India's Monetary Policy Committee kicks off the first meeting of the new financial year this week with a debate on whether it is time to hike interest rates for the first time in over four years.

The specter of rate hikes emerged at the last meeting of the committee, with one of the six members voting for a 25 basis point hike in the repo rate. Those supporting a rate hike say that the risk of inflation rising and slipping away from the mid-point of the MPC's mandate of 4 percent (+/- 2 percent) has increased. Those opposing a rate hike say inflation concerns are overdone and that there is a structural decline in inflation in India.

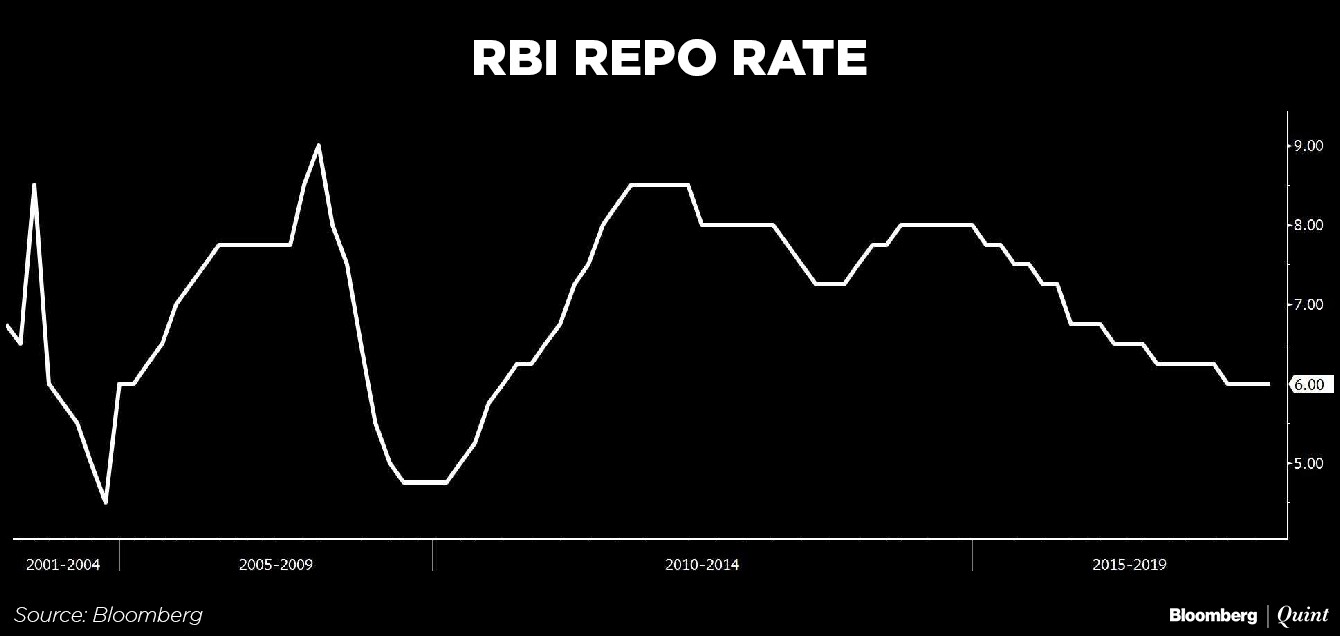

The debate presents an opportune moment to recall India's volatile inflation past and question whether the future is more sanguine.

At last read, consumer price inflation in India stood at 4.4 percent. That was for the month of February. At these levels, retail inflation has now remained within the MPC's tolerance band of 4 percent (+/- 2 percent) for 19 consecutive months.

For next year, the prognosis is for higher, but still moderate, inflation. In February, the RBI said that it expects CPI inflation in the range of 5.1-5.6 percent in the first half of 2018-19 and 4.5-4.6 percent in the second half. Inflation risks have risen both from global factors like higher oil prices and domestic factors like fiscal slippage, said the RBI.

It is true that price pressures may build up next financial year. Still, inflation is well below levels seen as recently as 2013, when CPI inflation had hit a high of 11 percent.

Also Read: How Much Longer In The Goldilocks Zone?

The key question is whether this run of low inflation can continue? And if it has been driven mostly by fortuitous factors like a period of low global oil prices and a change in minimum support price policies. Or if there has been a structural change in the inflation scenario in India.

The two divergent views on this issue come from two ends of the MPC. Michael Patra —the most hawkish member on the committee—argued in the last MPC meeting that a ‘series of rate hikes' may be warranted. On the flip side, Ravindra Dholakia—the most dovish member on the committee—in a co-authored paper in the Economic and Political Weekly argued in March that inflation dynamics in India have turned for the better.

The Case For A Softer Stance

The paper by Dholakia and co-author Virinchi Kadiyala tests the two basic findings of the 2014 monetary policy framework report. The study, which was the basis for India's flexible inflation targeting regime, had highlighted that high food and fuel prices feed into generalised inflation via inflationary expectations. The high inflationary expectations mean that core inflation (ex-food and fuel) becomes sticky and has a persistent impact on headline inflation.

As such, even though monetary policy may not directly impact food and fuel-led inflation, it can prevent generalisation of inflationary pressures by curbing second round effects, the report had argued.

Dholakia and Kadiyala argue that those dynamics do not necessarily hold true in the current scenario. According to the duo, the change in the institutional setting for inflation management (vis-à-vis the inflation targeting framework) has led to a moderation of inflation expectations and, hence, a decline in ‘inflation persistence.' This, according to the article, is consistent with international experience. The paper goes on to test whether core inflation moves towards headline inflation or vice-a-versa in the current scenario. It concludes that it is headline inflation which tends to revert to core inflation post a shock, which may have been brought on by volatile food and energy prices.

Essentially the authors argue that there has been a change in the inflation dynamics in India and the MPC must account for them before deciding on the future course of policy.

Also Read: Inflation Relief, IIP Boost May Not Be Enough For Monetary Policy Panel

Avoiding Mistakes Of The Past

Patra, a career central banker, appears to see the inflation scenario differently. In a speech in October, Patra had explained the RBI's much-criticized decision to change the monetary policy stance from ‘accomodative' to ‘neutral' in August 2017. Patra explained the move against the backdrop of concerns that an increase in House Rent Allowance would have not just a statistical first round impact but also possibly a generalised second round impact.

At subsequent MPCs, Patra has argued that upside risks to inflation are materialising and starting to get generalised. With an eye on the 4 percent mid-point of the MPC's inflation target, Patra noted at the December 2017 meeting that inflation is likely to stay above that point, particularly as growth strengthens. At the February meet, he noted that inflation expectations are elevated and volatile, and various measures of underlying inflation are moving closer to the headline inflation rate above 5 percent. He cautioned that as the negative output gap closes, inflation could move above the tolerance band of 6 percent.

In short, Patra seems to believe that traditional drivers of inflation in India persist and the MPC would do well to preempt a sudden pick-up in price pressures as the economy stabilises.

While Patra was the only one who voted for a rate hike, other member of the committee also called for greater caution on the inflation front. RBI governor Urjit Patel and deputy governor Viral Acharya both acknowledged that inflation risks have risen but said they prefer to wait for more data before changing the stance away from neutral or voting for a rate hike

What Will The Next Rate Cycle Look Like?

While most economists believe that rates will remain on hold in the near term, settling the inflation debate is important to understand what the next interest rate cycle will look like.

If indeed underlying inflation drivers have changed, could we see flat interest rates for a extended period of time into at least next year? If they haven't, will an inflation targeting monetary policy committee need to raise rates in quick succession to ensure that peak inflation and peak interest rates remain below those seen in previous cycles?

Questions for the MPC to ponder as it begins a new financial year of policies.

Ira Dugal is Editor - Banking, Finance & Economy at BloombergQuint.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.