A key recommendation of the Bimal Jalan committee that reviewed the Reserve Bank of India's economic capital framework was a reiteration that the central bank should not distribute surpluses from its very considerable revaluation reserves.

Separately though, the RBI has now adopted a significantly different method of accounting for its currency and gold sales, that extracts realised income from its revaluation reserves.

While details around this major accounting change are sketchy, we consider how this accounting methodology likely worked in FY19, and its implications for future.

Under the new policy, it may now be possible for RBI to theoretically extract over Rs 2 trillion of income from its revaluation reserves in FY20, under the right circumstances.

Ultimately, the debate should likely be less about whether this accounting change is appropriate or not, and more about how much the RBI can and should monetise the government via its market operations and surplus transfers.

Understanding RBI's New Currency, Gold Revaluation Methodology

In a previous article, we had described the somewhat anomalous nature of currency accounting hitherto followed by the RBI. Here is a quick recap, and a brief description of what has since changed in RBI's currency accounting policy.

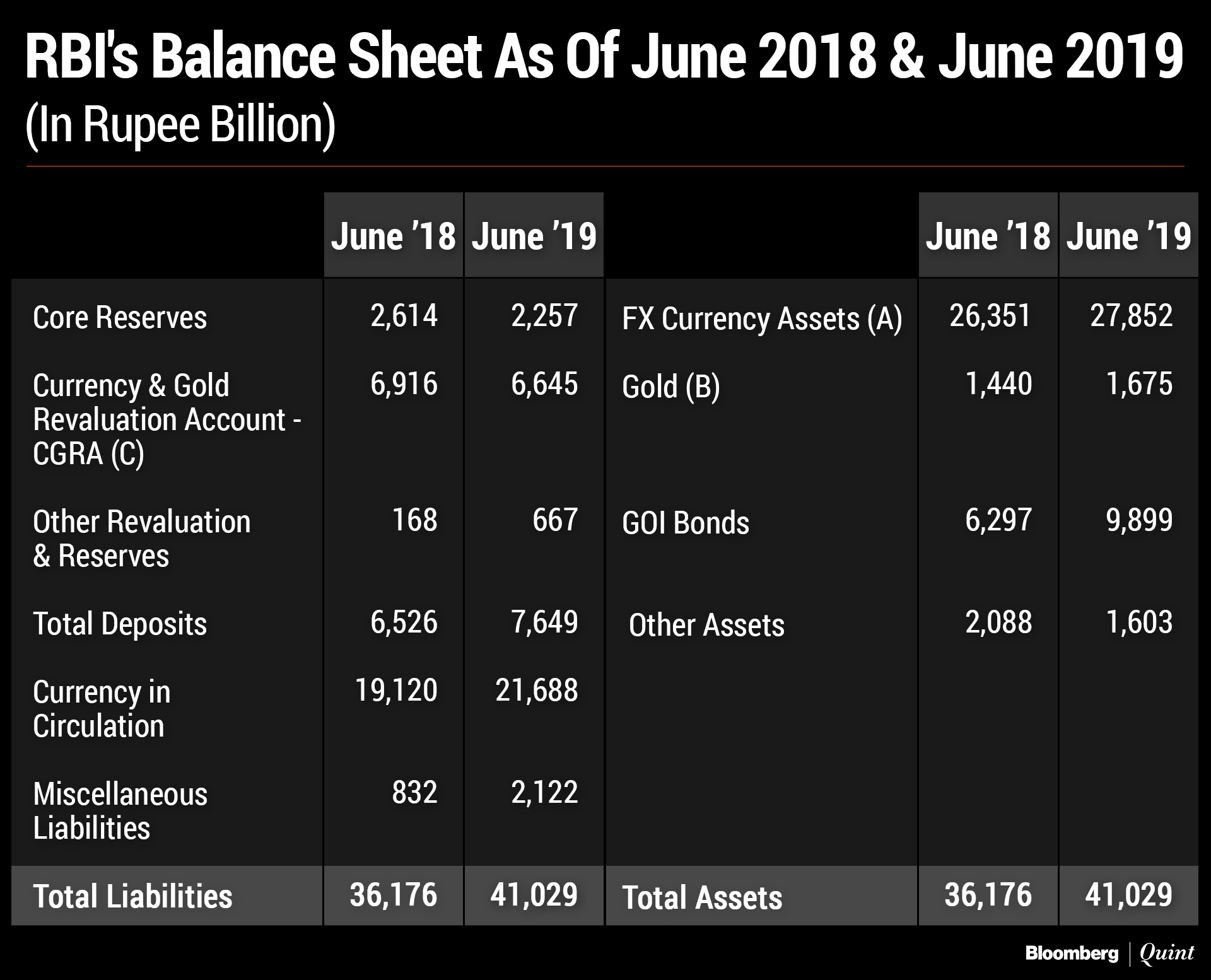

The table below provides a snapshot of RBI's balance sheet as of its year ending June 2018 and June 2019 respectively.

As of end June 2018, the RBI held $405.7 billion equivalent of foreign currency and gold, accounting for nearly 77 percent of its total assets. These were valued at Rs 27,791 billion as of end June 2018 (A+B on the table above), far higher than their original acquisition value in Rupee terms.

Foreign currency assets are revalued by RBI on weekly basis. The notional gain or loss arising from this revaluation is not recognised as income – instead, it is taken directly to its balance sheet into the Currency and Gold Revaluation Account as a reserve (C on the table).

Fresh foreign currency and gold purchases add to the total inventory of currency and gold assets and are subject to periodic revaluation (into CGRA), as described above.

This part of the revaluation and accounting policy remains unchanged. What has changed from FY19 is specifically how foreign currency and gold sales are now accounted by the RBI.

Till FY18, the selling rate of any foreign currency sale by the RBI was compared with the extant revaluation rate, and only this difference was taken to the RBI's profit and loss account. This meant that a bulk of the change between the actual historical (usually low) acquisition rate and the eventual (usually higher) sale rate of foreign currency remained locked in CGRA, and was never recognised as crystallised profit and loss.

Compared to the more conventional inventory valuation methodologies (Last In First Out, First In First Out, or Weighted Average Cost), this was an anomaly.

Alongside Rupee depreciation, this accounting method resulted in the ballooning of the CGRA over time.

From FY19, the selling rate of any foreign currency sale by the RBI is now compared with the Weighted Average Holding Cost of the currency, and this difference is taken to RBI's income statement as realised profit (or loss) from the CGRA.

Given that this is a historical anomaly that is sought to be addressed, the accumulated quantum of money that can be unlocked is very, very large.

Estimating RBI's Weighted Average Holding Cost Of Foreign Currency

There are serious information gaps that come in the way of us estimating any currency WAHC on RBI's books.

To start with, data around RBI's holdings and acquisition cost in different assets such as U.S. dollar, pound sterling, euro, yen and gold is not publicly available. As an extension, we do not have the split of RBI's CGRA reserve across gold and other individual currencies. We can nevertheless try and obtain a very crude estimate for the U.S. dollar WAHC.

Based on the timing of RBI's historical gold purchases, we estimate that 70 percent of RBI's gold assets as of June 2018 are revaluation gains. Of the Rs 6,916 billion of CGRA as of June 2018 (C in the table earlier), therefore, we estimate that only Rs 5,916 billion pertains to currency alone.

With this, RBI's effective foreign currency acquisition cost as of June 2018 amounts to Rs 20,435 billion, being the difference between current foreign currency value Rs 26,351 billion (A on the table) less Rs 5,916 billion (estimated currency revaluation).

That translates into a June 2018 U.S. dollar WAHC of 53.70, if all of RBI's $380.7 billion foreign currency reserves were held in dollars. By applying a similar logic, we find that the dollar WAHC increased to around 55.70 as of June 2019.

In reality, the pound, euro, dollar, yen, gold etc. would have different WAHC relative to current market price. For instance, given the sharp fall in the pound-dollar rate the past few years, the pound WAHC would likely be much closer to current market prices than dollars.

Estimating The Income Impact Of This Accounting Change For FY19

The table below provides RBI's month-wise gross purchase and sale of currency assets (in U.S. dollar terms) during FY19.

During July 2018 and June 2019, the dollar-rupee rate ranged between 68.50 and 70.50, significantly higher than the dollar WAHC between 53.70 and 55.70 in that period.

Assuming an average difference of 15.00 between average sale rate and the WAHC, a realised profit of Rs 532 billion would have been unlocked from CGRA on the gross sales of $35,464 million during FY19.

It is worth noting that notwithstanding the gross sales across months, RBI actually net purchased $8,959 billion during FY19.

Reconciling The Statements In The RBI Annual Report

As mentioned earlier, the RBI provides very sketchy information about this very significant accounting change.

The report states “During the year, exchange gain/loss has been computed using weighted average cost method resulting in an impact of Rs 214.64 billion. Certain items of income such as …exchange gain/loss from foreign exchange transactions are reported on net basis.” Surprisingly, this is the sole direct mention of the change in the accounting methodology in the annual report.

This impact number of Rs 214.64 billion is significantly lower than the Rs 532 billion that we estimated earlier. Perhaps a significant chunk of the $35,464 million of gross sale was of a foreign currency other than U.S. dollar. As mentioned earlier, the WAHC of the pound is likely much closer to the current market rate, in comparison to the dollar.

At another point, the report states “During 2018-19, the balance in CGRA decreased by 3.93 per cent from Rs 6,916.41 billion as of June 30,2018 to Rs 6,644.80 billion as of June 30, 2019 mainly due to depreciation of major currencies against US dollar, partly compensated by the rise in the international price of gold.” This statement omits to point out that the change in accounting methodology itself would have led to a drawdown of Rs 214.64 billion from the CGRA, going by the report's own earlier statement.

Overall, the commentary around this very significant accounting change is very thin.

Why Is This Accounting Change Significant?

If our estimate of the dollar WAHC of 55.70 as of June 2019 is reasonable, any gross sale of dollars by the RBI at current market prices of around 71.50 would unlock significant recognised profit and loss from the CGRA, irrespective of the net sale/purchase.

Gross sales of $100 billion, at an average sale rate of say Rs 16.00 higher than the dollar WAHC would unlock Rs 1.6 trillion of CGRA realised gains – far more than even the high core surplus of Rs 1.23 trillion registered this year.

In fact, commercial banks often ‘churn' their assets with near simultaneous sales and purchases to unlock revaluation gains.

Granted that the RBI is not a commercial bank. But gross currency sales of $100 billion need not be unrealistic or illegitimate. For instance, if the RBI were to seek to reduce market volatility and keep the dollar-rupee rate in a range, it could inevitably end up both buying and selling foreign currency around that band.

Do The Jalan Committee Recommendations Limit RBI Surplus Payouts?

One school of thought is that the Jalan committee's requirement to keep RBI's Available Realised Equity (ARE) at 5.5 percent of balance sheet, and Economic Capital (EC - the sum of realised equity and revaluation reserves) between 20 percent and 24.5 percent, would limit RBI surpluses in future, as the balance sheet grows.

This misses two points. First, RBI's EC stood at 23.3 percent of the balance sheet as of June 2019. Under the Jalan committee recommendations, the EC can drop down to 20 percent. To that extent, as much as Rs 1.3 trillion more of realised profit and loss could theoretically have been realised out of the CGRA even in FY19.

Second, a bulk of future increases in the RBI balance sheet could accrue from rupee depreciation, with a concomitant increase in both the value of foreign currency assets and CGRA. The increase in CGRA would effectively increase the Economic Capital to that extent. While RBI's ARE would need to be enhanced by 5.5 percent of this increase in balance sheet, 80 percent of the CGRA increase can be realised and paid out as surplus.

Is Realisation Of Crystallised Currency Gains Kosher?

Seen through commercial eyes, such crystallisation of revaluation gains does seem appropriate. After all, if assets have been acquired at a low cost, gains should be recognised when they are sold.

But what when the assets are not really sold? What if there are gross sales and gross purchases but little or no net sales of assets, as with RBI's currency operations in FY19?

More broadly, does the commercial logic of marking-to-market an asset apply to a central bank like RBI?

The Bottomline – Money for Nothing

Ultimately, perhaps it is important to debate the impact of of this RBI monetisation of the government, rather than just the justification for the monetisation.

When RBI credits the account of the government on its books, either by way of transfer of surpluses or by purchasing government bonds, it effectively creates money for the government to spend.

Over the past twelve months, with Rs 3.5 trillion of bond purchases through open market operations and now Rs 1.76 lakh crore of surplus transfer, the quantum of monetisation is higher than the annual net borrowing program of the central government.

We already are deep in the midst of an uncharted print-and-spend cycle.

In the wake of very weak economic sentiment, slowing growth, stressed sectors of the economy and stretched fiscal balances, printing and spending sounds like a seductively simple masterstroke solution to our economic ills. However, past experiments of this nature have invariably ended badly. This time around feels different, but is it?

Ultimately, we need to debate and decide whether continued monetisation of this magnitude is truly the answer to our core economic issues, or will it eventually threaten our external balance, inflation and financial stability.

Ananth Narayan is Associate Professor-Finance at SPJIMR. He was previously Standard Chartered Bank's Regional Head of Financial Markets for ASEAN and South Asia.

The views expressed here are those of the author and do not necessarily represent the views of BloombergQuint or its editorial team.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.