India's economic recovery may appear increasingly paradoxical. Surging equity markets amidst an incomplete recovery. Sluggish domestic investment but strong and sustained FDI. Unprecedented liquidity but soft credit growth. Tight IT labour markets amidst a lot of rural slack. Ostensibly large output gaps but sticky core inflation. What explains these disconnects? This piece lays out the various paradoxes, analyses their underpinnings and discusses associated policy implications.

Five Paradoxes

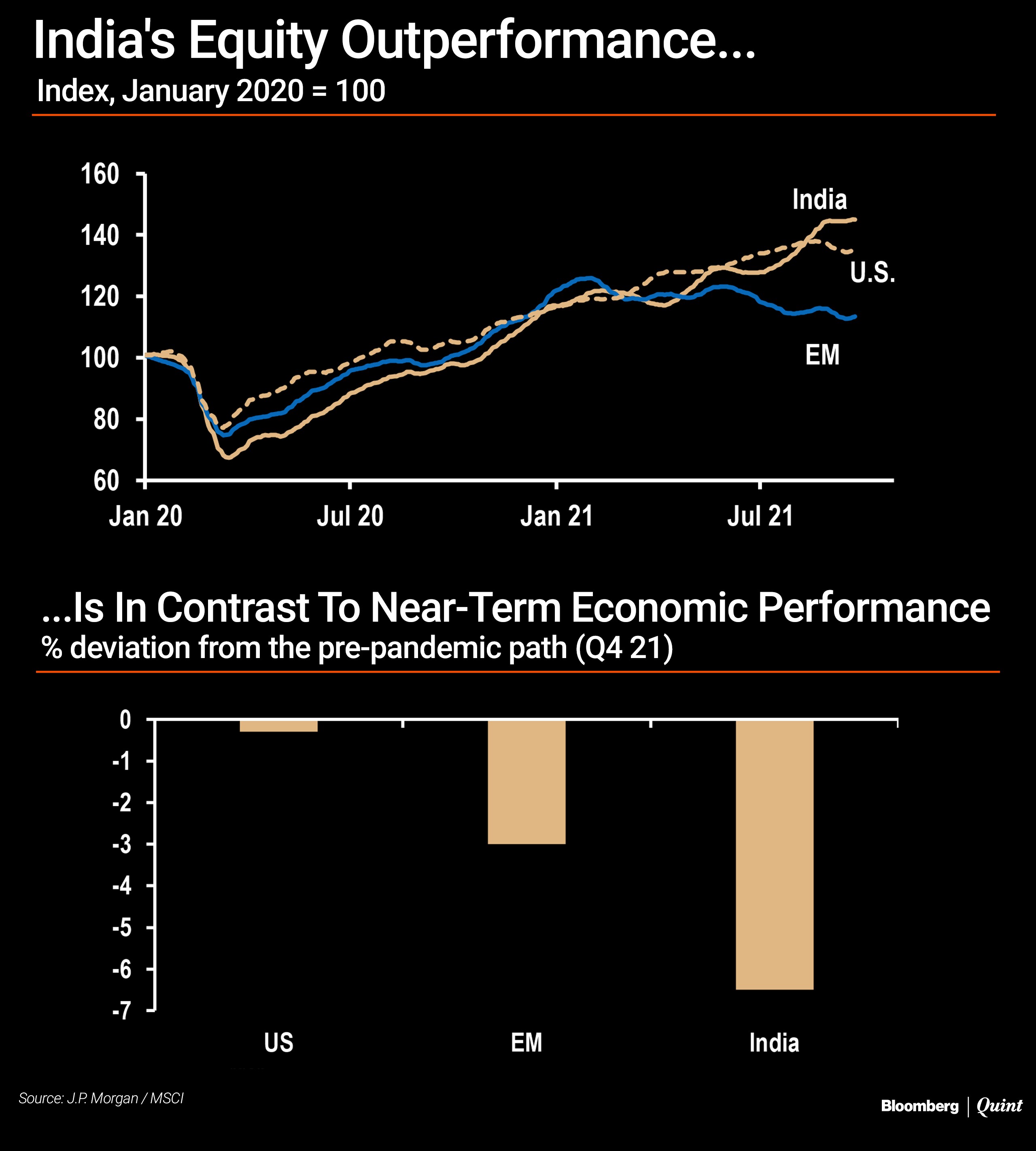

Paradox 1: Markets Versus The Economy

India's equity market has been among the best performing in the world this year, significantly outperforming emerging markets and moving lock-step with U.S. markets.

Yet, this relative market performance, prima facie, is at odds with relative economic performance.

Even as India's economy continues to recover, activity is still expected to be about 6% below its pre-pandemic path at the end of this year. In contrast, the United States will be virtually back on its pre-pandemic path and emerging markets will be about 3% below. As a consequence, India's equity market is among the most expensive in the world, with forward P/E multiples at an unprecedented 24x, more than two standard deviations away from the norm.

What explains this disconnect between markets and the economy?

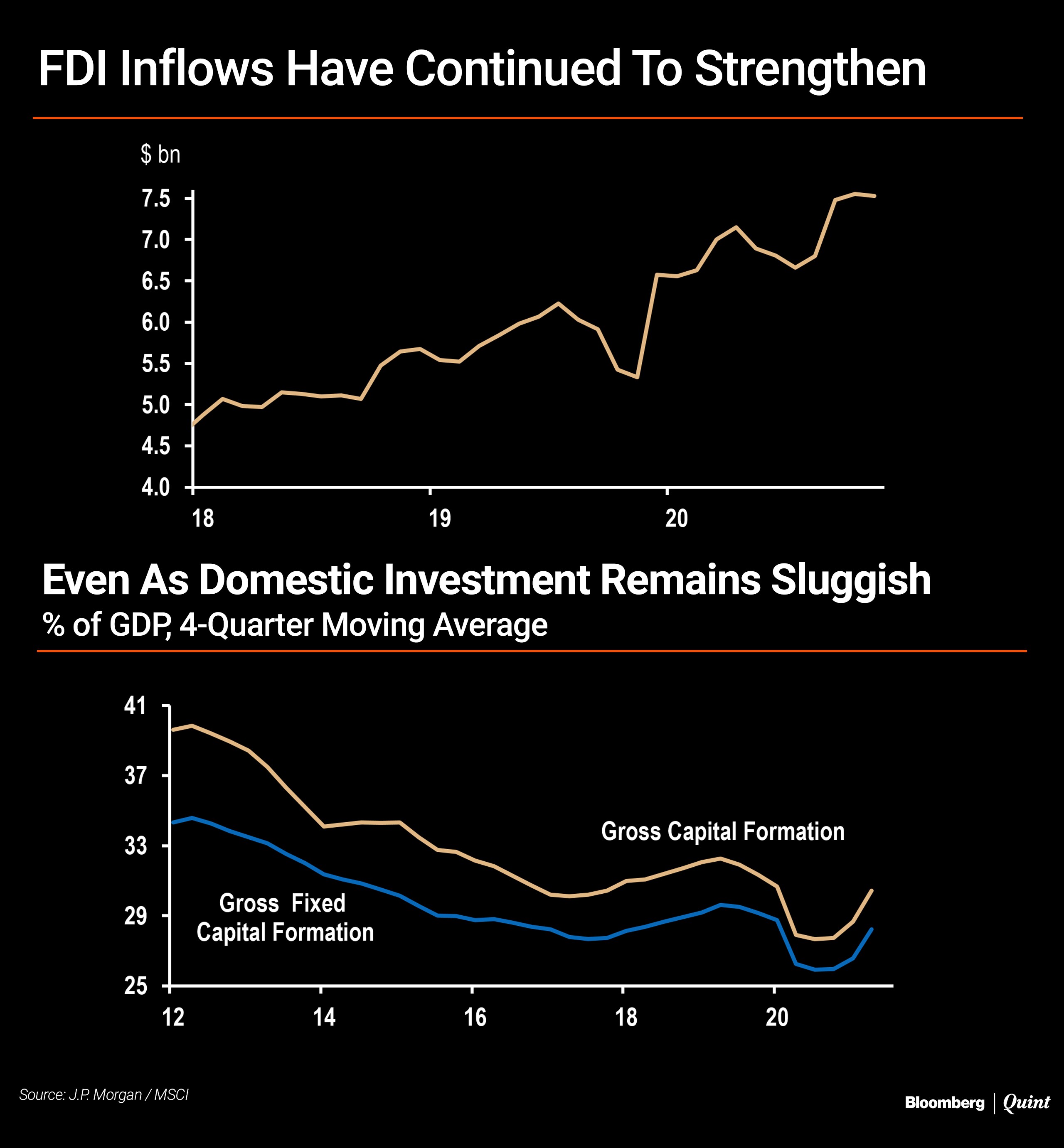

Paradox 2: FDI Versus Domestic Investment

Foreign direct investment inflows into India have increased strongly and secularly in recent years, getting another bump-up during the pandemic.

Normally, FDI should be positively correlated with the domestic investment cycle. But domestic investment has been slowing for a while.

Investment/GDP was at 39% in 2011, but has since slowed to 31% of GDP in 2020. To be sure, large corporates have deleveraged meaningfully and their balance sheets are generally in much better shape. Yet, aggregate manufacturing capacity utilisation has been running only in the 60s, suggesting any broad-based investment pick-up will take time.

Why the disconnect between domestic investment and FDI?

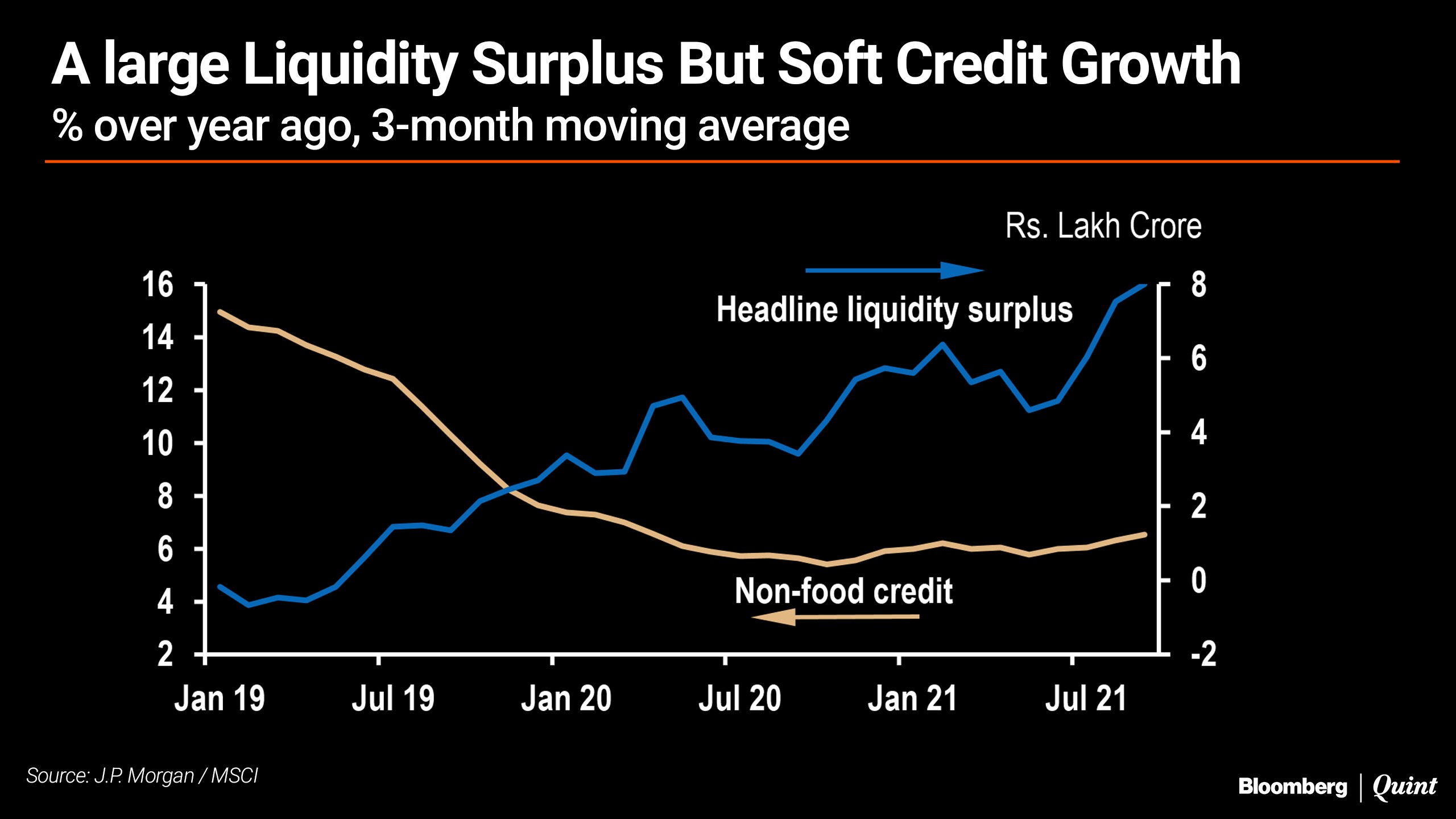

Paradox 3: Liquidity Versus Credit Growth

The banking system is awash in an unprecedented quantum of liquidity, with the core surplus touching Rs 12 lakh crore (around 5% of GDP) and banks typically parking Rs 7 lakh crore with the RBI.

Despite that, credit growth remains very muted, still averaging about 6-7% in nominal terms, and therefore barely growing in real terms.

Why the disconnect between liquidity and credit growth?

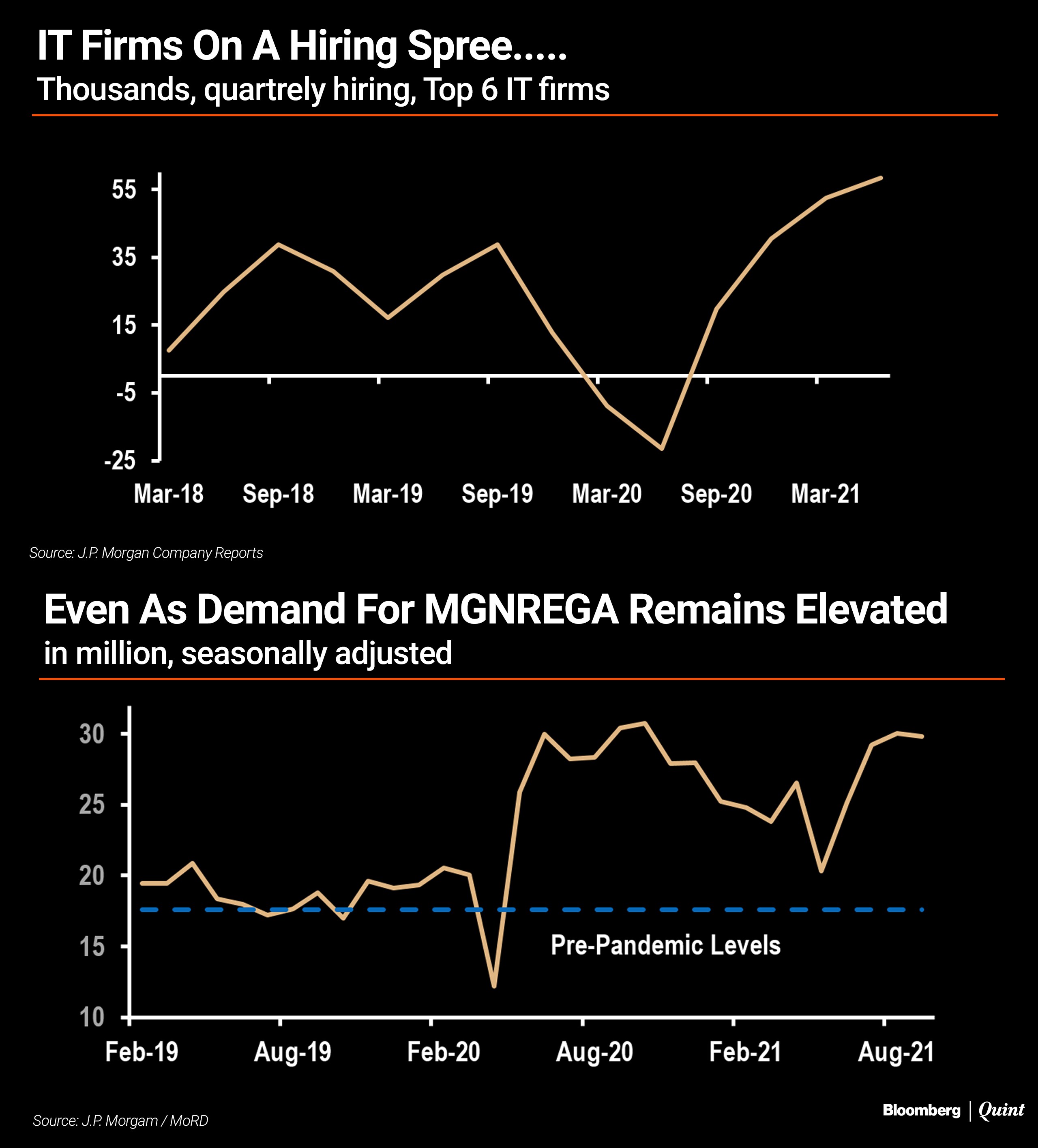

Paradox 4: Tech Versus The Rest

Informal and rural labour markets remain under visible pressure.

Employment in agriculture has increased from 36% to 39% of the labour force, demand for MGNREGA even in September was 60% higher than normal, and rural wages are rising at 5-6% in nominal terms, and therefore flat in real terms.

Yet this contrasts sharply with a very tight labour market for information technology services, for example, characterised by high attrition rates, strong hiring and upward pressure on wages.

Why, such a big contrast across labour markets?

Paradox 5: Growth Versus Inflation

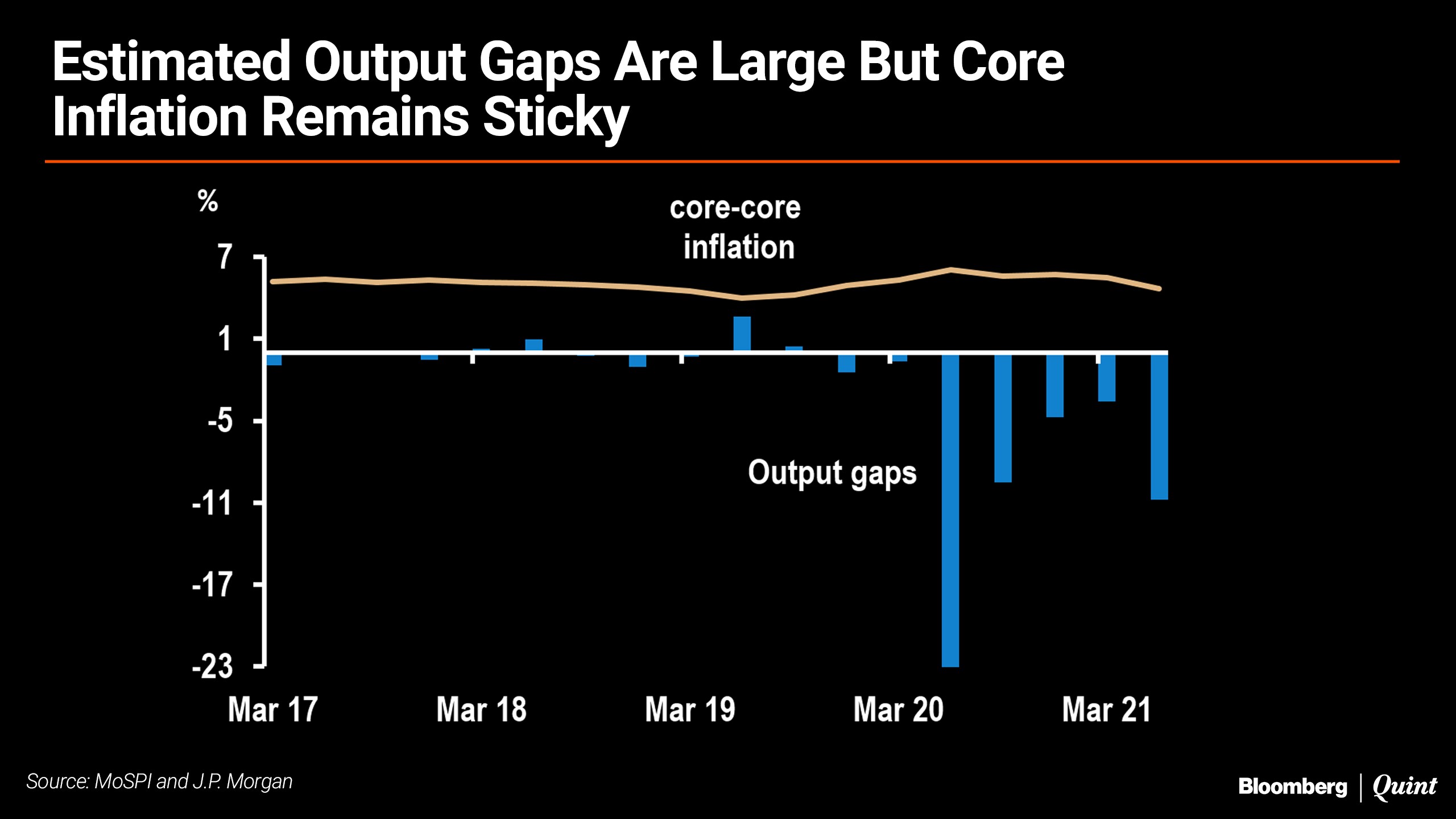

With the economy remaining consistently below the pre-pandemic path, significant slack is assumed to exist on the supply side.

Indeed, mechanical calculations of ‘output gaps' reveal large gaps for the last six quarters. Why then has core inflation been so sticky?

In contrast to many emerging markets, India's core inflation actually accelerated during the pandemic, and has remained at 5% for 18 months. If there is so much slack, why has core inflation been so sticky?

Four Characteristics Of The Recovery

How does one rationalise these paradoxes?

In our view, they reflect the interplay of four characteristics of India's recovery:

Labour market scarring spilling into consumption;

Divergences across factors of production and firm size;

A steroidal-burst towards digital adoption during the pandemic;

Very accommodative monetary policy intersecting with a financial system that is still risk averse in parts.

Labour Market Scarring And The Spillover To Consumption

Both a symptom and a cause of India's incomplete recovery is scarring in the labour market.

At an aggregate level, the employment/population ratio has consistently remained 2 percentage points below pre-pandemic levels. Consequently, the “effective unemployment rate” (combining changes in both labour force participation and unemployment) remains above 12% in October 2021 vis-à-vis 7.5% pre-Covid.

Sustained income pressures are bound to impact consumption, as reflected in the RBI's consumer confidence surveys, where current employment perceptions — while slowly improving — still remain depressed. In effect, the pandemic has insidiously generated a transfer of income from the bottom to the top of the income pyramid (as a share of GDP), where the marginal propensity to consume is lower and that to import is higher. This is demand impeding in the steady state.

Contrary to popular perception, therefore, consumption has been the slowest driver of demand to recover.

The consumption of goods remain about 15% below the path it was on at the end of 2018, before the consumption slowdown in 2019 and the pandemic. To be sure, the stress is concentrated at the lower end, with two-wheeler sales down almost 30% in 2021 vis-à-vis 2019 levels, and gross NPAs skewed towards financial institutions catering to the bottom of the pyramid.

These dynamics help explain why manufacturing utilisation and credit growth rates have not picked up more sharply, despite very accommodative monetary conditions. Essentially, the income shock to households is swamping the price effect from lower interest rates, for now.

A Divergent Recovery

The pandemic has inflicted Darwinian-like outcomes on firms.

Profits have prevailed over wages, large firms over small firms and the formal sector over the informal sector.

Over the last four quarters, listed company profits have surged 48% while the wage and salary bill has grown 6% (to be sure, future profits are likely to be squeezed by higher crude and commodity prices).

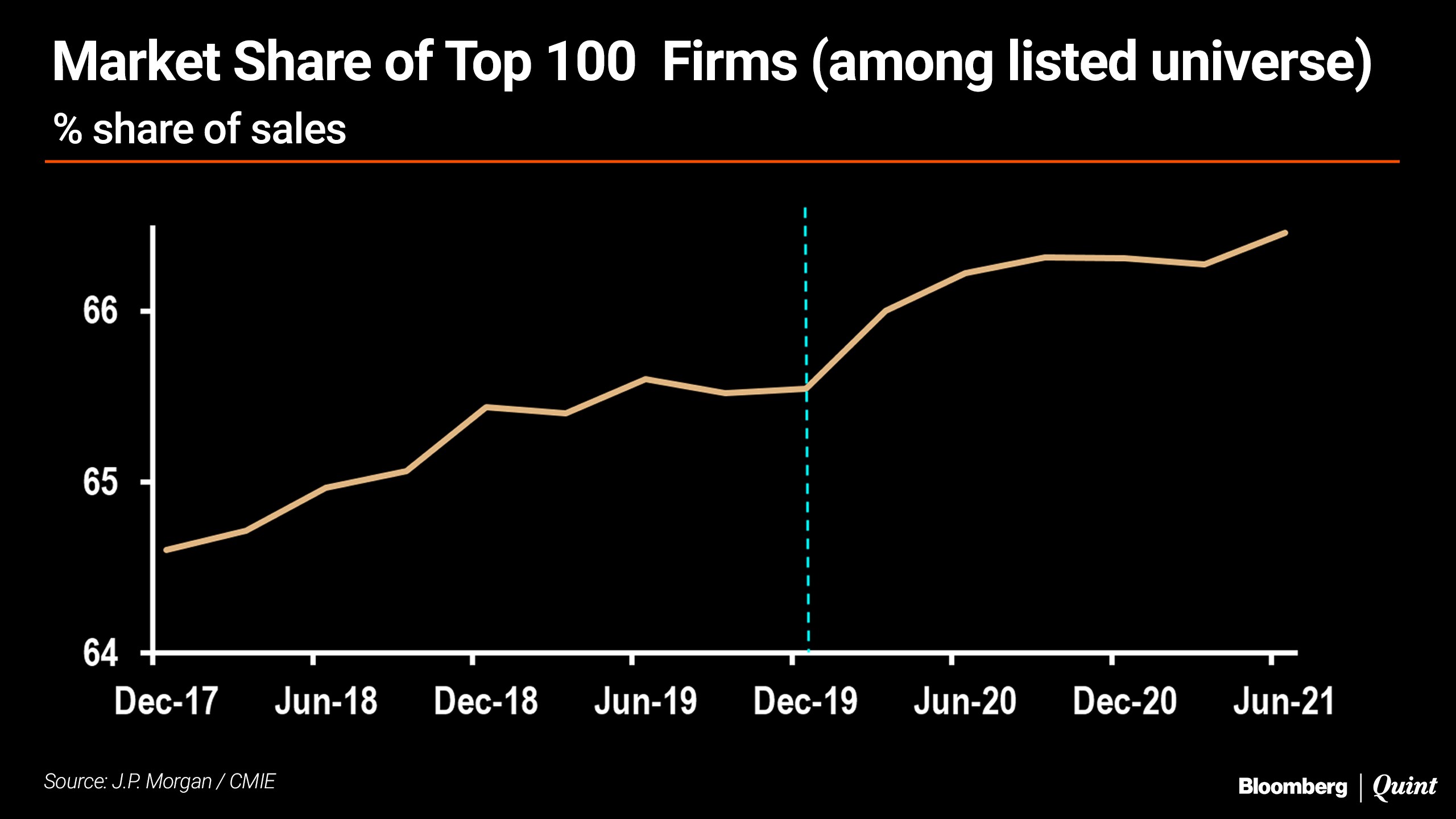

Even within the listed universe, size and scale has mattered. In the April-June quarter, sales of the top 100 firms grew 3% (vis-à-vis the same quarter 2019) but that of the bottom 500 firms contracted 18%.

Consequently, market share of the top 100 firms—already increasing pre-Covid—has increased further (see chart below).

That said, relative outperformance is likely to be greater between the formal and informal sectors, rather than within the formal sector.

These divergences help explain several paradoxes but also raise key questions.

A profit-led recovery and growing market share of the largest firms likely explains stock market excitement even as the broader economy makes a more gradual recovery.

But is the growing market share of the large firms contributing to higher pricing power? Also, is the hit to the informal economy, and therefore the supply side, more than anticipated resulting in smaller output gaps? Are these forces keeping core inflation sticky?

These industrial-organisational changes are likely to have a key bearing on future growth-inflation dynamics.

Tech And The Pandemic

Covid has delivered a steroidal thrust to technological adoption, with the implication that heretofore-unthought-of-services are likely to be offshored out of advanced economies.

India's IT sector is likely to be a large beneficiary of this dynamic. Increased IT adoption (advanced economies, domestic financial institutions, start-ups) have combined to generate a large demand for skilled IT workers, resulting in elevated attrition, strong hiring and sharp pressure on wages. Tech is also increasingly responsible for FDI inflows.

The ‘tech boom' therefore helps explain the strength of FDI and also why certain labour markets are tight. To be sure, strong IT sector growth will be unambiguously positive for growth. But industry estimates reveal total employment in the IT sector is just about 1% of India's labour market, so dynamics in the IT sector are not necessarily a microcosm for the broader economy.

Monetary Policy And The Financial Sector

Finally, like in many parts of the world, monetary policy remains very accommodative in India, though we worry about the stickiness of India's inflation.

Real policy rates remain meaningfully negative and the system is flush with liquidity. Yet, these dynamics have to contend with a financial sector that still remains, in part, relatively risk-averse to lend. Public sector bank risk aversion pre-dates the pandemic. And economic scars to the bottom of the pyramid, could inject caution to the system's periphery that was instrumental in driving growth pre-pandemic. Along with demand factors, therefore, residual financial sector risk aversion is likely contributing to muted credit growth.

Instead, very accommodative monetary conditions are likely contributing to buoyant asset prices, as a system flush with liquidity searches for returns.

All told, it's the interplay of these four characteristics that's generating the paradoxes:

Incomes and consumption will take time to recover and some parts of the financial system still remain relatively risk averse, explaining lower capacity utilisation, tepid credit growth and an incomplete recovery.

Yet, profits have surged and liquidity is plenty—both globally and domestically—underpinning frenzied asset prices.

The tech sector, in particular, is booming thereby attracting FDI and creating some employment.

But the informal economy lags, the demand effects of which are showing up in MGNREGA, and the supply effects of which may be keeping core inflation sticky.

Three Policy Implications

Against this backdrop, at least three policy implications come to mind:

The Fiscal-Monetary Balance

Given a yet-incomplete recovery and labour market scarring on the one hand, and sticky inflation on the other, overlayed with a negative terms of trade shock from higher crude and commodity prices (which will simultaneously impact growth and inflation) it will be important to maintain the appropriate fiscal-monetary balance in the near term.

Given the ability of fiscal policy to intervene in a more targeted manner, the fiscal should not overtighten in the near term.

For starters, the center and states must fervently attempt to execute the strong capex growth (30%+) that has been budgeted. Second, given the pandemic-induced formalization of the economy, gross taxes are running higher than budgeted. If revenues exceed budgeted targets, they should be used to increase expenditures, rather than over-deliver on the fiscal deficit this year. Central government expenditures (ex interest and subsidies), as a share of GDP, are budgeted to decline in FY22, and any revenue windfall should aim to augment this ratio.

At the same time, monetary policy is already very accommodative. Inflation risks apart, a steep yield curve creates maturity-transformation risks, while a large quantum of liquidity has ensured the spread between AAA and AA corporate bonds has virtually closed creating mis-allocation risks. Gradual but progressive normalisation of monetary policy will therefore be important to pre-empt any financial stability concerns.

Just as the fiscal impulse this year should seek to avoid being too tight, monetary policy should seek to avoid being too accommodative.

Meanwhile, continuing efforts to hasten stressed-asset resolution and reduce risk aversion in the financial system will be key to the broader transmission of easier monetary conditions but also to the facilitating of some creative-destruction that Covid is inevitably spawning.

Fiscal Consolidation With Capex Enhancement

With consumption and investment likely to recover more gradually, government capex will have to lead growth in the near term, a strategy the government has clearly adopted in recent quarters. Physical infrastructure apart, much-needed investments on health and education are also due.

But how will the government increase total physical and social infrastructure spend in the coming years, even as the consolidated deficit has to reduce from around 13.5% of GDP in FY21 to 7.5% of GDP in FY26? The only way to square the circle is to augment the revenue side: asset sales and monetization in the near term (of which an encouraging start has been made this year) followed by rationalising the tax base (both direct and indirect) and GST rate structure in the coming years.

Service Exports As An Engine of Growth

No emerging market has grown at 7-8% for years on end without partaking in strong export growth. India's own buoyant growth experience in the first decade of this millennium was underpinned on the Siamese twins of exports and investment.

But even as the extant focus has been on manufacturing exports — where India's global market share remains low and stagnant — India's global market share of services has continued to rise, revealing a growing comparative advantage. With the pandemic likely to provide a renewed thrust to off-shoring of services, India must stand ready to grab the opportunity, from both a regulatory and supply perspective.

Service exports are likely to be an important near term driver of growth. That said, creating an eco-system to improve competitiveness and boost exports more broadly will be vital to India's growth prospects over the next decade.

The pandemic has thrown-up unprecedented challenges and divergences but also delivered enticing growth opportunities. Emerging market policymakers have the unenviable task of having to simultaneously mitigate and dampen the former while harnessing the latter.

Sajjid Z Chinoy is Chief India Economist at JPMorgan. All views are personal.

The views expressed here are those of the author, and do not necessarily represent the views of BloombergQuint or its editorial team.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.