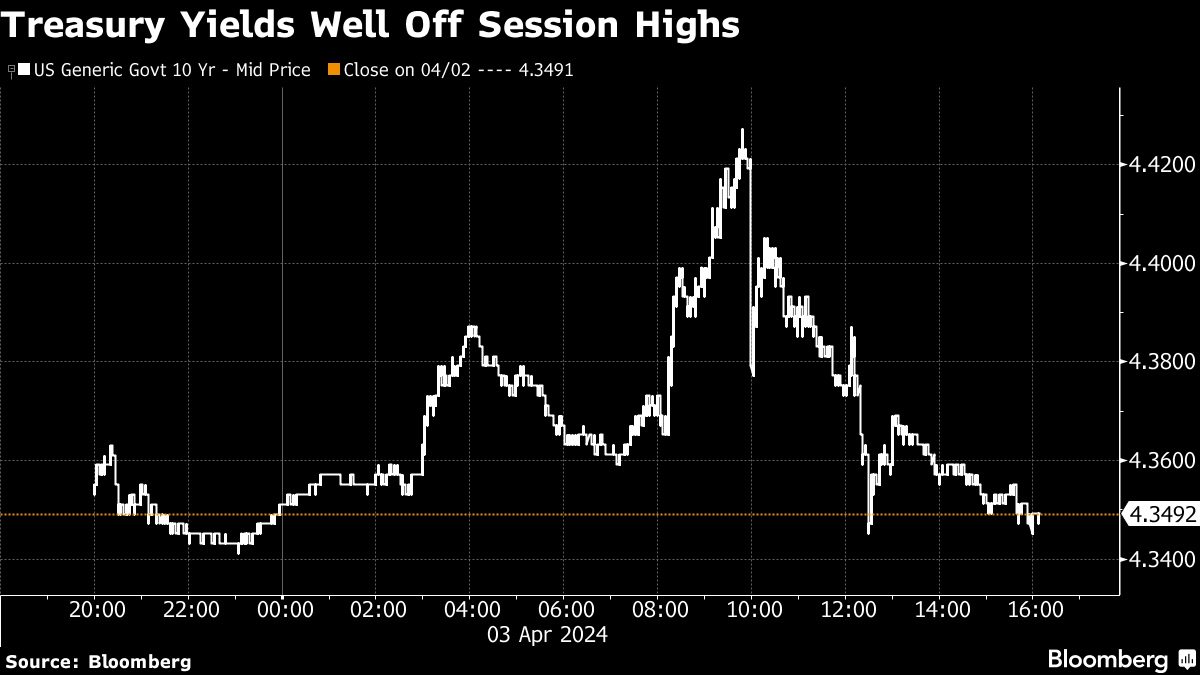

(Bloomberg) -- The bond market rebounded from session lows, with Jerome Powell only reiterating the Federal Reserve's wait-and-see approach before policymakers decide to embark on interest-rate cuts.

While the Fed chief didn't break any major new ground, Wall Street got some relief from his views that recent inflation figures did not “materially change” the overall picture. Powell also reaffirmed that it will likely be appropriate to begin lowering rates “at some point this year.” Equities edged up after a two-day slide, but struggled to pick up much traction amid a drop in a pair of blue chips — Intel Corp. and Walt Disney Co.

In recent days, traders had scaled back their rate-cut expectations amid signs of economic resilience and a more cautious tone from a drumbeat of Fed officials. That has led to skepticism on whether Powell and his colleagues would be able to deliver on the central bank's projection of three rate reductions this year.

“Powell says recent data has not materially changed the picture,” said Krishna Guha at Evercore. “We read this as confirming that the spasm of concern in markets that the economy might be too strong for the Fed to cut in June was overdone — and the base case remains June and three cuts this year.”

Treasury 10-year yields were little changed at 4.35% after climbing about eight basis points earlier Wednesday. The S&P 500 finished with a mere gain of 0.1%. Intel fell over 8% on a disappointing outlook for its factory operations. Disney dropped more than 3% as shareholders rejected dissident investor Nelson Peltz's bid for a board seat.

“The Fed is unquestionably in wait-and-see mode,” said Ian Lyngen and Vail Hartman at BMO Capital Markets. “All waiting and no seeing has been the hallmark of this cycle's first rate cut and nothing learned from today's session will change that.”

To Peter Williams at 22V Research, Powell seems to want to get some cuts done, but with growth and the labor market holding up, the spot incentive to do so is relatively minimal.

“Instead, the inflation data will have to give the Fed permission to start cuts,” Williams noted. “I continue to think that the odds they are able to cut in June are around or just a bit above 50%, but that cumulative cuts in 2024 lean more towards 2x than 3x at this point.”

The Fed could risk losing its credibility if it cuts rates too soon, according to Eric Veiel at T. Rowe Price Group Inc.

“Jerome Powell said very early on he is a student of what happened in the seventies,” he told Bloomberg Television — before Powell's remarks. “If they go ahead and start cutting now, I think they are in danger of making the same mistake.”

In the 1970s, the central bank was too quick off the mark in easing policy before inflation was truly vanquished. That's an error that Paul Volcker committed in 1980 as the economy weakened, only to reverse course later and drive the US into a deeper downturn.

Amid a backdrop of mixed data and a question on how long the Fed intends to pause, “expect some churning in the market,” says Victoria Fernandez at Crossmark Global Investments.

“We expect more of a market consolidation instead of a correction,” said Yung-Yu Ma at BMO Wealth Management. “The stock market doesn't need Fed rate cuts or even falling inflation, but it's also not in a robust position to quickly digest risks that could arise from accelerating inflation, increasing geopolitical shocks to oil prices, or rising long-term interest rates.”

Despite a “solid” outlook for a US soft landing, stock investors' expectations have gotten stretched. Morgan Stanley's wealth management arm says that's reason to seek opportunities outside the S&P 500, according to a note from the bank's global investment committee.

The US equity benchmark's rally was driven by multiples expansion, with investors expecting improving profits despite cooling growth, Morgan Stanley Wealth Management Chief Investment Officer Lisa Shalett wrote this week.

Investors appear to be showing “persistent” demand for US stocks, according to Citigroup Inc. strategists, suggesting there's room for the rally to resume after the recent pullback.

More than $16 billion in net long positions was added to S&P 500 futures last week, while exchange-traded funds showed net inflows, strategists led by Chris Montagu wrote this week.

Corporate Highlights:

- Apple Inc. has teams investigating a push into personal robotics, a field with the potential to become one of the company's ever-shifting “next big things,” according to people familiar with the situation.

- Ulta Beauty Inc. sank after executives signaled cooling consumer demand for beauty products, which weighed on the shares of industry peers as well.

- Ford Motor Co.'s US auto sales rose 7% in the first quarter on strong demand for gas-electric hybrids, despite a laborious launch of a redesigned F-150 pickup truck.

- Cal-Maine Foods Inc. reported earnings per share and net sales that topped consensus expectations. It touted strong demand for eggs, noting that total sales volumes, or dozens sold, hit a company record.

- Eli Lilly & Co.'s weight-loss drug Zepbound is officially in shortage in the US, after mounting complaints by patients, doctors and pharmacists who are having trouble finding the drug.

- Dave Calhoun, who plans to step down as chief executive officer of beleaguered Boeing Co. later this year, will also depart from the board of machinery manufacturer Caterpillar Inc.

- Mastercard Inc. plans to increase certain credit card fees beginning April 15, just days after the company and Visa Inc. trumpeted a $30 billion settlement over separate swipe fees designed to provide relief to retail businesses.

- Spotify Technology SA plans to raise the price of its popular audio service in several key markets for the second time in a year, a crucial step toward reaching long-term profitability.

Key events this week:

- Eurozone S&P Global Services PMI, PPI, Thursday

- US initial jobless claims, Challenger job cuts, Thursday

- Fed's Loretta Mester, Alberto Musalem, Thomas Barkin, Patrick Harker, Austan Goolsbee speak, Thursday

- European Central Bank publishes account of March rate decision, Thursday

- Eurozone retail sales, Friday

- US unemployment, nonfarm payrolls, Friday

- Fed's Michelle Bowman, Thomas Barkin and Lorie Logan speak, Friday

Some of the main moves in markets:

Stocks

- The S&P 500 rose 0.1% as of 4 p.m. New York time

- The Nasdaq 100 rose 0.2%

- The Dow Jones Industrial Average fell 0.1%

- The MSCI World index rose 0.1%

Currencies

- The Bloomberg Dollar Spot Index fell 0.3%

- The euro rose 0.6% to $1.0833

- The British pound rose 0.6% to $1.2649

- The Japanese yen was little changed at 151.68 per dollar

Cryptocurrencies

- Bitcoin rose 0.2% to $65,856.04

- Ether rose 1.3% to $3,315.95

Bonds

- The yield on 10-year Treasuries was little changed at 4.35%

- Germany's 10-year yield was little changed at 2.40%

- Britain's 10-year yield declined three basis points to 4.06%

Commodities

- West Texas Intermediate crude rose 0.5% to $85.57 a barrel

- Spot gold rose 0.7% to $2,297.60 an ounce

This story was produced with the assistance of Bloomberg Automation.

--With assistance from Farah Elbahrawy and Rheaa Rao.

More stories like this are available on bloomberg.com

©2024 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.