxable allowances and deductions under Section 16 in case of income from salary and the gross rent, tax paid to local authorities, interest payable on borrowed capital in case of income from house property.

This change is in line with the recent initiatives of the tax department to try and match as many figures of an ITR form as possible with data obtained from other sources (TDS returns, Statement of Financial Transactions etc.).

Late Filing For Return Fees: Section 234F

The Finance Act, 2017 introduced a new fee under Section 234F if the taxpayer did not furnish the return of income on or before the due dates prescribed under Section 139(1). The fees shall be levied as under:

- Rs 5,000 if the return is furnished after the due date but before December 31 of the assessment year [Rs 1,000 if total income is up to Rs 5 lakhs].

- Rs 10,000, in any other case.

A new field has been incorporated in ITR 1 to ITR 7 wherein the assessee has to furnish the details of the late filing fees.

Schedule For Capital Gains: Transfer Of Unlisted Shares

In accordance with the new section introduced by the Finance Act, 2017 pertaining to the transfer of unlisted shares, consideration shall be deemed to be the price calculated by a merchant banker or a chartered accountant on the valuation date if the transfer price is less than its fair market value.

The taxpayer is required to provide the following details in the new ITR Forms i.e. ITR 2, ITR3, ITR 5, ITR6 and ITR 7:

- Actual sales consideration;

- FMV as determined in a prescribed manner;

- Deemed full value of consideration (higher of A or B).

Further, specific columns have been introduced to record the capital gain exemptions separately in their respective columns of the ITR forms.

Schedule For Income From Other Sources: Gift

As per section 56(2)(vii), any sum or property received by an Individual or an HUF without any consideration or for inadequate consideration (in excess of Rs 50,000) shall be taxable as ‘income from other sources'. The Finance Act, 2017 widened the scope of this section with clause (x) to section 56(2) whereby the provision is made applicable to all taxpayers. Therefore, new fields have been introduced in ITR2, ITR 3, ITR 5, ITR 6 and ITR 7 for reporting the same.

Assessees Opting For Presumptive Taxation Under Section 44AD, 44ADA Or 44AE

ITR 4, to be filed by taxpayers opting for presumptive taxation, now requires furnishing details of secured loans, unsecured loans, advances, fixed assets, capital account etc. under financial details of a business, in addition to the previous requirement of total creditors, total debtors, total stock in trade and cash balance.

ITR 4 also seeks details of the amount of turnover or gross receipts as per the GST return filed by the taxpayer.

Assessees Eligible To Claim DTAA Relief

The new ITR 2, ITR 3, ITR 5 and ITR 6 require furnishing the following additional details from taxpayers claiming DTAA relief under capital gains and income from other sources schedule:

- Rate as per the treaty;

- Rate as per income tax;

- Section of the Income Tax Act;

- Applicable rate [lower of (a) or (b)].

Impact Of ICDS And Additional Details Of GST

The new ITR 3, ITR 5 and ITR 6 require taxpayers to report the impact of ICDS on the profit and loss separately in the three schedules namely Schedule OI, Schedule BP and Schedule ICDS. Simply speaking, it prohibits reporting only the net impact on profit and loss of ICDS in Part A of the other information schedule like the previous year.

The ITR 3, ITR 5 and ITR 6 have also introduced new fields to furnish details regarding CGST, SGST, IGST or UGST paid by or refunded to the assessee.

Details Of TDS

New columns have been introduced in ITR 2 to ITR 7 in order to assist the department to verify the PAN, amount of income and TDS thereon as disclosed by both the parties in their respective return of income. The 2 columns included in the TDS schedule deal with:

- TDS deducted in the hands of any other person as per rule 37BA (2);

- TDS claimed in the hands of any other person as per rule 37BA (2).

Income From Other Sources: Carbon Credits

Carbon credits is an incentive given to an industrial undertaking for reduction of the emission of greenhouse gases, including carbon dioxide. A reduction in emissions entitles the entity to a credit in the form of a Certified Emission Reduction certificate. The CER is tradable and its holder can transfer it to an entity which needs carbon credits to overcome an unfavorable position on carbon credits.

Accordingly, a new section has been inserted in the Finance Act, 2017, Section 115BBG whereby any income from transfer of carbon credit shall be taxable at a concessional rate of 10 percent (plus applicable cess and surcharge). The new ITR forms i.e. ITR 2, ITR 3, ITR 5, ITR 6 and ITR 7 contain relevant changes for reporting the income arising from the transfer of such carbon credits and tax thereon.

ITR 6

In addition to the above-mentioned modifications, the following changes in reporting have been incorporated in ITR 6 for AY 2018-19:

1. Ind AS compliant companies are required to present their balance sheet and profit and loss account in the format as prescribed by Division II of Schedule III to the Companies Act, 2013.

2. The new provisions inserted with respect to Section 115JB i.e. MAT require Ind AS compliant companies to make additional adjustments to the book profit for all items credited/debited to ‘other comprehensive income‘ and all items specified therein. Consequent changes have been made to ITR 6 to facilitate the reporting of the calculation of ‘Book Profit' in accordance with the provision.

3. Every company not subject to Tax Audit under Section 44AB is required to provide the following details pertaining to transactions entered into with registered/unregistered suppliers under GST in a new schedule that has been incorporated in ITR 6:

- Transactions in exempt goods or services;

- Transactions with composite suppliers;

- Transactions with registered entities and total sum paid to them;

- Transaction with unregistered entities.

One will need to be very careful while filling up these fields since all the GST related data is already available with the government and it would be very easy for them to match the two sets of data through a software.

4. A new field has been inserted in ITR 6 to provide details of amounts apportioned by companies from the net profit towards their corporate social responsibility.

5. A new column has been incorporated in ITR 6 whereby an unlisted company is required to furnish particulars of natural persons who were the ultimate beneficial owners, whether directly or indirectly of shares holding not less than 10 percent of the voting power at any time during the previous year. The following particulars are to be furnished:

- Name and address,

- Percentage of shares held,

- PAN (if allotted).

6. Companies not subject to tax audit under Section 44AB are required to provide details of payments made and sum received in foreign currency towards its capital and revenue account.

ITR 7

In addition to the above-mentioned modifications, the following changes in reporting have been incorporated in ITR 7 for AY 2018-19:

1. Changes have been incorporated in ITR 7 wherein a trust is required to furnish certain details if there has been a modification to the stated objects and if such objects do not conform to the conditions of registration. The details to be furnished are as follows:

- Date of change in objects;

- Whether the application for fresh registration has been made within a stipulated time period;

- Whether fresh registration has been granted;

- If yes, date of such registration.

2. Dividends received exceeding Rs 10 lakh taxable under Section 115BBDA are to be disclosed in Schedule OS i.e. schedule for income from other sources and Schedule SI i.e. schedule for income subject to tax at special rates.

3. The following additional information is to be presented in ITR 7 by a charitable or religious trust:

- Date of registration or approval granted to the trust;

- Amount utilized during the year for the stated objects out of surplus sum accumulated during the earlier year;

- The table seeking details about the name and annual receipts of institutes under Section 10(23C)(iiiab), (iiiac), (iiiad) and (iiiae) has been removed from the ITR. However, a trust is required to provide details of its aggregate annual receipts of the institutions run by it.

4. ITR 7 requires the political parties to make a declaration by selecting ‘Yes' or ‘No' in the check-box provided in Schedule LA for political parties in the ITR in response to the question whether it has received any cash donation in excess of Rs 2,000.Further ITR 7 also seeks following information regarding the auditor under Schedule LA for political parties:

- Name of the auditor signing the audit report;

- Membership number of the auditor;

- Name of the auditor;

- Proprietorship/firm registration number;

- PAN of the auditor.

Conclusion

Based on our experience, we strongly believe that taxpayers would be taking a big risk by not taking professional help in filling up the ITR forms. The forms, the schema, the interconnection between various fields of the same form as well as matching of data in the ITR with data from other sources are all extremely intricate and complicated and a small mistake could result in protracted litigation and consequential headaches for the taxpayer. Even riskier would be to use the services of websites and outsourcing agencies who claim to help taxpayers in filing their returns within a few minutes and that too “with a smile” – all for a pittance. Filing of returns is not a petty task and must be accorded utmost importance and urgency by a taxpayer.

Ameet Patel is Partner and Ayesha Aziz is Tax Executive at Manohar Chowdhry & Associates, Chartered Accountants

The views expressed here are those of the author's and do not necessarily represent the views of BloombergQuint or its editorial team.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.