The arrival of the Omicron variant has imparted significant uncertainty with respect to the Covid-19 endgame, the economic outlook, and the monetary policy exit strategy. To answer these questions, it is beneficial to take a step back and assess where the economy stood before the virus threat emerged, how Omicron might influence the economic outlook, and the appropriate policy response.

How Strong Is the Growth Recovery?

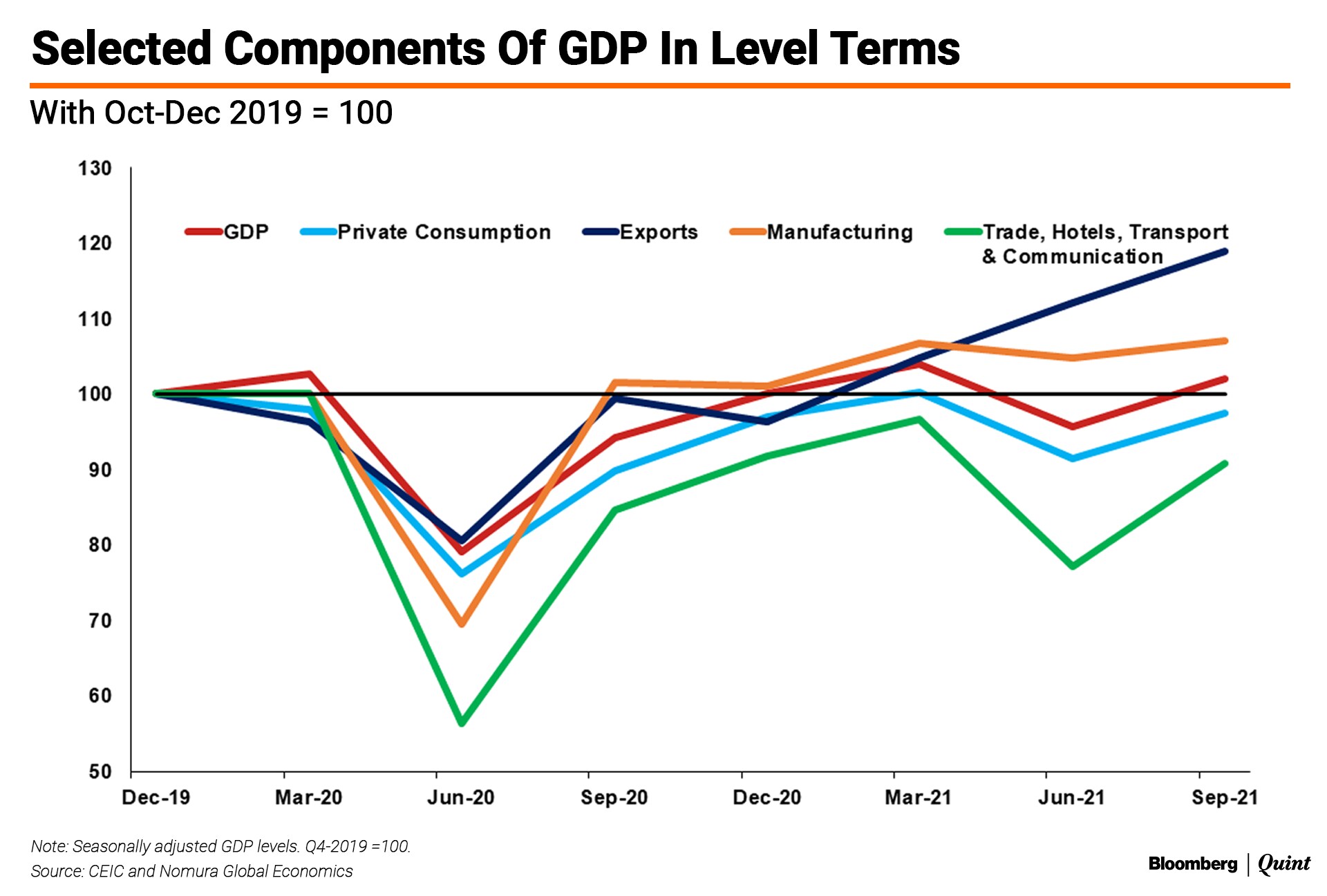

GDP data for Q2FY22 (July-September) show the economy bounced back swiftly from the second wave trough. In level terms, GDP is now around 2% above pre-pandemic levels (October-December 2019).

However, this masks the unevenness below the surface. While the manufacturing sector is nearly 7% above pre-pandemic levels and exports are 19% above, private consumption is still 3% below, and the trade, transport, hotels, and communications sector lags 9% behind.

For a durable growth uplift, the investment cycle has to pick up. Yet, despite the push on public capex and reforms, private investment remains lacklustre, mainly due to weak demand.

Hence, while the economy has bounced back from the second wave lows, the uptick appears cyclical for now, while scarring effects suggest post-pandemic potential growth has fallen.

Is Inflation A Real Worry?

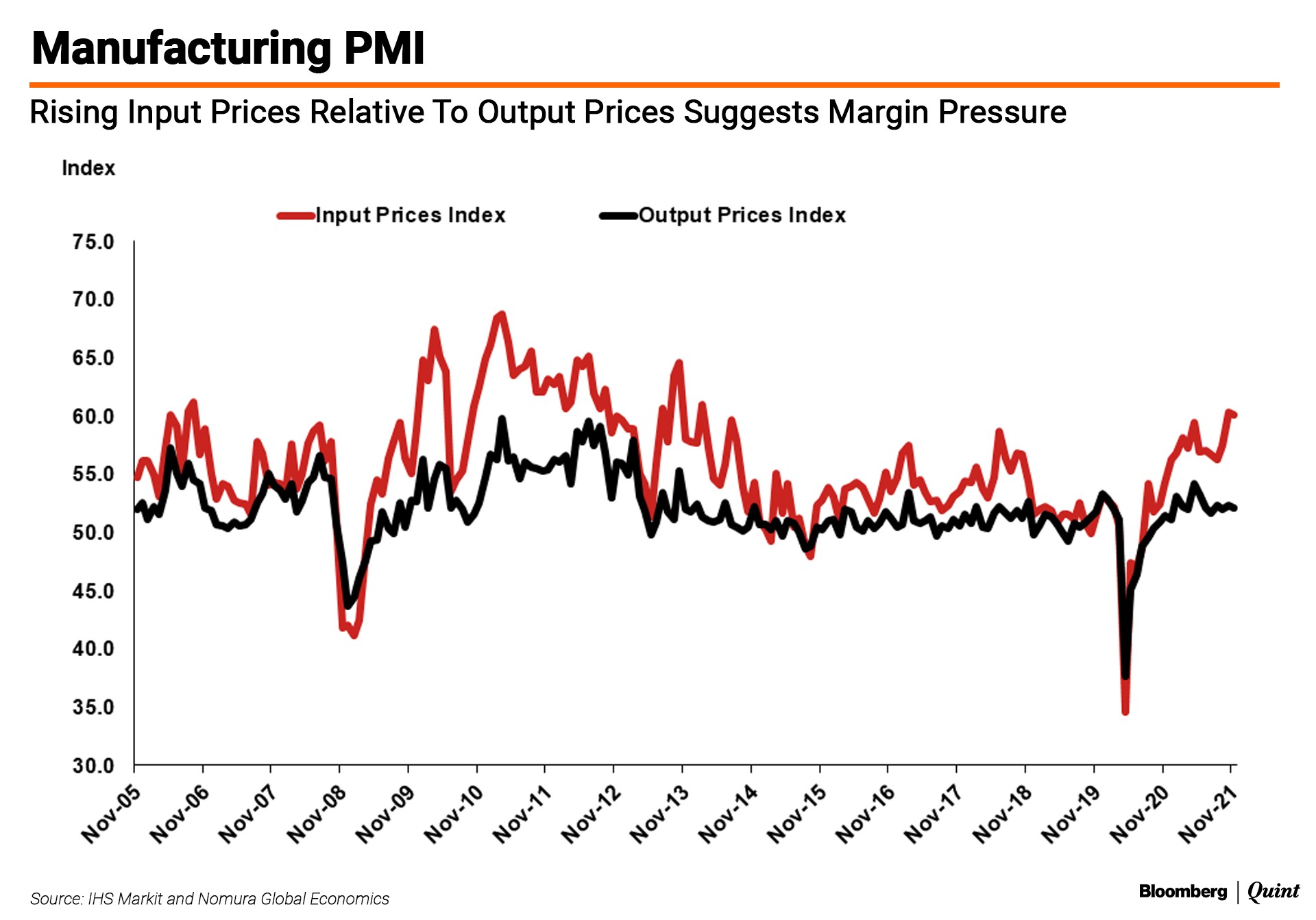

Even as growth remains shaky, inflation risks appear skewed to the upside. The build-up of commodity cost pressures over the last year has not been passed completely to consumers due to weak demand. But with firm margins under pressure, some pass-through is inevitable.

There are other price pressures. Higher gas prices globally have led to skyrocketing fertiliser costs. Higher coal and gas prices are raising the cost of producing electricity. Telecom firms have raised tariffs to strengthen their balance sheets.

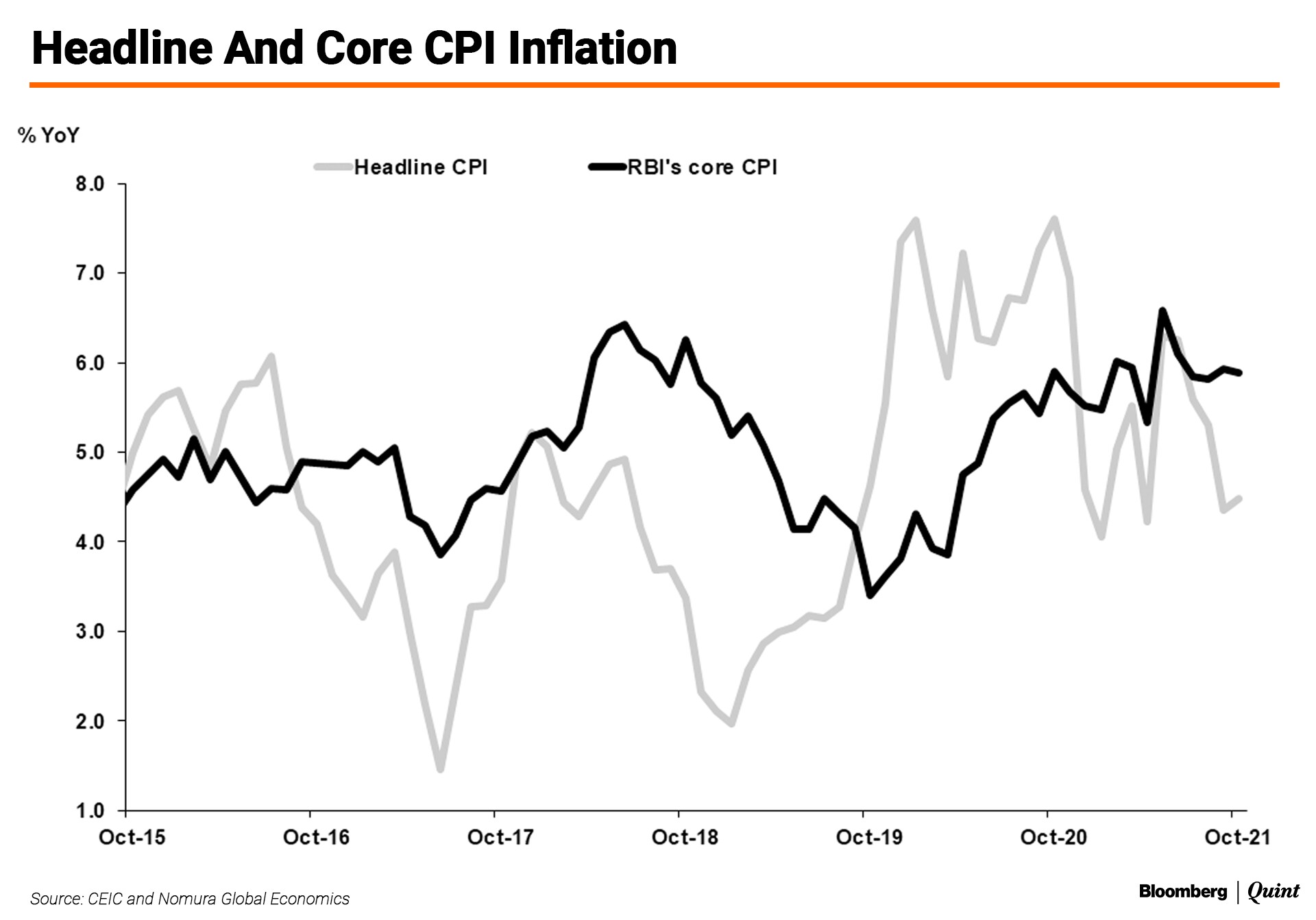

Policymakers have also become more tolerant of inflation. After two years of 5-6% inflation, the inflation glide path aims for a gentle landing towards the 4% midpoint target only by FY24. Inflation expectations have nudged higher to a level that is now consistent with CPI inflation at 5.0%.

As a result, while the output gap is still negative and should lead to lower inflation, other factors are stacked in the opposite direction.

How Will Omicron Impact The Economic Outlook?

Past experience suggests virus waves lead to higher inflation and lower growth.

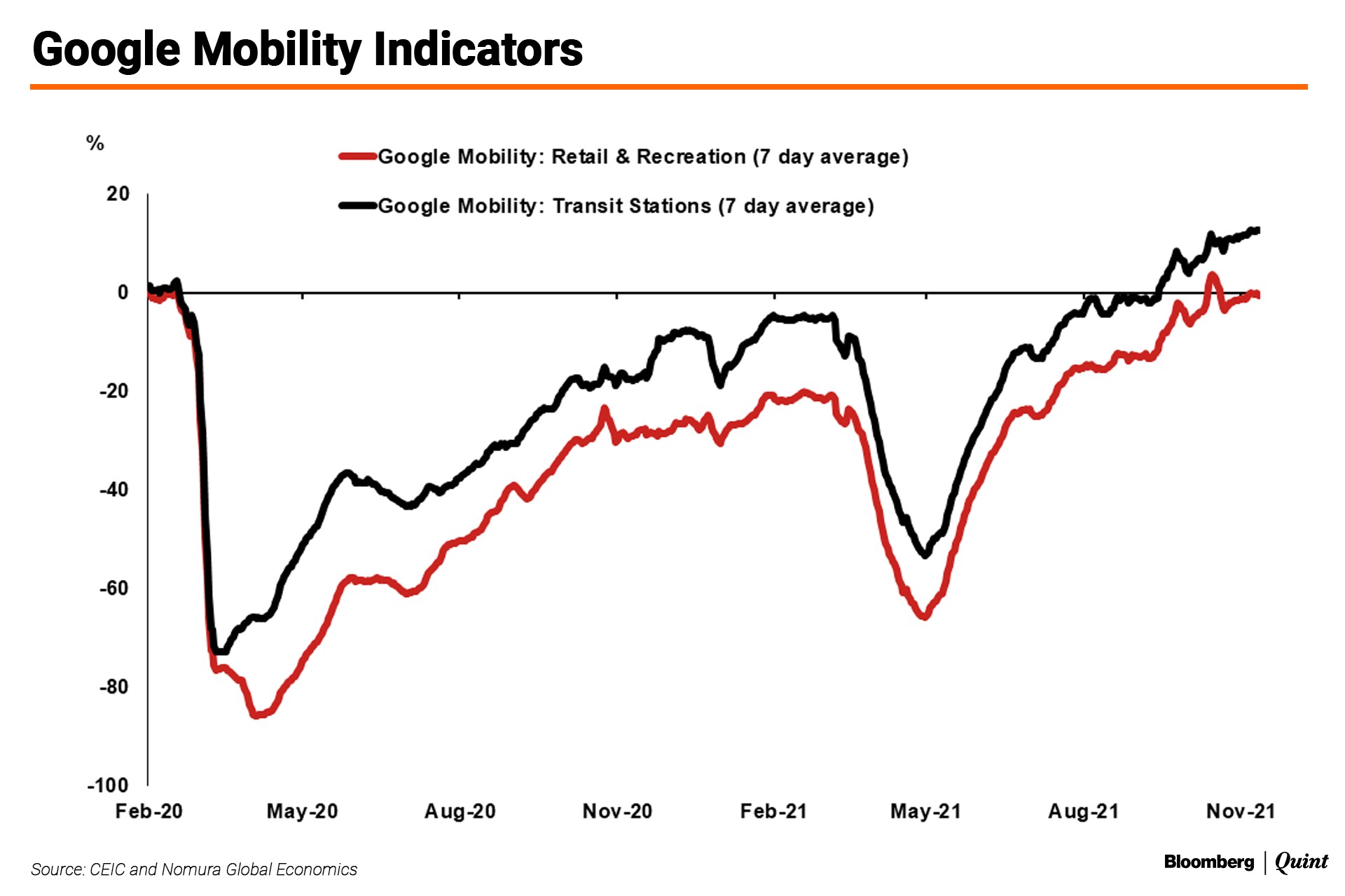

The negative growth impact of each wave has waned over time, as consumers and businesses are adapting. Nevertheless, there could be an adverse impact on services such as travel & hospitality, retail & recreation, either due to tighter government restrictions or voluntary caution by individuals due to the fear factor. For instance, travel booking cancellations rose after the Omicron news. Therefore, the uptick in mobility seen since the May 2021 lows may start to taper. On the other hand, the impact on manufacturing should be minimal, unless India experiences a third wave.

In contrast, each wave has left price levels higher. Even though lower oil prices are a big relief for India, if it sustains, pandemic waves could lead to higher inflation. Labour market frictions could rise, as virus concerns reduce the willingness to work in person. Insufficient numbers of plantation workers in Malaysia or factory workers in Vietnam have become a common occurrence.

Global supply chain disruptions could continue, adding to cost pressures. Supply constraints can also lead to a greater mark-up between retail and wholesale prices, as witnessed in India during the first and second waves.

What Course Of Action Should Policymakers Take?

While the continued disruptions due to the pandemic strengthen the case for extending the targeted fiscal and financial support for hard-hit sectors, economic restructuring and the reskilling of workers will eventually be needed to adapt to the new normal. If high uncertainty weighs on private demand, then a bigger push on public capex will be needed.

For monetary policy, the uncertainty around Omicron may lead policymakers to wait and watch, but we would argue that monetary policy should keep calm and carry on (with their business), for three reasons.

First, uncertainty may prevail even in the future. One thing we have learnt over the last two years is that the virus will keep mutating and there could be newer variants. Vaccinations may need to be followed by booster shots. Countries are learning to live with the virus and the uncertainty.

Second, policies need to take into account the risk/reward from continuing with the current approach. Easy policies do help growth, but they don't help contact intensive services as much, and could even hurt growth, if they lead to sustained higher inflation. There is also the risk of asset price bubbles or the mispricing of risk.

Third, as discussed earlier, past waves suggest the economic impact of Omicron may fall less on growth and more on inflation, even with lower oil prices. 2022 will likely mark the third year of above 5% inflation, on our forecasts.

Hence, sticking with gradual normalisation, so that medium-term risks do not fructify, is par for the course.

For now, this means continuing with liquidity normalisation and narrowing the corridor, both of which will still leave accommodative conditions behind.

Just as consumers and businesses are learning to live with the virus, so should policymakers. Otherwise, they will end up waiting for Godot.

Sonal Varma is the Chief Economist for India and Asia ex-Japan at Nomura.

The views expressed here are those of the author and do not necessarily represent the views of BloombergQuint or its editorial team.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.