Shares of One 97 Communications Ltd., the parent of Paytm, hit fresh record lows on Tuesday after Macquarie Equity Research slashed its target price by 58% and downgraded it to 'underperform'.

Macquarie has cut the target price to Rs 275 per share from Rs 650 apiece earlier due to a sharp reduction in revenues across various segments. It has also cut revenues sharply as it reduced both payments and distribution business revenues.

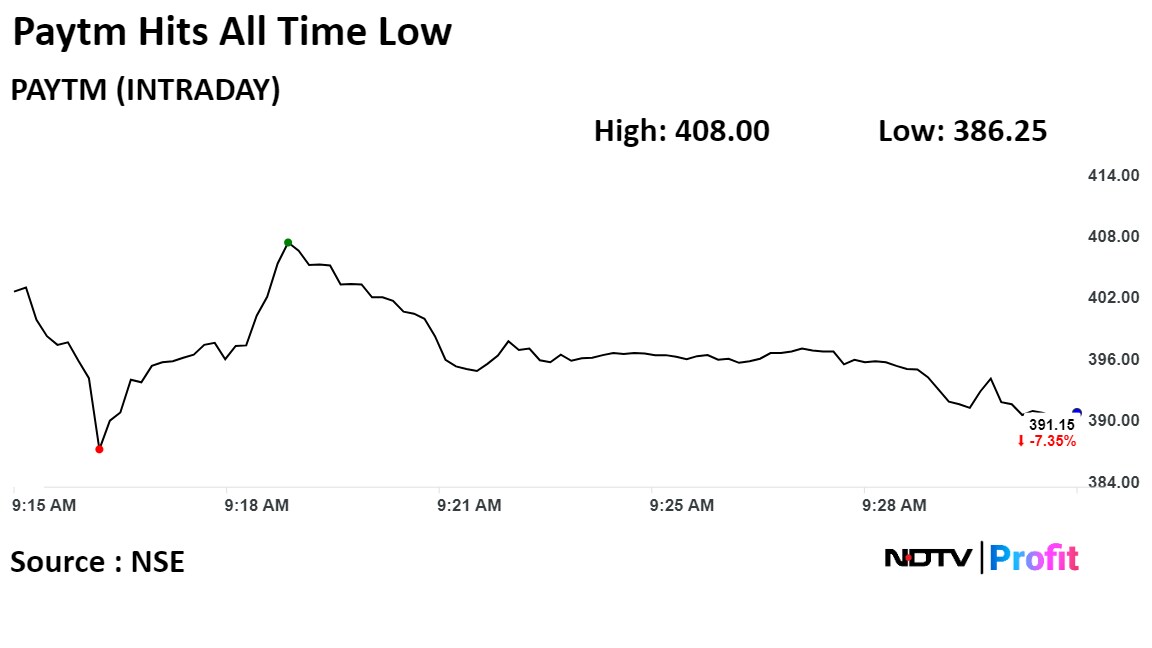

Shares of the company fell as much as 8.51% to Rs 386.25 apiece, hitting an all-time low. The stock last hit an all-time high on Feb. 6. It pared losses to trade 6.05% lower at Rs 396.65 apiece as of 9:27 a.m. This compares to a 0.10% decline in the NSE Nifty 50 Index.

It has fallen by 81.55% in the past 12 months. Total traded volume so far in the day stood at 0.3 times its 30-day average. The relative strength index was at 24, indicating it was underbought.

Out of 15 analysts tracking the company, six maintain a 'buy' rating, three recommend a 'hold', and six suggest a 'sell', according to Bloomberg data. The average 12-month consensus price target implies a downside of 38.4%.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.