The Indian financial services sector has seen the launch of account aggregator services, which signals a sea-change in the manner that the financial consumers can access and transmit their account information and financial data held by various financial services companies to other financial services companies or to themselves.

It brings together unparalleled access to financial data, control over such data, and technology to enable secure transmission of such data, with due consent and control by the financial consumers. It is a techno-legal framework like no other in India or indeed around the world.

This techno-legal framework is underpinned by the Reserve Bank of India's licensing and registration of account aggregator companies, and its master directions which govern the financial information providers (FIPs), the financial information users (FIUs), the account aggregators (AAs), and the manner in which financial consumers can utilise such services.

Sahamati, a collective of the financial and technology service providers in the account aggregator ecosystem is harnessing several legal innovations which are worthy of note.

Utilising a revolutionary open-architecture multipartite contractual framework (dubbed ‘ecosystem terms') enabling easy signup by the three sets of financial institutions — FIPs, FIUs, and AAs — which eliminates bilateral negotiation and contracting process among or between them, and instead interlinks all three sets of financial institutions with uniform, common terms based on the RBI master directions.

Principles of interoperability, interdependency, and reciprocity are captured in the ecosystem terms among the participants which are also a reflection of the technical standards envisaged in the Sahamati AA ecosystem.

An evolutionary character: changes based on experience, feedback, and technological advances are possible with the least amount of friction.

Building of an advanced, multi-tiered dispute resolution process built on a parallel techno-legal advancement that has taken place: automated dispute resolution and online dispute resolution.

While each of these innovations may be deserving of an essay, this article focuses on the advanced multi-tiered dispute resolution process adopted by Sahamati and its constituents reflecting its three-pronged approach.

Such a dispute resolution process would give a whole lot of comfort and confidence to the financial consumers interacting with the Sahamati AA ecosystem on potential or actual issues, concerns, complaints, grievances, or disputes which may arise.

Effectively Addressing The Concerns Of Financial Consumers

Clearly, in a multipartite platform having interdependencies, and which requires secure, speedy, interoperable protocols, a financial consumer may have an independent contractual linkage with each of the participants and also with all of them simultaneously when using the AA services.

Any breakdown in the service could involve multiple participants. The breakdown could be around any one or more of the features of the AA service: breach of data security or failure of encryption, delay in transmission of required data, or failure of interoperability, and so on.

While technology can (possibly) help pinpoint the specific point where the breakdown occurred and therefore which participant/s is/are responsible, it could look daunting to Miss A.

The TLDR Explainer

Sahamati seeks to ease the process of resolving issues, concerns, complaints, or grievances considerably for Miss A and for each financial consumer interacting with the Sahamati AA ecosystem.

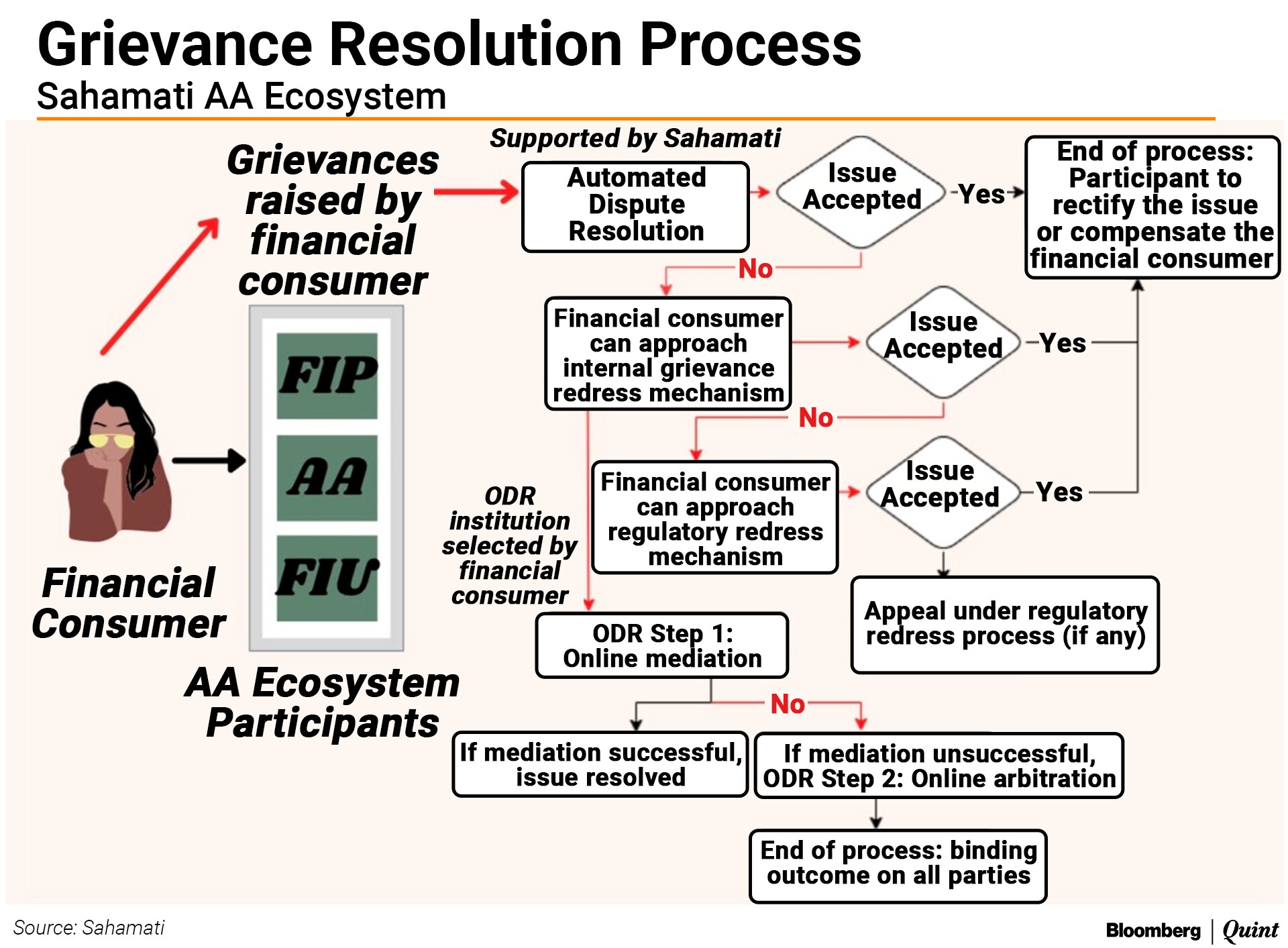

So, when Miss A as a consumer of the AA ecosystem, encounters an issue or has a concern, complaint, or grievance, she would have recourse to the following systems in a sequential and linear manner:

An automated dispute resolution system

The issue when logged, would be cross-checked against the records and databases of the relevant participants and either accepted or rejected.

If accepted, the relevant participant at fault would rectify the issue or compensate the consumer.

Sahamati would keep evolving the issues that can be addressed in the automated mode.

Internal grievance redress mechanism of the participant

If the automated mode has not addressed the issue or has rejected the complaint, the consumer can raise it to the internal grievance redress mechanism.

Many names, one job: internal grievance redressal is undertaken by nodal officer or grievances redressal officer or internal ombudsman.

Evaluates the issue, checks internally what transpired, and provides a finding that accepts or rejects the issue. In case of acceptance, the participant rectifies the issue or compensates the customer.

Regulatory redressal mechanism

If the issue is unresolved by the internal redressal mechanism, the consumer can approach the regulatory redressal mechanism – RBI Ombudsman, SEBI Complaints Redress System or SCORES, IRDAI Grievance Redressal Cell, PFRDA Grievance Redressal Cell.

Some of these mechanisms have a system of appeal as well.

Online dispute resolution mechanism

If the issue cannot be resolved under the regulatory redress mechanism for any reason, two further mechanisms are provided by Sahamati:

Online mediation (a process of consensual resolution of issues among the disputing parties); or

Online arbitration (an independent, neutral arbitrator deciding on the matter after examining the submissions of all the parties. Obviates having to go to courts for relief or remedies.)

For a more detailed read, see the anatomy of the multi-tiered dispute resolution process.

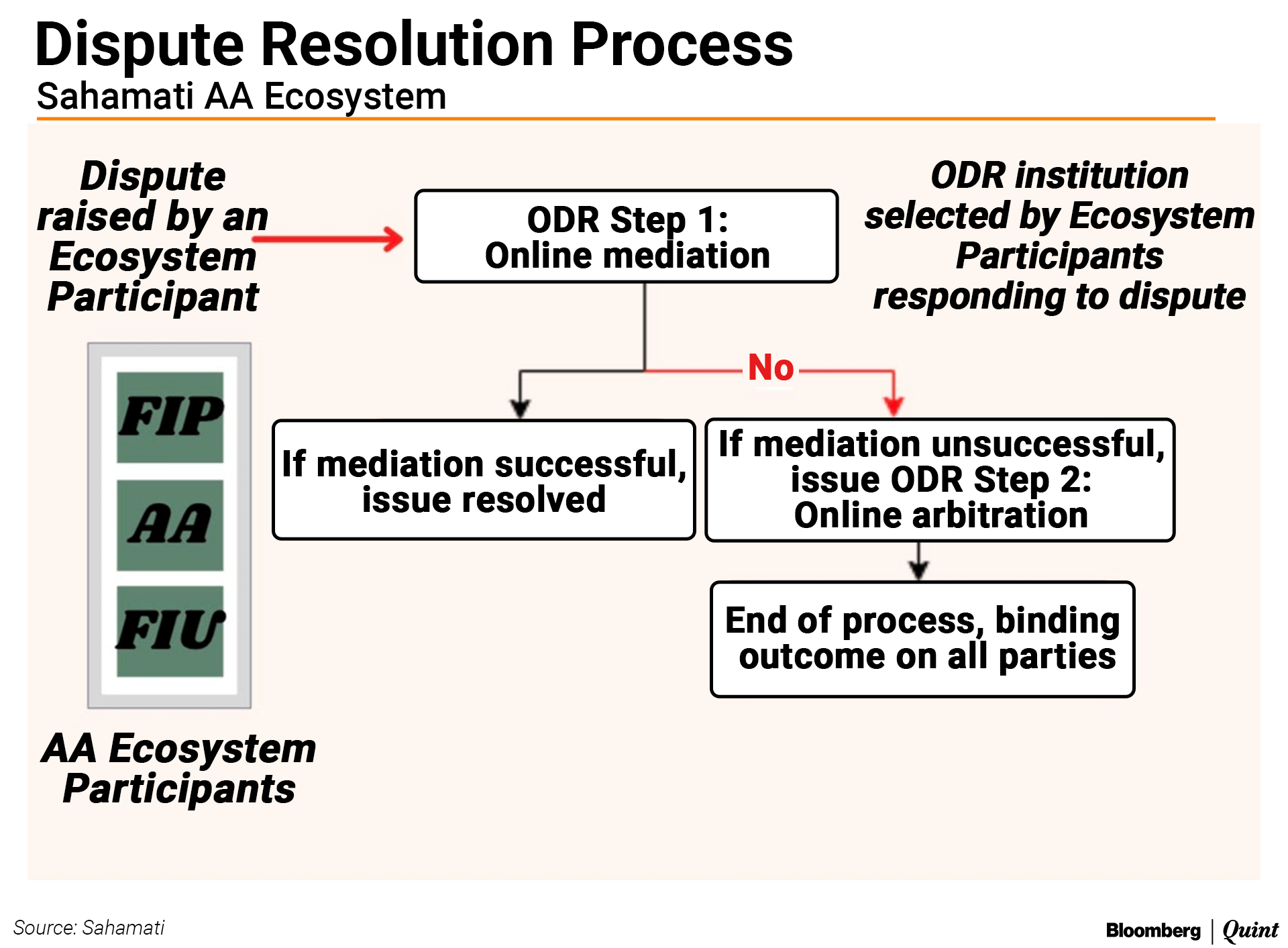

Addressing Disputes Between Participants

It is entirely within the realm of possibility that one or more of the participants within the AA ecosystem—the FIPs, FIUs, or AAs—themselves may have issues, concerns, or disputes with one or more other participants.

Sahamati anticipates such situations and possibilities and requires the participants within its AA ecosystem to resolve such disputes by utilising the ODR institutions as empaneled.

Accordingly, for dispute resolution involving two or more participants, the ODR institution will provide online mediation as the first level of the resolution process.

If the mediation process is not acceptable or no resolution can be arrived at, then the ODR institution shall provide online arbitration as means of resolution. The outcome of the arbitration is binding on all parties.

Conclusion

In any new financial product or financial service offerings, there is bound to be anxiety or worries on how the financial product provider or financial service provider will address the issues, concerns, complaints, or grievances of the financial consumers.

In the AA services, Sahamati has taken the lead in fostering an ecosystem approach, which eases how the participants come together and makes it convenient for financial consumers. Sahamati has also stipulated for its participants a multi-tier dispute resolution process, which keeps pace with technological advances, and makes available speedy, cost-effective resolution processes (including automated dispute resolution process and online dispute resolution), and fosters the use of APIs to facilitate a smooth transition from one tier to the next or in the choice of ODR institutions.

Indeed, time will tell whether the multi-tier dispute resolution system meets the needs of the financial consumers of the AA ecosystem, and keeps pace with the open banking and finance revolution that the AA ecosystem enables. Sahamati's success in pioneering a transparent, effective, multi-tier dispute resolution process could also serve as an inspiration for other open-architecture platforms to consider harnessing.

In the meantime, financial consumers (including Miss A) interacting with the participants within the Sahamati AA ecosystem can leave behind their anxieties or worries and draw a high level of comfort and have confidence that the best possible design elements to ensure convenience, fairness, and transparency, harnessing the power of technology and techno-legal framework (of automated dispute resolution and online dispute resolution) is on their desktops and in their palms.

Pramod Rao is Group General Counsel at ICICI Bank, and also a member of the Advisory Council of Sahamati, contributing to its legal and governance aspects. Views are personal.

The views expressed here are those of the author and do not necessarily represent the views of BloombergQuint or its editorial team.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.