(Bloomberg) -- Wall Street traders betting the Federal Reserve will be able to cut rates soon sent bond yields tumbling — while driving a rotation out of the tech megacaps that have powered the bull market in stocks.

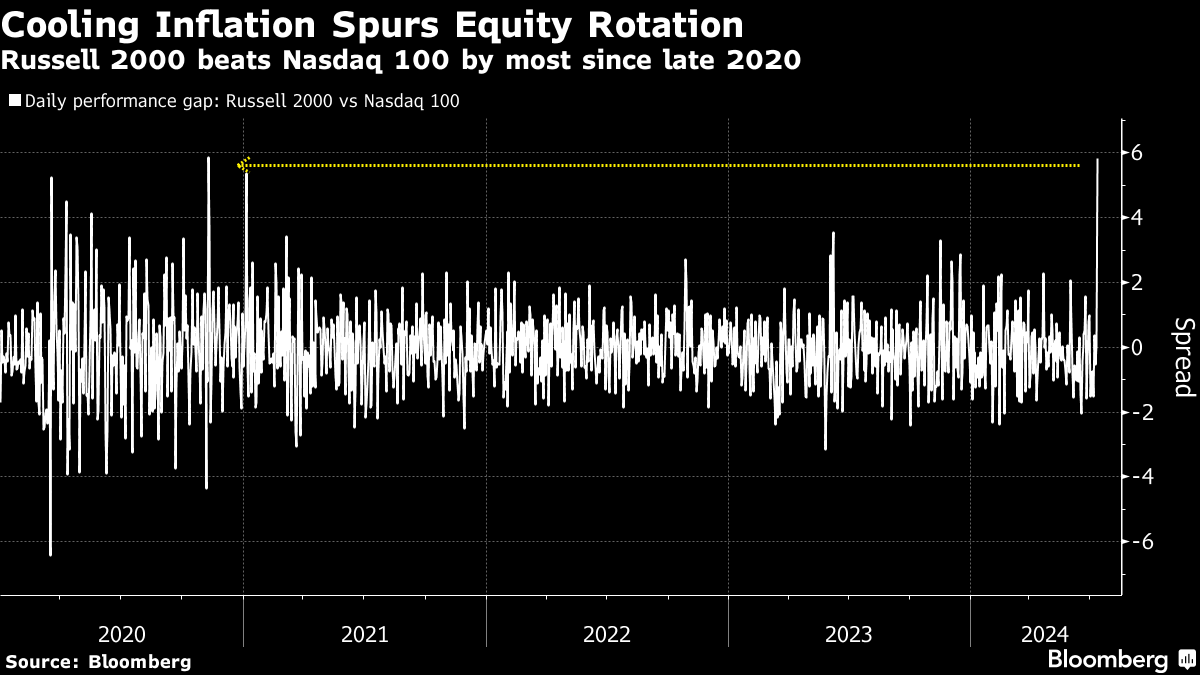

Further signs that inflation is slowing down fueled speculation the Fed will be able to move as early as September. Optimism over lower rates sparked a shift into riskier corners of the market — as money exited the long-favored safety trade of big tech. The Russell 2000 of smaller firms beat the Nasdaq 100 by 5.8 percentage points — the most since November 2020. While the S&P 500 fell nearly 1%, almost 400 of its shares went up.

To Callie Cox at Ritholtz Wealth Management, today could be a turning point for markets. It's also a good reminder that diversifying is important.

“The big tech trade is turning on itself, yet the rest of the market is finally stepping in,” Cox said. “The S&P 500 is down today, but this is the best kind of selloff you could hope for if you're a long-term investor.”

An equal-weighted version of the S&P 500 — where the likes of Nvidia Corp. carry the same heft as Dollar Tree Inc. — jumped. That gauge is less sensitive to gains from the largest companies — providing a glimpse of hope that the rally will broaden out.

The Nasdaq 100 sank 2.2%. A Bloomberg index of the “Magnificent Seven” megacaps slid the most since 2022. Tesla Inc. plunged 8.4% on news it's postponing its planned robotaxi unveiling to October. The rotation out of this year's winners sent the iShares MSCI USA Momentum Factor ETF slumping.

Conversely, the worst-performing sector in 2024 — real estate — had its best day this year. The Russell 2000 climbed 3.6% — the most since November. Financials rose as a group ahead of the start of the earnings season.

Treasury 10-year yields tumbled seven basis points to 4.21%. The dollar saw its biggest drop since May. Japan's currency chief stuck with his strategy of trying to keep market players in the dark over whether Tokyo stepped in to prop up the yen after sharp moves.

US inflation cooled broadly in June to the slowest pace since 2021 on the back of a long-awaited slowdown in housing costs, sending the strongest signal yet that the Fed can cut interest rates soon. The so-called core consumer price index — which excludes food and energy costs — climbed 0.1% from May.

To Chris Larkin at E*Trade from Morgan Stanley, July is still a longshot, but Thursday's “Fed-friendly CPI” got markets one step closer to a September rate cut. A lingering question is whether this high-flying stock market has already priced in multiple cuts, he noted.

At Interactive Brokers, Steve Sosnick says that looking at the moves in the S&P 500 and Nasdaq 100 Thursday, one might eventually think that the “benign” CPI report was bad for stocks. In reality, he said, the data actually helped the vast majority of shares trade higher.

“We are getting a dose of the ‘healthy rotation' that many have hoped for,” he noted. “One day does not a trend make. But as someone who has been advocating and hoping for a broader market rally and a rotation into value from growth, today's activity makes me wonder if I should be more careful about what I wish for.”

Dan Wantrobski at Janney Montgomery Scott says Thursday's market action showcases a notable improvement in overall breadth/participation.

“This fanning out from the narrow leadership areas (Mag 7/AI/megacap) throughout much of this year is what we would like to see continue over the coming weeks and months in order to confirm a healthier expansion cycle on a longer-term basis,” he added.

“It's a pretty swift reversal in the momentum trade, and that tends to benefit the laggards to a significant degree,” said Kevin Gordon at Charles Schwab. “No question it's in response to the fact that the prospect of rate cuts helps companies that have been struggling in the ‘higher for longer environment.'”

Sosnick at Interactive Brokers warns, though, that a prolonged selloff in some of the biggest names could pressure the main indices that investors watch — even if the majority of stocks remain initially unscathed.

“That in turn could cause investors to lighten their exposure to key index-based investments, such as ETFs like SPY and QQQ,” he said. “If that occurs, then the selling could swamp the index as a whole, hurting the now laggard value stocks nonetheless.”

Neuberger Berman Group's Steve Eisman expects the outsized strength in US megacap technology shares will “last for years,” as artificial intelligence becomes more accessible to consumers via electronic devices.

“You have to own the big, large-cap tech stocks,” he told Bloomberg Television in an interview on Thursday. Eisman's words attract notice on Wall Street because he made a name for himself with his “Big Short” bet against subprime mortgages ahead of the global financial crisis

While forecasts for the “Magnificent Seven” remain robust, their earnings are expected to slow in the second quarter — just as the rest of the S&P 500 may finally post their first year-on-year growth in at least five quarters, according to Bloomberg Intelligence strategists led by Gina Martin Adams.

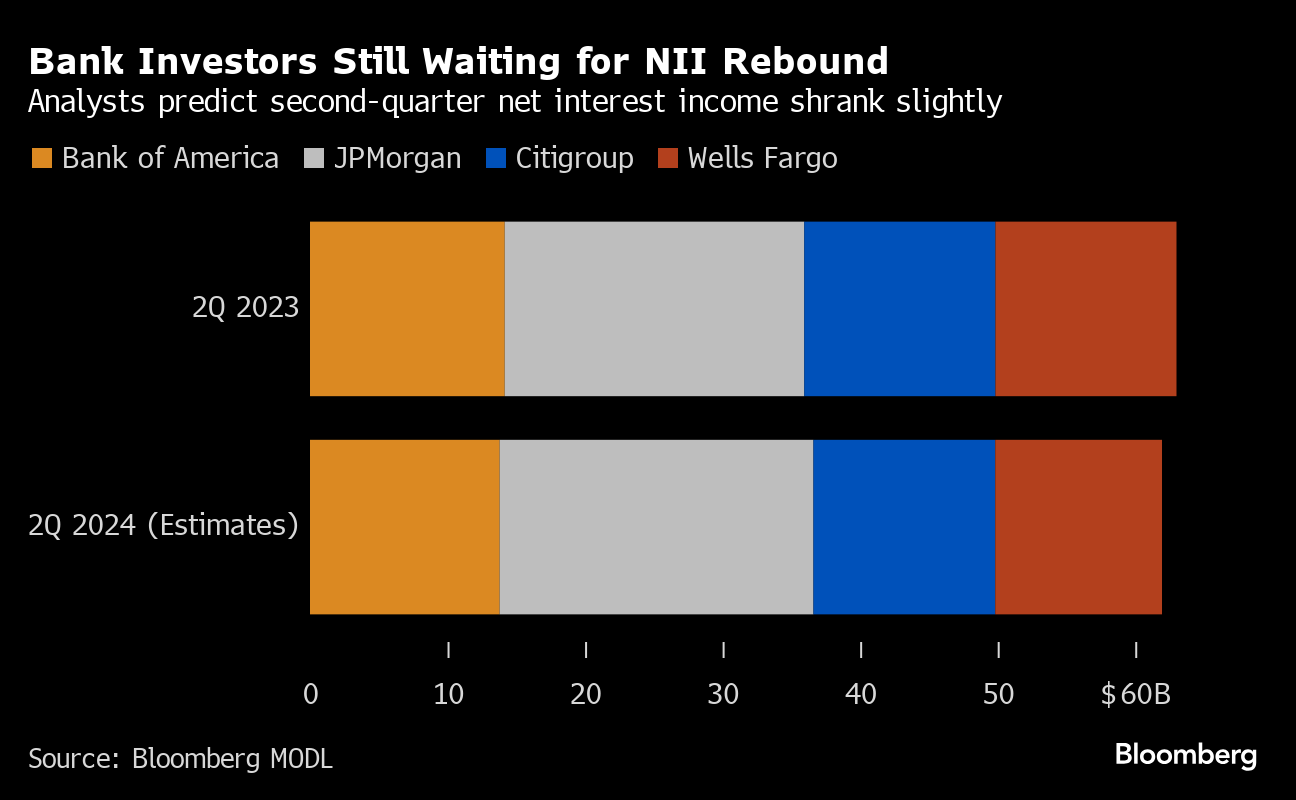

As the Wall Street banks kick off their second-quarter earnings announcements Friday, investors are looking past another projected drop in net interest income — a key source of revenue for the lenders. Instead, they're anticipating a rosy view on fee-generating businesses like investment banking and signals that at least some lenders see a rebound in loan profits.

JPMorgan Chase & Co., Wells Fargo & Co. and Citigroup Inc. start the earnings cycle Friday morning, followed by Goldman Sachs Group Inc. on Monday. Morgan Stanley and Bank of America Corp. report Tuesday.

Wall Street's Reaction to CPI:

- Michael Feroli at JPMorgan Chase & Co:

Sticky inflation is coming unglued. We now think this paves the way for a first cut in September (previously November), followed by quarterly cuts thereafter.

- Neil Dutta at Renaissance Macro Research:

The doves have what they need. It is time to cut.

- Richard Flynn at Charles Schwab UK:

This is the latest in a string of data releases that continues to set the stage for the Fed to cut interest rates this year, potentially as soon as September. We expect that this economic optimism will benefit markets.

- Peter Boockvar at The Boock Report:

Inflation continues to moderate. September cut is a lock I believe.

- Chris Low at FHN Financial:

The Fed will be very pleased with the June CPI report. In fact, inflation was so subdued, FOMC members may start to worry they have kept policy tight for too long.

- Bret Kenwell at eToro:

When combined with the recent weakness we've seen in the labor market, this likely has the Fed readying a rate cut. Some investors may be wondering if a July cut could be in the cards. While that may be too soon for the Fed, a September cut should be the base-case expectation.

- Lindsay Rosner at Goldman Sachs Asset Management:

One word: pivotal.

With three inflation prints between this morning and September's Fed meeting, today's print was crucial in helping the Fed gain confidence inflation is still moving in the right direction.

- Quincy Krosby at LPL Financial:

Cool CPI puts a September rate cut clearly in play.

For the market, clearly the preferred basis for easing rates is predicated on inflationary pressures cooling at a steady pace rather than on an economy losing momentum.

Corporate Highlights:

- The US Federal Trade Commission plans to delay its decision whether to block Chevron Corp.'s $53 billion takeover of Hess Corp. until after an arbitration case with Exxon Mobil Corp. is settled, according to people familiar with the matter.

- Bunge Global SA's $8 billion deal to acquire Glencore Plc-backed Viterra is facing the risk of delays as countries including Canada, China and the European Union are yet to approve the acquisition.

- Delta Air Lines Inc. warned that domestic carriers are struggling to fill planes in the all-important summer travel season, dragging down ticket prices in a fare war that's weighing on profits.

- Pfizer Inc. is moving forward with a weight-loss pill as it seeks to mount a comeback from its post-pandemic slump, but the drugmaker gave few clues about what exactly informed that decision.

- Apple Inc. has avoided the threat of fines from European Union regulators by agreeing to open up its mobile wallet technology to other providers free of charge for a decade.

- Dollar General Corp. agreed to a sweeping companywide settlement with US safety regulators, a potential turning point for the nation's most ubiquitous retailer after years of controversy about safety conditions in its stores.

Key events this week:

- China trade, Friday

- University of Michigan consumer sentiment, US PPI, Friday

- Citigroup, JPMorgan and Wells Fargo's earnings, Friday

Some of the main moves in markets:

Stocks

- The S&P 500 fell 0.9% as of 4 p.m. New York time

- The Nasdaq 100 fell 2.2%

- The Dow Jones Industrial Average was little changed

- The MSCI World Index fell 0.3%

Currencies

- The Bloomberg Dollar Spot Index fell 0.5%

- The euro rose 0.3% to $1.0864

- The British pound rose 0.5% to $1.2913

- The Japanese yen rose 1.8% to 158.83 per dollar

Cryptocurrencies

- Bitcoin was little changed at $57,364.12

- Ether rose 0.3% to $3,105.14

Bonds

- The yield on 10-year Treasuries fell seven basis points to 4.21%

- Germany's 10-year yield declined seven basis points to 2.46%

- Britain's 10-year yield declined five basis points to 4.07%

Commodities

- West Texas Intermediate crude rose 1.2% to $83.06 a barrel

- Spot gold rose 1.8% to $2,413.84 an ounce

This story was produced with the assistance of Bloomberg Automation.

--With assistance from Lu Wang, Sagarika Jaisinghani, Alexandra Semenova, Felice Maranz, Carly Wanna, Henry Ren and Bre Bradham.

More stories like this are available on bloomberg.com

©2024 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.