When market sentiment is not great, you will likely come across several blog posts, marketing inserts, ‘experts' on television; all counselling you about the long-term nature of equity markets, how patience pays etcetera. If you are like me who pauses to read anything at all on behavioral finance, you may have even come across a few recent articles on ‘recency bias.'

Simply put, this bias is the tendency to overweight recent events. So, if you were sulking due to a prolonged heavy loss in your portfolio, you were exhibiting recency bias. Conversely, if you were feeling over-joyous over a brief rally, or a great momentum-driven stock pick, you were doing the same. Not too many people point out your recency bias on the upside. After all, it doesn't serve the marketeer's purpose – of shaming you.

I don't know about you but I am not a big fan of ‘shaming' as a marketing tool.

Think of that time your hairdresser sold you unnecessary products for dandruff that you may or may not have had, insisted that you needed a spa or facial that cost you a fortune – how many times would you have fallen prey to that tactic? Now just project your salon experience on your portfolio.

Note To Clients 1: If You Are Loss-Averse, There Is No Reason To Be Ashamed

Loss-aversion is not just natural, but it is also part of evolution. Forget being ashamed for it, pat yourself on your back that you haven't lost your survival instincts. Here's why.

As human beings, we are wired to be loss-averse. Amos Tversky and Daniel Kahneman, who were mentors to the father of behavioural economics, Richard Thaler, have written extensively on the same. One of their key findings is the following:

Given a loss and a gain of equal value, the loss hurts almost twice as much as the gain feels good.

Tversky even had a little joke – “There once, was a species that didn't exhibit loss aversion and now, they are extinct”.

There is a certain set of people who thrive on taking risks – are you sure you are one of them? If you lose sleep over downswings you may want to take a good, hard look; at your risk profile?

Note To Clients 2: You Can Call Out This Bluff

The next time, you read or hear anything from anyone, (particularly from fund houses) on recency bias, shaming you, do the following:

1. Ask your wealth manager to share performance data over long periods.

See if the fund was in the top quartile during better times, or ever. This will help you find out if a perpetually-underperforming fund is just hiding behind new-found jargon, and finding new ways to dupe you; or is it just an honest take, over-simplistic maybe, carefully timed even, but perhaps not in bad faith.

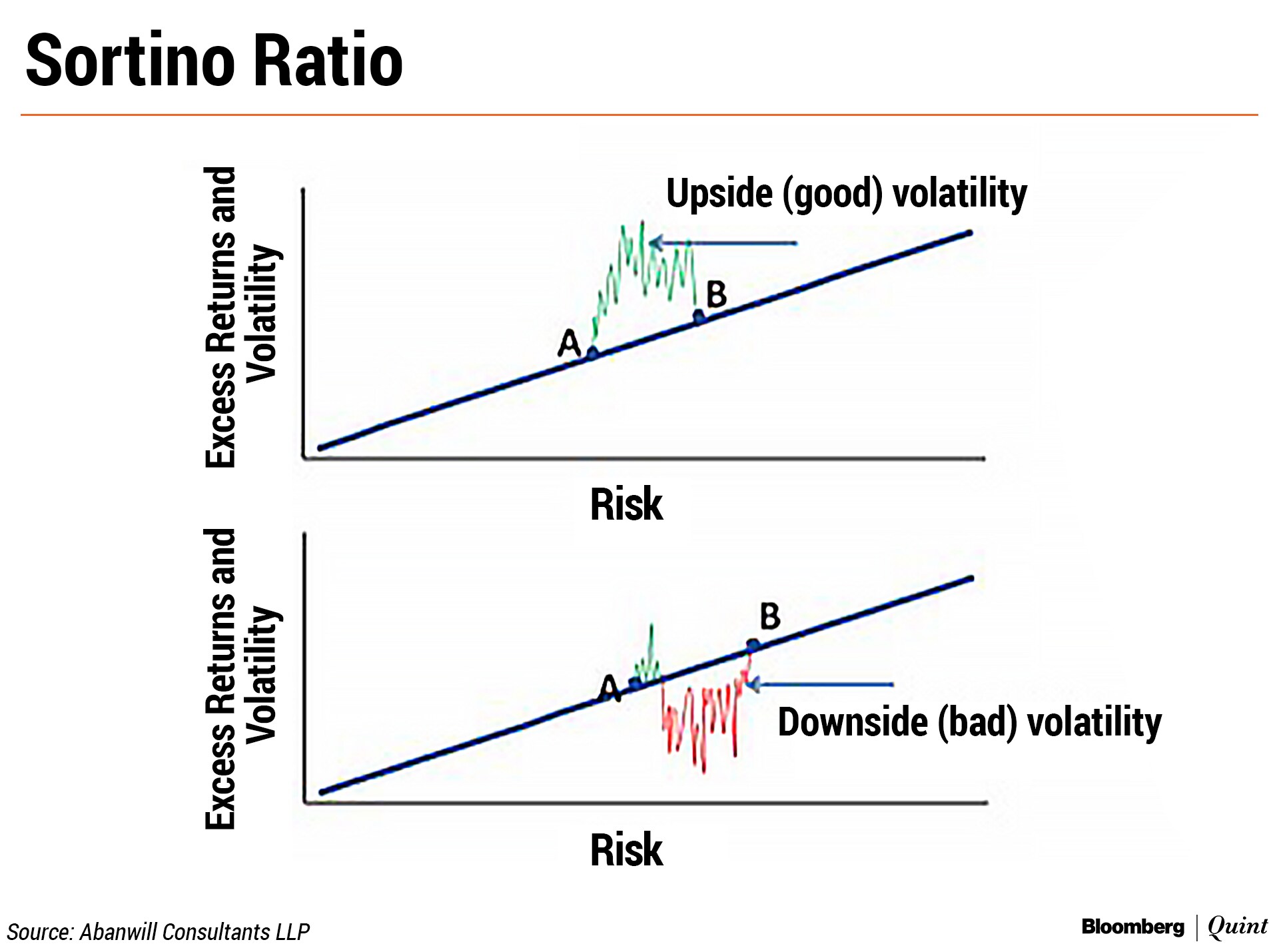

2. Learn about the Sortino Ratio.

Volatility can occur on the upside, as well as the downside.

The Sortino Ratio reflects how much your fund is yielding for a given level of ‘bad' volatility. The higher the Sortino, better your fund is, as illustrated below. Now, look at this ratio for the fund in question.

If the fund has a low Sortino Ratio, it means a recent fall in your portfolio may not bode well for the immediate future as well. I suspect it won't be great for the distant future either.

It is true that

- Equities are volatile.

- During a downturn, it is important to stay the course.

- It is a bad idea to stop your systematic investment plans.

It is also true that

- One could use a market downturn to hide underperformance through some smart marketing.

- All and sundry could try preaching patience to clients without really getting into what their investments are. Some may be very poor choices.

- Others could wax eloquent on technical stuff you, or they, know little about.

For example, telling clients that they have ‘recency bias' when a portfolio is down 30 percent or thereabouts, is... well, not cool.

No matter how ‘risk tolerant', nobody likes to see their portfolios down by that much or more. If that were to sustain, who would?

Note To Clients 3: Correctly Assessing Risk Profile

Years of marketing efforts have convinced many of us that we all are bulls whereas we may just be bears, or rabbits or something that is even more scared. Say no right in the beginning.

If you are not a bull, don't let your portfolio resemble that of one.

Insist on creating a risk-free portfolio first so that you don't have to touch the volatile one if you ever needed funds.

Many of us know how it feels to dip into one's equity portfolio for any large need. Don't fall for that trap.

The real reason for feeling jittery during downturns is that we don't allocate assets properly. We get greedy, we buy sub-par quality stocks and/or try and pick stocks on our own, take risks we don't understand and exhibit several biases that are harmful in the long-run. If the markets are in a bull phase, everything seems right and we are led to believe that we are good at risk-taking.

The behavioural coaching that you need and your advisor should then provide is:

- To not confuse luck with skill,

- To not exhibit overconfidence,

- To not react to the noise.

I believe that those of us that make up the community of financial advisors should take full responsibility for asset allocation. The road to that is sometimes a little tricky. To determine the client's risk profile, we usually rely on a questionnaire that throws up a ‘tolerance score' - Now, this could steer clients down a horribly wrong lane.

The best risk profiling tool I have used isn't perfect but it does touch upon the subtle difference between what one thought one's risk tolerance was and what it actually is. Clients may often be tempted to take on more risk in anticipation of returns, but that is not really their tolerance level. Those who have managed clients for long, know who the genuinely risk-tolerant ones are and who are not.

In the meanwhile, my request to some ‘experts' is – “please don't put out strange half-baked stuff on behavioural finance”. We are all learning, and we don't want to learn incorrect things.

As for you, dear clients, you should know that shamers and blamers are just gamers – develop a knack to spot them and stay far, far away.

Abaneeta Chakraborty has close to two decades of experience in managing money for ultra-HNI families. She founded the firm Abanwill Consultants LLP in 2017 to provide independent views on investing.

The views expressed here are those of the author and do not necessarily represent the views of BloombergQuint or its editorial team.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.