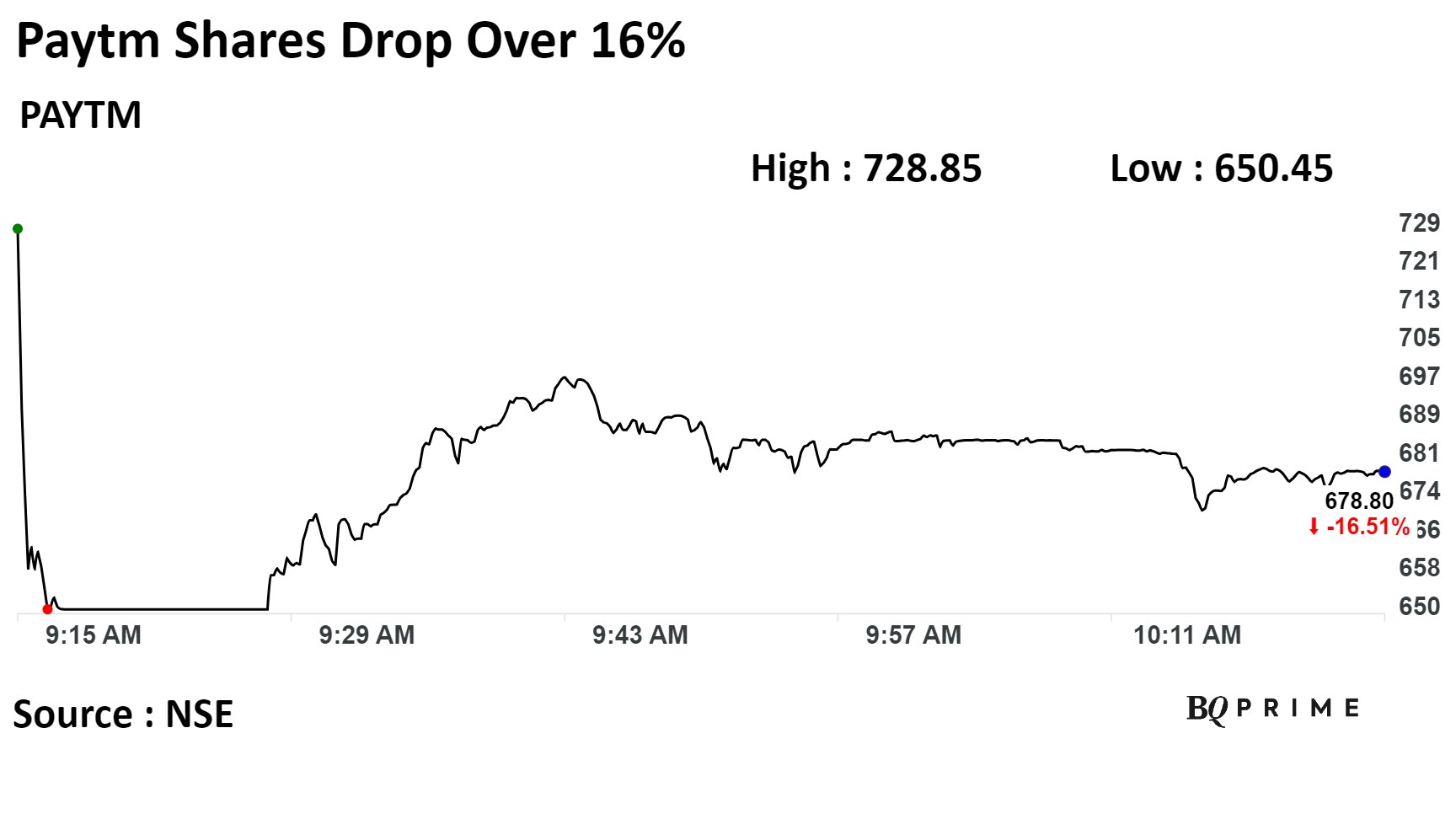

Shares of Paytm parent One97 Communications Ltd. tumbled to hit the 20% lower circuit after analysts downgraded the stock as the company decided to bring down the level of unsecured loans under Rs 50,000 in a calibrated manner.

"Postpaid loans is a portfolio which is predominantly under Rs 50,000. On the back of the macro developments and regulatory guidance, which is there, we have decided to—in a calibrated manner—keep scaling the Rs 50,000 portfolio, especially the Postpaid loan, down," Bhavesh Gupta, president and chief operating officer of Paytm, said in a conference call on Wednesday.

JPMorgan called it a "profit warning", highlighting a sharp moderation in its ticket loan distribution following the system-level concern from the regulators and lending partners.

The company is indicating a 40–50% drop in low-ticket lending as it had intensified bottom scaping of customers with lower limits, with rising system-level concerns around low-ticket unsecured lending, the research firm said in a note. "We assume a sustained slowdown in BNPL and even PL over FY24/25, and do not give credit on offsets via pick-up in Merchants loans/high tickets loans or any flexibility that Paytm may have on direct costs."

Paytm's move comes after the Reserve Bank of India tightened norms for unsecured retail loans in November.

The central bank made consumer lending costlier for banks and non-bank lenders, and also asked them to limit exposure to such loans, amid growing risk concerns.

What Analyst Have to Say

JPMorgan

The research firm downgraded Paytm to 'neutral' from ' overweight' on the back of rising concern around unsecured credit likely slowing down revenue/Ebitda.

It reduced target price from Rs 1,200 to Rs 900, implying a downside of 10.70%

JPMorgan cut FY24–26 revenue and adjusted Ebitda estimates by 4–9% and 7–34% respectively, driven by slower lending growth rate.

The research firm remains cautious on building success in high-ticket loans or ability to rationalise indirect costs to limit the impact on profits.

Slowdown seems pre-emptive in nature as Paytm has not witnessed a deterioration in portfolio quality or rise in bounce rates.

"We think if Paytm is able to manage the asset quality over the next 2-4Q in the BNPL segment, investors would draw comfort from the quality of portfolio underwriting."

This segment is likely to be more competitive given the wider presence of banks and NBFCs that could pressure PL take rates.

Jefferies

Jefferies has retained a 'buy' on Paytm with target price of Rs 1,050, implying an upside return potential of 29%.

Paytm announced its decision to halve its BNPL disbursals over the course of next 3-4 months. "We believe this reflects growing conservatism in the system, as well as Paytm's large share in the segments."

The brokerage expect some moderation in loan disbursals following RBI measures. The quantum is ahead of Jefferies estimates. "Compared to our earlier estimate of overall loan disbursal growth of 98%/49%/43% in FY24/25/26E, we now expect 65%/5%/27%, respectively".

Paytm announced plans to expand into higher-ticket personal and merchant loans, which would be targeted at lower risk and prime/near-prime customers, in partnership with large banks and NBFCs.

Motilal Oswal Financial Services

The research firm has a 'buy' rating with a target price of Rs 1,025, implying an upside of 26%.

Paytm's strategy to move away from small -ticket-size BNPL loans will affect the total loan originations via the platform as the segment forms over 50% of total disbursements.

The company indicated the monthly postpaid loan sourcing run rate to moderate by 50% from Rs 30 billion to Rs 15 billion. As a result, the total disbursement run rate is expected to decline to around Rs 45 billion per month from about Rs 60 billion per month.

Take rates are expected to be marginally affected as BNPL as a product has lower take rates. However, a pick-up in higher-ticket personal loans should offset the overall impact. While the longevity of these measures and the outlook in low-ticket unsecured loans remains under watch.

Trimmed FY24/FY25 disbursement estimates by 15%-18%, reflecting the current developments.

Paytm has denied recent speculation that the company is losing out on lending partners. It currently has seven NBFC partners for loan distribution, while it is in process of integrating one large bank and two large NBFCs by March 2024 and June 2024.

Paytm mentioned that the scale-down in postpaid business is primarily prudential in nature and is to preempt any asset quality issues in coming quarters.

Asset-quality metrics remain steady and the pickup in high-ticket personal loans and merchant loans, along with the increase in the number of lending partners, should support steady growth in the medium term.

Morgan Stanley

Morgan Stanley has maintained 'equal-weight' rating on the stock with a target price of Rs 830 per share.

Asset quality trends for Paytm remain strong and unchanged. The partnership for postpaid lending business is still in place and high/ticket cohorts will continue to get credit.

Disbursement run-rate will drop in the near term, but Paytm's management expects limited earnings impact, as higher-ticket loans and other financial businesses scale up.

Paytm hit a lower circuit of 20% during an early trade. The stock was trading 16.60% lower at Rs 678 apiece, compared to a 0.37% decline in the NSE Nifty 50 as of 10:22 am. It has risen 27.55% year-to-date.

Total traded volume so far in the day stood at 17 times its 30-day average. The relative strength index was at 18, indicating the stock may be oversold.

Ten out of the 15 analysts tracking the company have a 'buy' rating on the stock, while five recommend 'hold', according to Bloomberg data. The average of 12-month analyst price targets implies a potential upside of 24%.

Essential Business Intelligence, Sharp Market Insights, Practical Personal Finance Advice, Daily Fuel, Gold and Silver Prices and Latest Stories — On NDTV Profit.