We in India are subjected to a great deal of hype about Indian information technology, and sometimes we are a bit jaded about it. The hard facts are, however, very impressive. IT is now the biggest industry. Software and services exports are the big Indian success story. After the pandemic, all around us, the economies of Sri Lanka, Bangladesh and Pakistan went into dark crises, and it seems one big thing that protected India was the revenues from services and IT exports. The global firms operating in India—such as Tata Consultancy Services Ltd., with a market capitalisation of Rs 11.6 trillion, and Infosys Ltd. with a market capitalisation of Rs 5 trillion—are a major source of hope about India.

In a recent article in the Business Standard, KP Krishnan asked the interesting question: What elements of Indian policymaking get credit for these achievements?

Three parts are clear:

The establishment of the IITs and IIMs, which created the seed corn of scientific and management knowledge, around which millions of people were able to learn.

Telecom reforms, which removed the government from the telecom industry.

The equity market reforms of the 1990s, with the establishment of National Stock Exchange and Securities and Exchange Board of India.

There is a fourth element: The reduction of barriers to cross-border transactions.

At the end of the Second World War, the global consensus was in favour of capital controls: it was felt that international trade is a good thing, but capital flows should be controlled by governments. The emergence of modern economies made capital controls practically infeasible.

"Finance follows trade": Where international trade takes place, there is inevitably a ladder of sophistication with trade finance, currency risk management, and foreign direct investment. Globally, diversified portfolios have about half the risk of single-country portfolios. Developing countries face higher asset prices (i.e. reduced cost of capital), when capital comes in from overseas. Political freedom and rule of law are hard to reconcile with capital controls. All these factors came together, and the post-war consensus was abandoned.

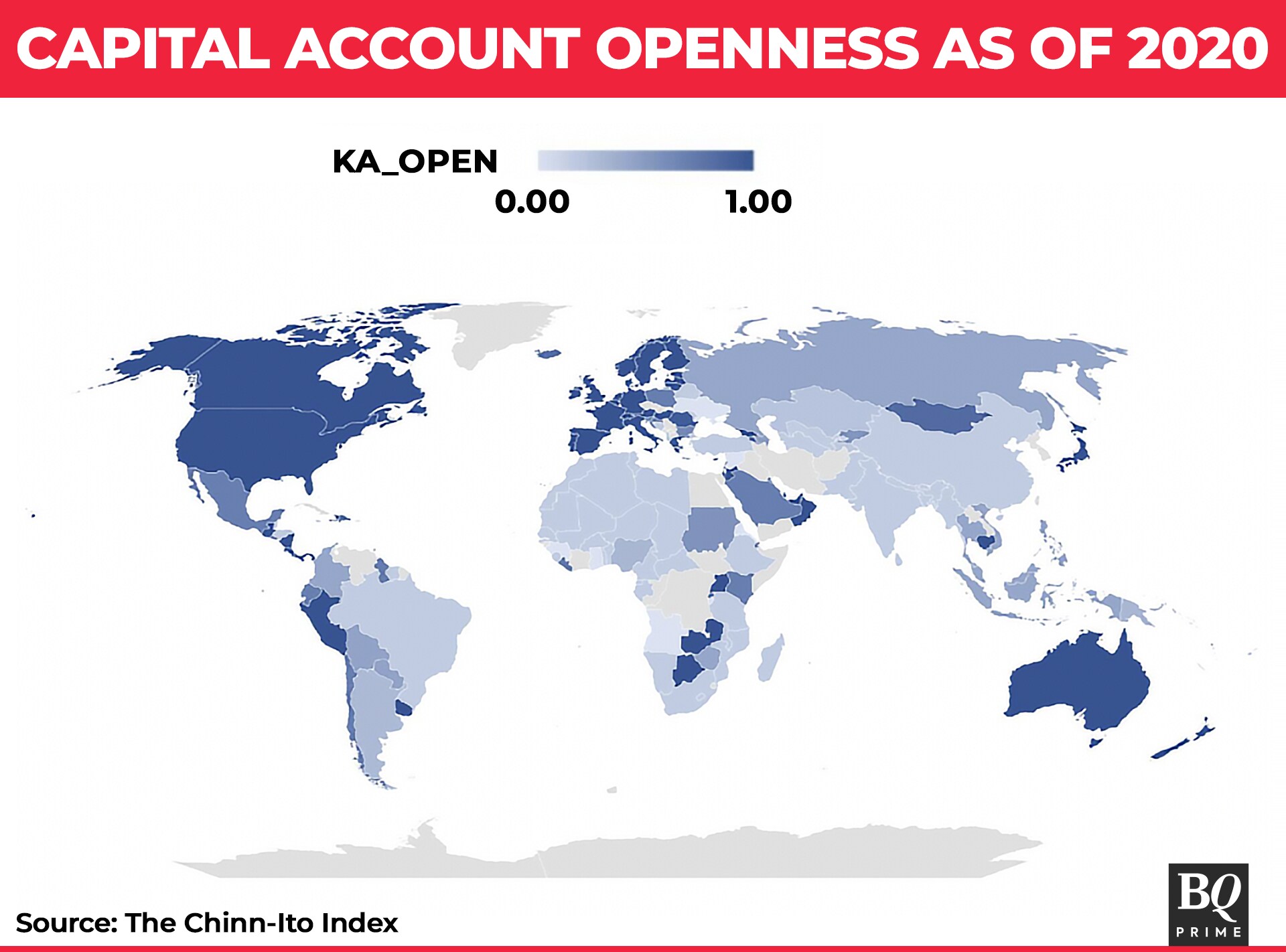

In 2006, Menzie D. Chinn and Hiro Ito introduced an index to measure de jure financial openness of countries across the world. The Chinn Ito index measures a country's degree of capital account openness. The figure below shows the global map of financial openness in 2020, based on this index (normalised, 1 to 0). The darker the country's map, the more open it is. As the figure shows, the advanced economies have fully removed capital controls. The last exponents of big administrative capital control systems are China, India and (after the Ukraine war) Russia.

Under Indian socialism, the Foreign Exchange Regulation Act, 1973 imposed severe restrictions on cross-border financial activities. To understand the practical implications of these regulations, an example would be useful. Aviation fuel was purchased by paying in foreign exchange. Exchange control regulations restricted such exchange. Consequently, a person intending to travel abroad had to first procure an approval from the Reserve Bank of India, that such international travel was necessary in national interest. Only then could such a person be allowed to purchase an airline ticket.

Such severe restrictions were relaxed slowly over time, from 1978 through 1980s, and then more rapidly during the economic liberalisation of the early 1990s. In August 1994, India formally adopted current account convertibility, by accepting the obligations under Article VIII of the International Monetary Fund's Articles of Agreement. From 1997 to 2003, various current account restrictions on residents were gradually liberalised. This new policy found statutory recognition in Section 5 of the Foreign Exchange Management Act, 1999. This provision empowered any person to sell or draw foreign exchange to or from an authorised dealer, for current account transactions, subject only to 'reasonable restrictions' that the central government may prescribe in consultation with the RBI.

As part of this liberalisation strategy, the Liberalised Remittance Scheme was introduced in 2004. LRS allowed resident individuals to remit funds abroad, for current or capital account transactions or a combination of both. The LRS limit has been gradually increased from $25,000 per year in 2004 to $2,50,000 per year at present, albeit not in a linear progression. By reducing the friction in purchasing goods and services internationally and minimising the transaction cost of global portfolio diversification, LRS greatly enhanced the financial freedoms of Indians. These reforms facilitated IT and services exports from India. Tens of thousands of people in India got deeply integrated—at the level of technical knowledge, business knowledge, and culture—into advanced economies.

Many Indians now lead a substantially cross-border life, with a spectrum of connections ranging from travel to work visas. When we look at modern Indian software-as-a-service companies or Silicon Valley startups with a development centre in India, the line between the Indian and overseas activities is thin. None of this would have been possible with the old world of currency controls, where an individual was given a quota of $8 per day when travelling abroad, where having dollar bills could get you into jail. Some of us remember how exhilarating it was, in the early 1990s, when Indian credit cards first started working overseas. It is, after all, quite hard for persons living in India to have a personal and professional life abroad, without the ability to spend, using credit cards.

These reforms also paved the way for foreign investment, which made the market value of Indian software and services companies possible. The world over, there is the problem of "home bias"—investors tend to over-invest in their own country. This is rooted in asymmetric information—you will not readily invest in, say Brazil, as you have so little knowledge about Brazil.

For global investors to get invested in India, a tremendous social process had to take place, of personal engagement by them with individuals from India. This social engagement has taken many forms, including the role of NRIs, of persons of Indian origin, who studied in universities abroad, and intensive overseas travel and business activities of the leadership cadre living in India. All these benefits came from liberalisation of cross-border money flows.

While India has moved towards greater openness in cross-border movements of money over the last three decades, this has been done only partially and with great hesitation. These reforms did not add up to true convertibility on the current account. Convertibility on the current account means the freedom to covert INR into, say JPY (Japanese yen), with no additional friction. In India, these transactions remained saddled with restrictions and procedural overheads. In other countries, with current account convertibility, residents are simply able to convert local currency into foreign exchange, without the concept of an LRS-like scheme, without “authorised dealers”, without reporting requirements, or a limit of $2,50,000.

In this landscape, we now have two important new restrictions on current account activities.

First, Section 206C (1G) of the Income Tax Act, 1961, was introduced in 2020. It required, for the first time, 5% of certain remittance transactions under the LRS route to be collected from the buyer (or person remitting), as income-tax collected at source. The Finance Act, 2023 now broadens the ambit and quantum of this TCS. From July 1 this year, 20% of most remittance transactions under the LRS route would be collected as TCS. While this amount can always be recovered by the individual at the end of the tax year, this provision imposes a significant financial and administrative burden on all Indians using the LRS route. It eases the job of the tax administration at the cost of imposing disproportionate restrictions on the financial freedom of Indians.

Second, a resident individual was earlier not required to repatriate funds, or income generated out of investments made under the LRS route. This rule was suddenly changed in August 2022. Any foreign exchange acquired through the LRS route, unless ‘reinvested', must now be compulsorily repatriated or surrendered by a resident individual, within a period of 180 days from the date of acquisition. This legal change imposes a significant transaction cost on Indians who may wish to hold foreign exchange abroad in a deposit account, to engage in legitimate international transactions such as foreign travel, business, etc. It may also cause confusion and raise disputes. For instance, opinion may vary whether an interest earning savings deposit or a seven-day fixed deposit would be considered as ‘reinvestment' by the regulator.

Such interpretational issues would make implementation unpredictable, further increasing compliance costs under the LRS route.

A small cadre of the Indian business and professional elite is able to connect up into globalisation. Their activities have resulted in the most important economic buoyancy ever seen in India's history. The story is far from complete: India's growth in the coming decade critically relies on these same individuals. The trajectory of policy in India should be to do more of the four policy pathways which got us here—higher education, telecom connectivity, well-functioning equity market, and cross-border freedoms. Cross border activities in India require more freedom, not less.

Ajay Shah is co-founder of XKDR Forum. Pratik Datta is Senior Research Fellow, Shardul Amarchand Mangaldas & Co., New Delhi.

The views expressed here are those of the author, and do not necessarily represent the views of BQ Prime or its editorial team.

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.