Indian financial markets have been going through a turbulent period over the last couple of weeks. Stock markets have slipped and shares of banks and non-banking finance companies have taken a big hit.

Questions like “Is this India's Lehman Moment?” have been raised. The government and the regulators have made statements to assuage the markets and restore normalcy. On Monday, the government moved to supersede the board of Infrastructure Leasing & Financial Services Ltd., which had roiled financial markets due to a series of defaults. The Reserve Bank of India, too, has stepped in with liquidity support.

While the actions of the government and the RBI may restore some degree of calm to the markets, we must use this moment to recognise the deeper problems in the Indian financial sector that this episode has exposed.

How Did We Get Here?

NBFCs and housing finance companies have seen dramatic growth over the last four years, in part, due to some peculiar circumstances in the Indian financial system.

Most public sector banks and some large private sector banks, facing high levels of bad loans, had become averse to lending to riskier segments of borrowers such as small and medium enterprises and lower income borrowers within the housing loans segment (so-called “affordable” housing loans). These banks, however, were willing to lend to NBFCs, whose capital base provides a sort of first default guarantee to banks.

Contemporaneously, the Indian economy was seeing greater financialisation, with both households and corporations moving their savings into financial assets, chiefly mutual funds. Demonetisation, announced in November 2016, fast-tracked this process and led to unprecedented levels of inflows into mutual funds. This groundswell in domestic capital flowing to equity and debt markets, in turn, led to a sharp rise in share prices and fall in interest rates.

On the back of increased valuations, NBFCs could raise equity capital easily. The larger and better rated ones (those rated AA and above) could also easily issue debt paper to mutual funds and insurance companies. They could also raise debt capital at interest rates that were comparable or even lower than those offered by banks.

NBFCs, thus, grew rapidly, essentially taking on credit risks that banks were avoiding. A large number of new NBFCs were established. The number of HFCs went up from around 50 in 2013 to nearly 100 now. New NBFCs and HFCs have lower ratings – typically BBB or below – and hence cannot access mutual funds or insurance companies for debt as these institutions typically invest in papers rated AA and above.

This started a game or rating arbitrage where large, better-rated NBFCs would borrow from banks and funds and lend to smaller, lower-rated NBFCs. The entire NBFC sector started getting intertwined.

When The Winds Turned

These tailwinds for NBFCs began to change course earlier this year.

Driven largely by global factors – chiefly rising crude oil prices, rising interest rates in the U.S., and trade tensions – Indian interest rates started to rise. The yield on the benchmark 10-year government bond moved up from around 6.8 percent to over 8 percent in a period of about three months.

Fresh inflows into mutual funds, especially into debt funds, slowed, and debt fund managers began to adopt a “wait and watch” policy on deploying fresh funds. Liquidity supply to NBFCs began to dry up rapidly. Fresh bond issuances by NBFCs declined and the costs of borrowing rose.

All this preceded the spate of defaults by IL&FS.

And then the news of IL&FS defaults broke. It had two immediate implications.

- First, there was a fear of large scale redemptions in debt mutual funds. So some funds resorted to panic selling of debt securities which sent a negative signal to the entire market.

- Second, the defaults shattered faith in ratings of debt securities. IL&FS debt had the highest rating just a couple of weeks before the default. The rating was revised to the lowest default grade (“D”) after the default occurred. This raised doubts about the quality of other issuers assigned similarly high ratings.

The reaction in the market was vicious. Yields on corporate bonds went up and the debt market almost stalled.

The RBI acted quickly and took steps to inject liquidity via open market operations. Since then calm has returned to the market for securities of less than one year but the market for medium-term securities remains tight.

Even so, the long term structural issues of the debt market still exist. The actions taken so far don't do anything to address these structural liquidity issues. In fact, these actions highlight the limited options the central bank has in addressing such issues.

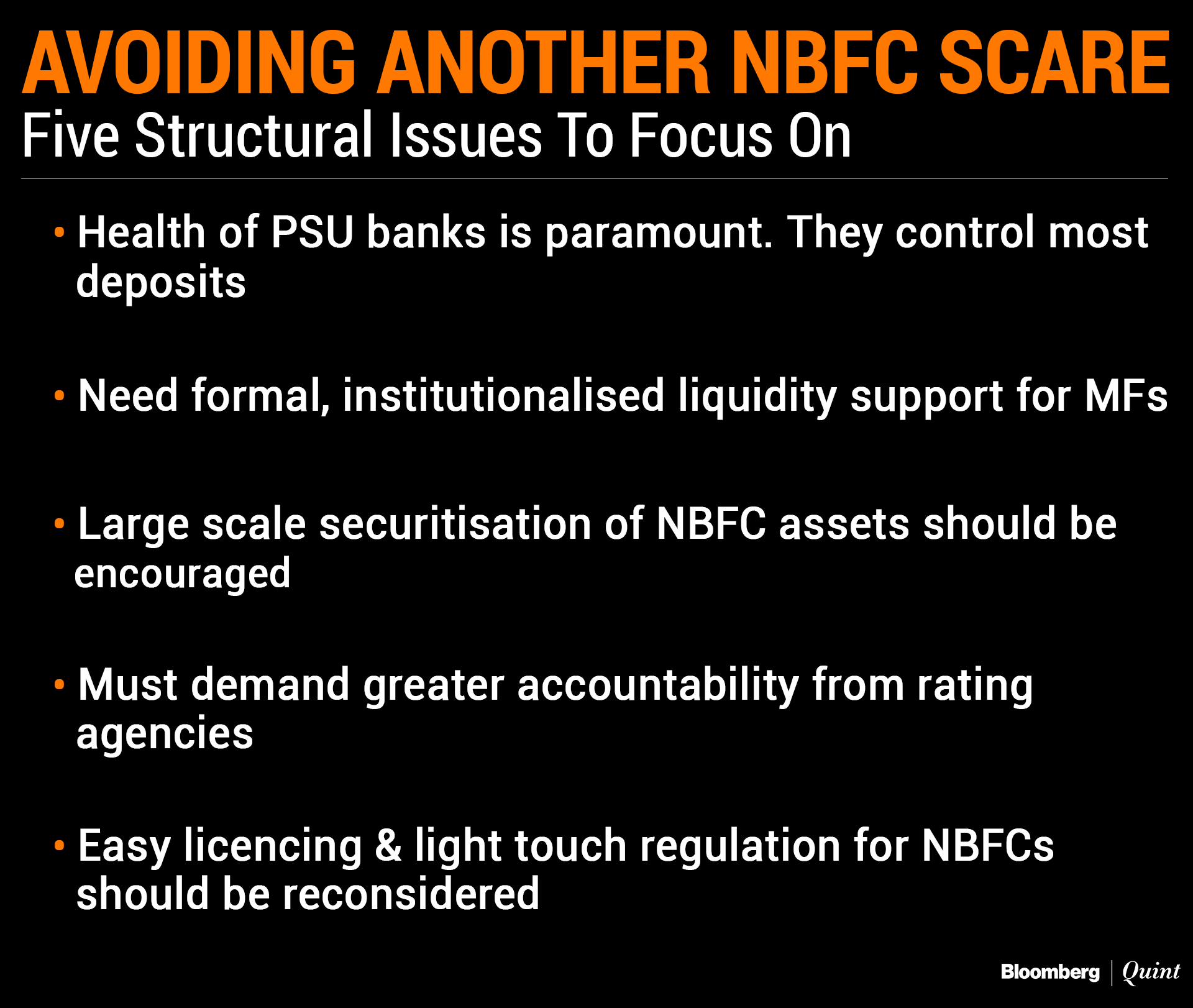

A Five-Point Structural Agenda

If policymakers are serious about avoiding such accidents in the future, they need to focus on a few aspects of the financial system and work towards making changes.

Point 1: NBFCs have a wholesale-funded model and the wholesale funding market is underdeveloped, illiquid, and founded on ratings of questionable quality. These features make the funding market and, by consequence, NBFCs vulnerable to liquidity shocks. All those who thought that the withering away of public sector banks will not matter much as their space will be filled by NBFCs as debt providers, must pause and think again.

As long as primary liquidity, via access to household savings, is with banks (and predominantly with PSU banks), their health is of paramount importance to Indian financial system. RBI can add liquidity at the shorter end of the yield curve as it did over the last few days, but its ability to inject liquidity at the medium and long end is non-existent.

Some have argued for open market operations on the lines of quantitative easing that was followed in the U.S. and Europe as a means to structurally inject liquidity. But that would require the entities needing liquidity to hold tradable securities that can be bought by the central bank. That is not the case with NBFCs, who have loans on their balance sheets and not bonds or asset backed securities.

RBI can inject liquidity into banks who hold large amount of government securities, through OMOs but the only institutions that can inject structural liquidity into NBFCs are banks. They need to start lending again.

Point 2: Debt mutual funds that are invested in illiquid bonds but promise their investors redemption in a day or two, need access to a liquidity window on the lines of the Liquidity Adjustment Facility that the RBI offers to banks. In the midst of the global financial crisis, the RBI had opened its repo window to money market funds for a short time. There is a repo window run by Clearing Corporation of India Ltd. called the Collateralized Borrowing and Lending Operations but it is too small.

Now that the size of debt funds has grown significantly, we need a more formal, institutionalised liquidity support for them so that they can withstand sudden redemption pressures that may arise from time to time.

Point 3: We must encourage large scale securitisation of NBFC assets so that the resulting asset-backed securities can be traded imparting liquidity to otherwise illiquid balance sheets. This is especially critical for housing finance companies.

This would require a relook at the regulations governing securitisation and there is a case for setting up a government backed institution to facilitate such large scale securitisation.

Point 4: We must demand greater accountability from the rating agencies. The entire edifice of the corporate bond market stands on credible ratings. If the market loses faith in ratings, then it cannot exist. Regulators need to take a hard look at the functioning of the rating agencies. In India, even banks use ratings provided by rating agencies for loans. So, the issue of credibility of ratings impact both banks and bond markets.

Point 5: Easy licensing and light touch regulation of NBFCs should be seriously questioned. Most NBFCs depend on banks for funding and hence the risks they underwrite ultimately impinge on the banking system.

Long Debated Depth Of Bond Markets

Finally, the much discussed topic of development of bond markets. While the bond markets in India have grown in size, as measured by value of bond issuances, they have not developed depth. A hundred crore trade in bonds of an issuer with thousands of crore worth of outstanding bonds spikes yields higher, demonstrating the lack of depth in the market.

Liquidity develops when a large number of diverse investors, diverse in their risk appetite, participate in a market. In the bond markets, this can be achieved by opening up pools of capital other than mutual funds and banks such as provident funds, pension funds, trust funds, etc. Provident funds, insurance, and pension funds in India have a debt corpus of around Rs 50 lakh crore, which is almost entirely deployed in government securities. Even allowing a 2 percent increase in the corpus that can go to corporate bonds can inject Rs 1 lakh crore.

Managers of the Indian financial system – regulators, managements, policy makers, and investors – should learn the lesson from the episode that just played out and work towards strengthening the system.

Harsh Vardhan is executive-in-residence at the Centre of Financial Services, SP Jain Institute of Management & Research. He has more than 20 years of experience in consulting to the financial services industry.

The views expressed here are those of the author's and do not necessarily represent the views of Bloomberg Quint or its editorial team

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.