At a recent investors meet, the management of Pidilite Industries Ltd. conveyed their ambition to improve the underlying volume growth to double digits. They also expressed their focus remained on overall growth rather than margin expansion.

However, these goals and intents were not sufficient for brokerages to upgrade the rating of Pidilite Industries, due to unstable near-term demand outlook. The brokerages maintained ratings that suggest either trimming the stock from the portfolio or waiting to sell.

Jefferies maintains a 'hold' rating on Pidilite Industries. Macquarie has an 'underperform' rating, while Citi Research maintains 'sell' rating.

The reason behind near-term unstable demand outlook is the uncertainty over recovery of urban demand. Geopolitical factors will weigh on international demand, Jefferies indicated. It estimates over 13% Ebitda and 16% net profit growth for the period between financial years 2024 and 2027. Volume growth from construction, furnishings, new product launches, and premiumisation is expected to drive growth.

Jefferies revised the target price to Rs 3,040 apiece from Rs 3,200, which implied a 11.38% upside from Tuesday's closing price.

Macquarie gave a thumbs-up to Pidilite Industries' perspective on its distribution and supply-chain strength and growth opportunities for various categories. They also liked the management's focus on innovation for 'core' brands, for which Pidilite Industries has a leadership position in the market. However, the brokerage found fault with the management's lack of tangible targets for its growth and profitability.

Pidilite Industries did not share any near-term or medium-term growth and profitability targets. The management's guidance was on growing sales ahead of GDP for the medium term, Macquarie said. The brokerage maintained 'underperform' rating with Rs 2,600 target price, which implied a 4.7% downside from Tuesday's closing price.

Pidilite is aiming to become an emerging player in the international market. It is likely to implement the same strategy as it has in India, Citi Research said. Its entry in the Europe market will depend on any purposeful merger and acquisition. Citi Research has a target price of Rs 2,800, which implied a 2.6% upside.

Decline in housing and home improvement, and excess volatility in raw material prices will be key negatives for Pidilite Industries, Jefferies said.

Pidilite Industries Share Price

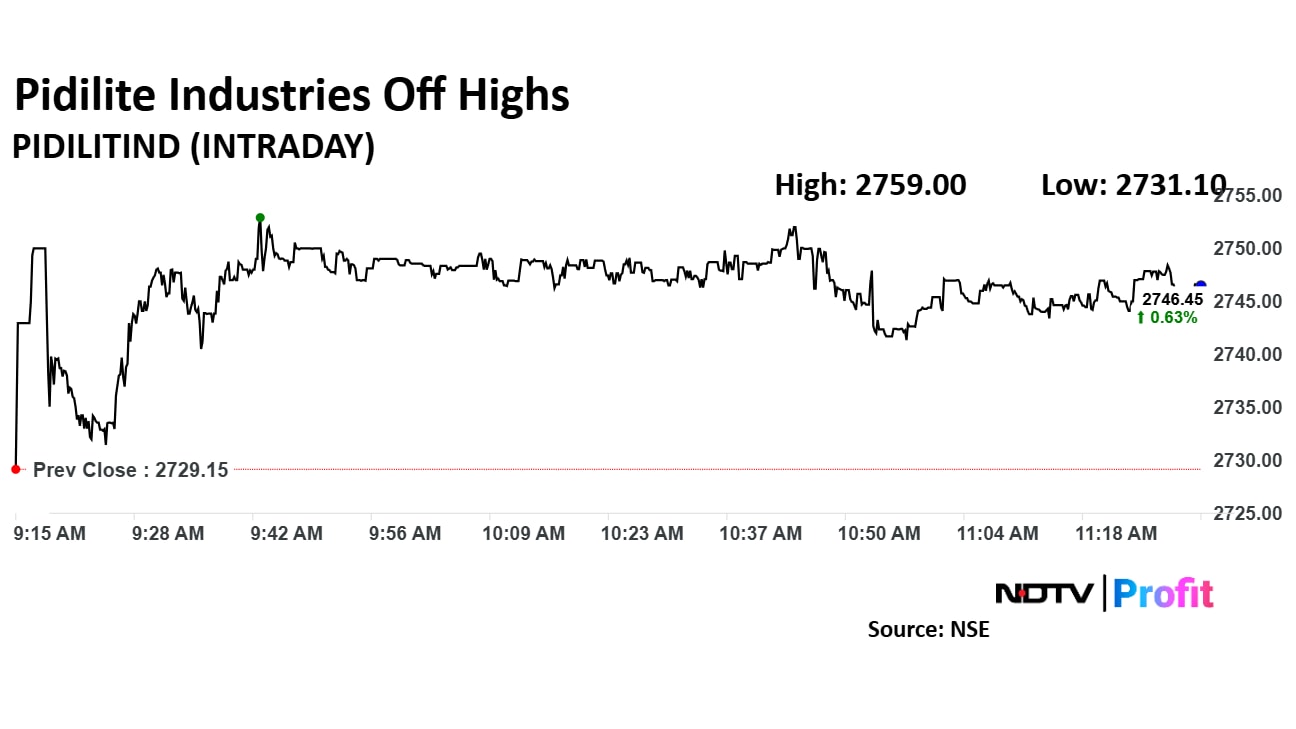

Pidilite Industries' share price rose 1.09% to Rs 2,759 apiece. It pared gains to trade 0.68% higher at Rs 2,747.80 apiece as of 11:27 a.m., as compared to a 0.24% advance in the NSE Nifty 50.

The stock declined 4.97% in 12 months, and 5.39% on year-to-date basis. Relative strength index was at 47.00.

Out of 17 analysts tracking the company, 10 maintain a 'buy' rating, two recommend a 'hold' and five suggest 'sell', according to Bloomberg data. The average 12-month analysts' consensus price target implies an upside of 15.4%.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.