SBI Life Insurance Co.'s growth trajectory looks predictable, brokerages said, after the company posted strong earnings for the third quarter of fiscal 2025.

Motilal Oswal Financial Services has given a buy rating for the insurance company's stock, whereas Emkay Global has upgraded its incumbent rating to buy, in view of the favourable valuations and improved growth visibility.

SBI Life Insurance posted healthy margin growth for value of new businesses in three months to December, which was driven by non-par and protection products. Also, a rise in preference for pure term plans compared to return on premium products resulted in lower retail protection growth, albeit better margin.

Emkay Global has raised the target price for the firm's stock to Rs 1,850 from Rs 1,750 apiece.

Motilal Oswal expects SBI Life Insurance to deliver 15% and 14% compounded annual growth rate in the annual premium equivalent and value of new business, respectively, over the period of fiscal 2024 to fiscal 2027.

Motilal Oswal expects that momentum in APE collection will continue. However, risks from interest rates may remain.

SBI Life Q3 Results (Consolidated, YoY)

Net profit up 71.2% at Rs 551 crore versus Rs 322 crore. (Estimate Rs 436 crore)

Net premium income up 11.3% at Rs 24,828 crore versus Rs 22,317 crore.

APE up 13% Rs 6940 crore vs Rs 6130 crore

VNB up 11% Rs 1870 crore vs Rs 1680 crore

VNB Margin at 26.95% from 26.9% (QoQ)

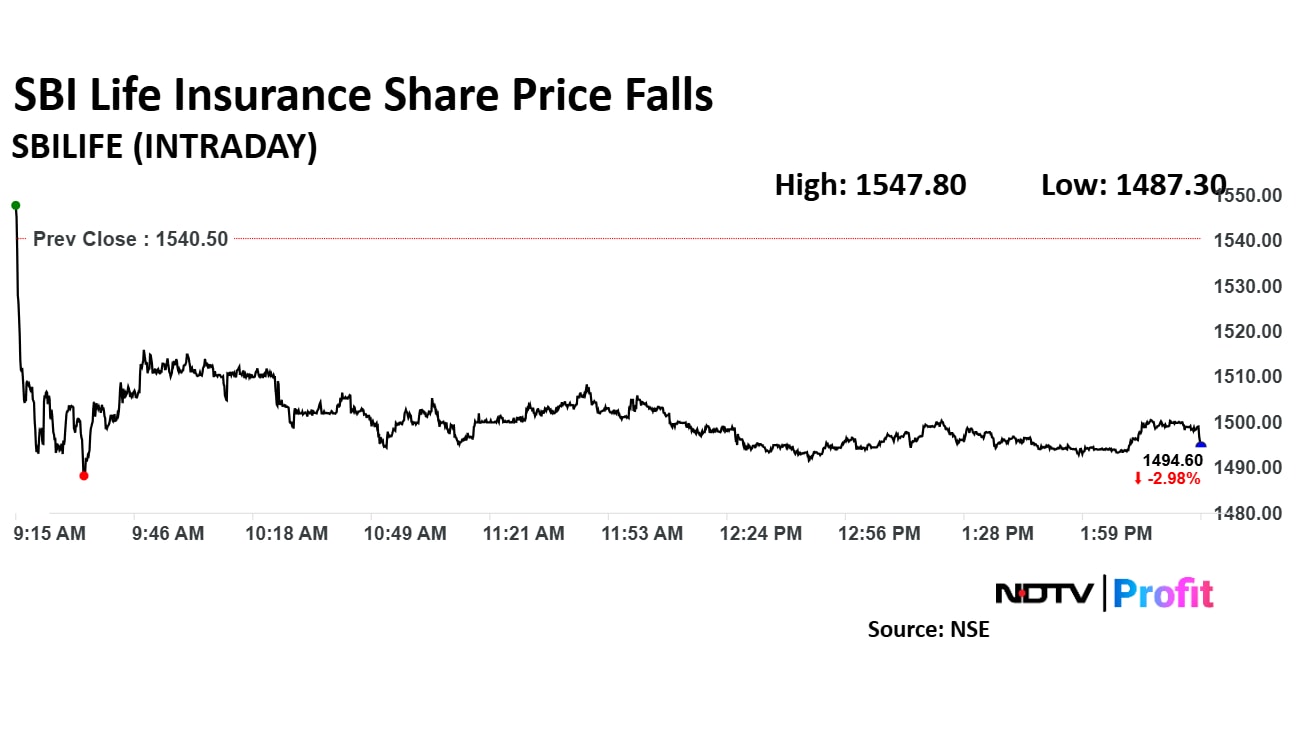

Shares of SBI Life Insurance declined to a low of Rs 1,487.30 apiece, down 3.45% during the day's trade. The scrip recovered to marginally to trade 2.69% lower at Rs 1,499.10 on the NSE as of 2:22 p.m., as compared to 0.66% advance in the benchmark Nifty 50.

The company's stock has gained by 3.95% in 12 months. The total traded volume so far in the day stood at 2.8 times its 30-day average. The relative strength index was at 49.39.

Out of 39 analysts tracking the company, 33 maintain a 'buy' rating, four recommend a 'hold', and two suggest 'sell', according to Bloomberg data. The average of 12-month consensus price target implies a potential upside of 27%.

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.