This week had all the makings of what can be called extremely complicated. Filled with cues. More so for the crypto investors, but certainly the risk assets at large. And mind you, it was not that the markets were unprepared, as a story from Bloomberg 36 hours before the U.S. CPI data came out says:

"A cooling in inflation on Thursday could very well set off a relief rally in the stock market. Just don't expect it to stick around for long because it's unlikely that the Federal Reserve will be diverted from its rate-hiking path, even if it slows the pace in December."

This was one instance where, even though it was widely anticipated, the recent disappointments on the inflation front in the U.S. led people to not buy the rumour, but buy the news. That, plus the impact on the Indian landscape and the widely covered crypto news, form a part of this week's piece.

Buoyancy For Risk Assets

Concerns about the Fed's impending tightening were reduced as a result of the headline and core CPI inflation readings of 7.7% and 6.3%, respectively, on Oct. 22, which led to a risk-on trade. This had an impact on U.S. stocks, especially the tech indices, as well as the declining value of the dollar (DXY down 1.8% at 109 versus the most recent peak of 114). Adding to the positive sentiment, China reduced its quarantine time for inbound travellers and scrapped Covid flight suspensions. All these led to strong moves in equity markets, with the Nasdaq posting an over 7% rally in Thursday's trade and Asian markets following suit, albeit not on the same scale. The Fed Fund Futures have also begun to taper, with the July 23 projection dropping from 5-5.25% the day before to 4.75–5.0%. Would this last? One can argue that this was the first of the moves which was CPI-softening led, and there is room for more. Note that before the 7% upmove, the Nasdaq had corrected around 19% in the preceding three months.

Indian IT To Follow Suit?

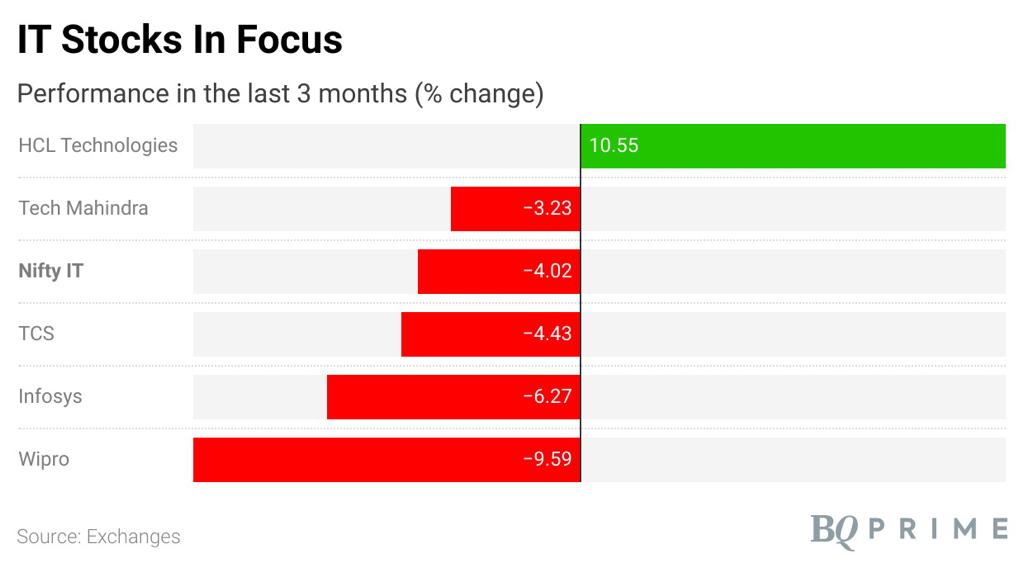

From the Indian markets standpoint as well, there is a good chance that IT stocks, which have been major underperformers this year, should resonate with the positivity of the U.S. tech. Following the Q2 FY23 results, Indian IT companies are still guiding for resilient revenue growth in the near term and margin pressure concerns have eased somewhat. Despite this, when one looks at the stock prices as of Thursday's close (see bar chart below), most of the large-cap IT stocks, save for HCL Tech, were trading deep in the red for the last three months, and therefore, a bounce was the most probable outcome.

Not only IT services, all tech led names shot up on Friday. If Nykaa had double-digit gains, others like Naukri and Zomato surged too. All in all, it is a decent time for IT stocks in India, considering that they have seen corrective moves despite earnings holding out, and risk on in the world on the tech sector might only help sentiment. It must be pointed out though, that the street is not too bullish, with the average return potential for all the Nifty names in the IT services space being less than 10%. Only Tech Mahindra comes close with a 9.6% return potential over the next 12 months.

Case For Some Caution?

All market experts and quant indicators who have recommended caution since the October rally started have had an egg on their face. Partly due to the inherent strength in the Indian markets and partly due to the CPI data led uptick in global markets, there is a short-term case of the optimism continuing. But are there enough reasons for caution? One could argue yes.

The valuations of India are among the highest, if not the highest, in the EM landscape. Sunil Tirumalai of UBS, on the sidelines of the UBS India Conference, spoke about how potentially rising deposit rates can hit savings which have hitherto been coming into Indian markets from the retail investors. There is also a case of how higher crude prices (should China re-open) can impact the CAD and the currency, and thereby have an impact on the Indian markets. For now, staying bullish has helped. But the arguments are strong, and worth pondering over.

Changpeng “CZ” Zhao walked away from his bailout for Sam Bankman-Fried's FTX.com almost as quickly as he offered a rescue. As a story in Bloomberg read, it became evident in a matter of hours that rescuing FTX would be a tall order for Binance. Its executives found themselves staring into a financial black hole—a gap between liabilities and assets at FTX that's probably in the billions. Cryptocurrency prices plunged for a second-straight day after crypto exchange Binance said it was pulling out of a deal to purchase failing rival FTX Trading. Ether, the coin linked to the ethereum blockchain and the second largest cryptocurrency, also tumbled by more than 10% on Thursday to below $1,200. While there was a small uptick post the risk-on mood after the US CPI data, bitcoin remains more than 60% off its all-time high, hit exactly one year ago. In terms of the fallout, the FTX debacle impacts investor confidence in the short to medium term. The scale of losses is yet to be estimated, but rumors are that FTX has a large hole. The cascading effects of this development would be known only over a period of time. However, this side of the investing world remains unpredictable, and events next week would be closely followed.

All in all, a very interesting week has gone by, and would have implications for what follows in the week ahead. After another U.S. inflation surprise, CPI data will be dominating the agenda in most other markets in the coming week, shifting the focus away somewhat from the greenback. The pound will likely attract the most attention as it will be a busy week for the U.K., as apart from the economic releases, the budget statement will be watched amid lingering worries about high borrowing. Growth indicators will be important in China and Japan, while in the U.S., the main highlight will be the retail sales numbers. And in India's case, eyes on the closure of the earnings season and the global sentiment.

Niraj Shah is Executive Editor at BQ Prime.

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.