All across FY23 and more so in the second quarter results, we are seeing increasing commentary and evidence of a K-shaped recovery in the great Indian consumption story. In fact, one can argue that the K is more pronounced than ever in India.

A recent note from DSP Mutual Fund points out that a monthly salary of Rs 25,000 in 2019-2020 puts the earner in the top 10% of the Indian population, and so the "per capita potential" numbers must be taken with a pinch of salt. Nothing brings out that dichotomy more than the pattern of consumption in post-pandemic India, as highlighted by the results and the commentary of the listed consumption sector players.

These trends take time to change, and while there has been a nascent recovery in the badly hit fast-moving consumer goods space, the K-shaped narrative still holds. Granted, a consumer confidence survey by Jefferies in Asia showed that 80% of respondents in India feel more confident regarding their finances, but I would reckon they have spoken to the urban consumer at large in India. Going by the feedback of Indian companies, the rural guy is still hurting.

Dichotomy Between Urban And Rural Consumption

Here are the plain facts. Overall performance in the quarter was largely value-driven as volumes remained subdued, with a clear dichotomy between urban and rural consumption patterns. Rural was not only weak, but there are no clear signs of recovery over the next few months, judging from the commentary in the quarter. One can argue that an odd Parle or Britannia has spoken of the strength of the rural consumer, but that might be a difficult case to build for the space at large.

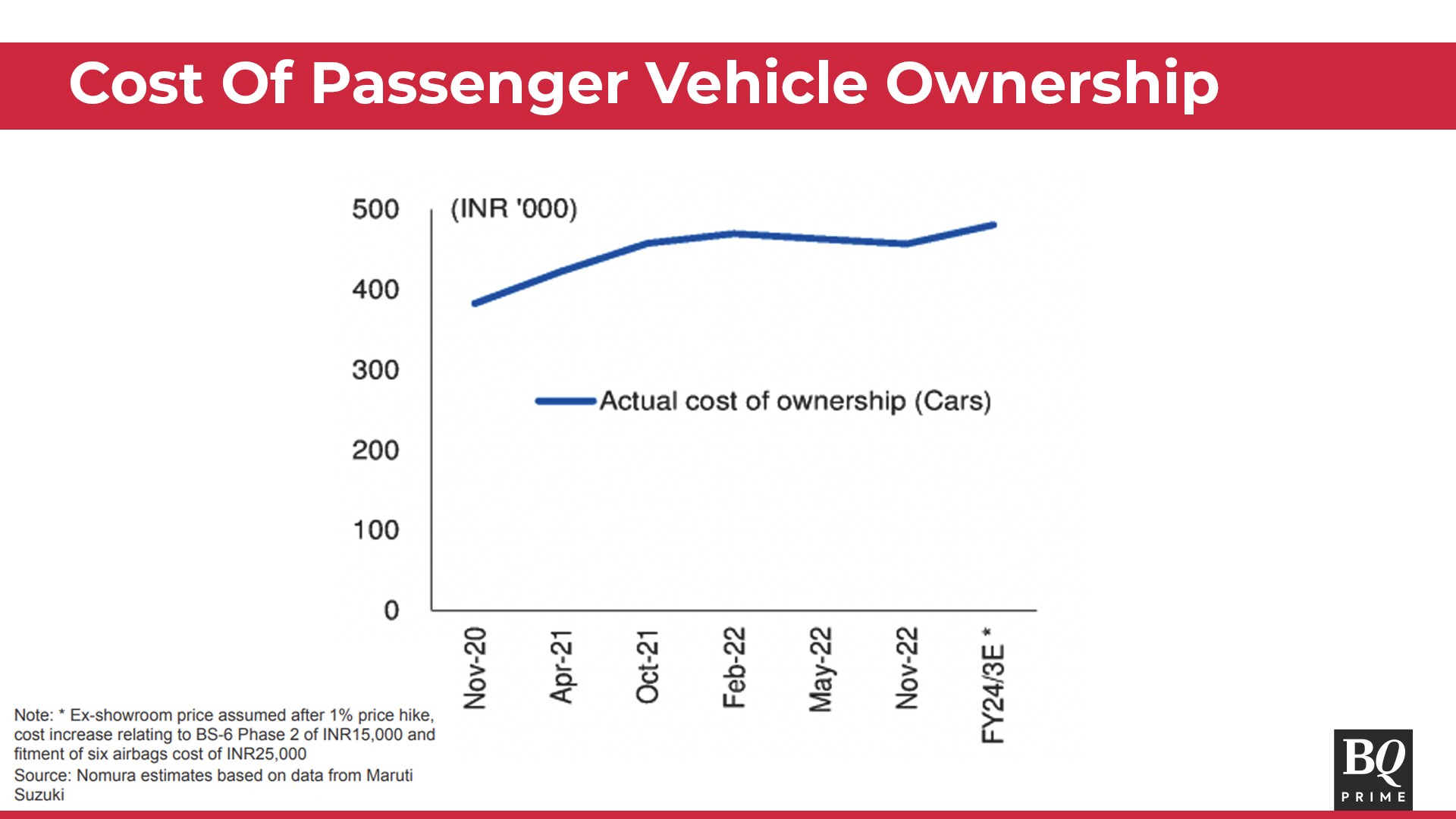

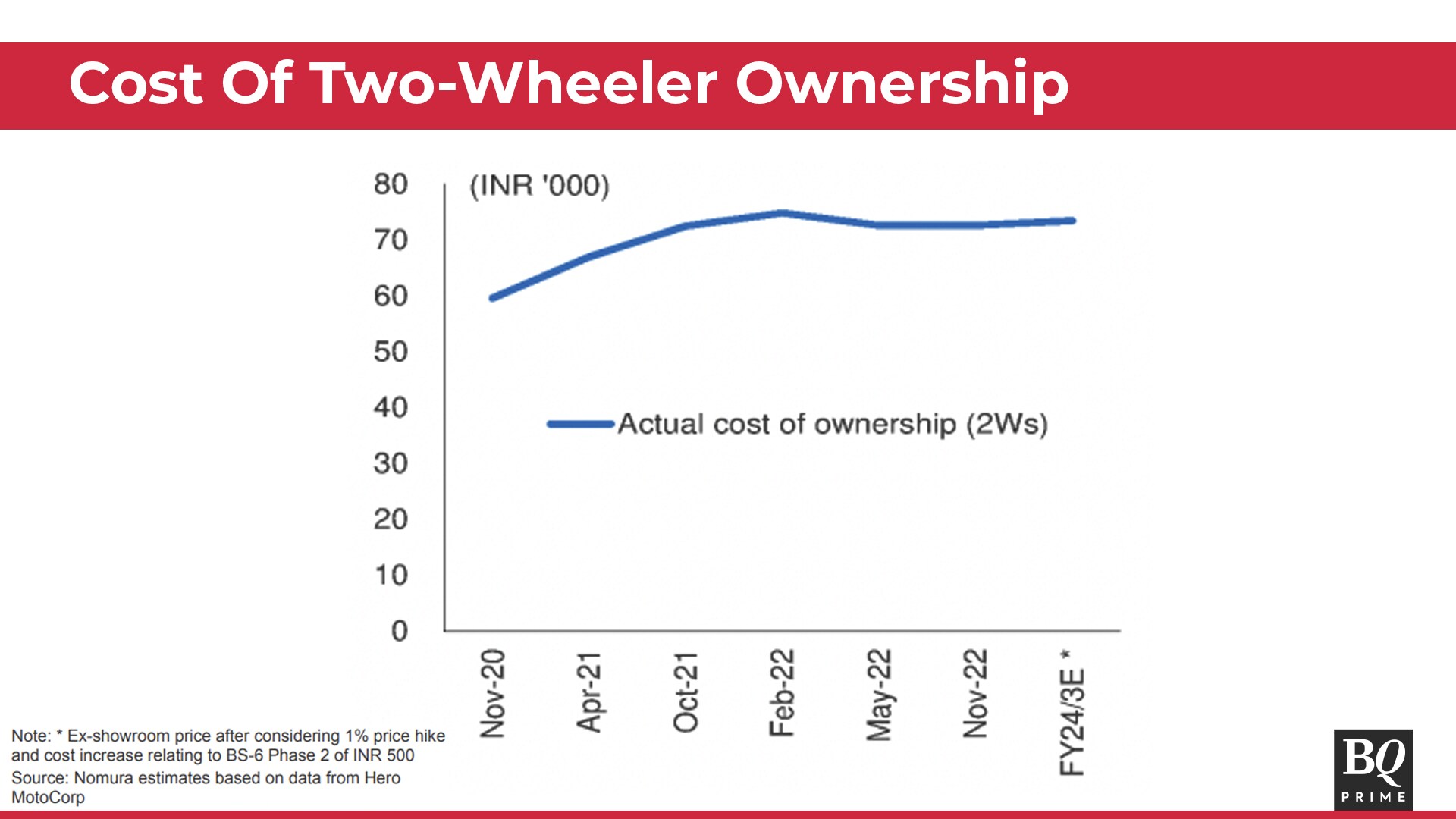

Even in auto, the belief is similar. A recent note by Nomura points out that the cost of ownership of cars and two-wheelers has gone up by around 19% and 22%, respectively, over the past two years--between November 2020 and November 2022, led by rising fuel and vehicle prices. Analysts believe that the cost of ownership is likely to go up further 5% and 1% in FY24, which prompts them to remain concerned about the mass consumption of entry-level cars and two-wheelers.

The dichotomy in the commentary was unmissable and brought out the K-shaped nature of the recovery. If Bata, with revenue growth of 35% tear-on-year, said the traction on the premium side is extremely high, Relaxo, with a revenue decline of 6%, spoke about the impact on affordability in the mass segment, which impacted them.

HUL reported 16% growth in sales, but mentioned in its call that it is quite natural for consumers, especially those in lower income levels, to feel the pinch of increased pressure on their wallets. On the other hand, Titan, which showed double-digit growth across most segments in Q2, spoke about how growth in the higher segment was coming more easily.

Simply put, most rural-focused companies showed signs of stress, and most urban-focused companies showed some glimpses of promise. This was also reflected in the order books of Samvardhana Motherson, which showed promise as they sold to the top-tier car manufacturers; or Westlife, which caters to the urban discretionary sector and has shown a promise of 16–18% compounded annual growth rate for the next five years in its Vision 2027 statement. On the contrary, V-Guard stated that there is stress on demand in small towns, rural markets, and entry-level products.

The demand gap is not the only thing that is hurting companies. While commodity costs have shown signs of stabilisation, many of them still remain high. Gross margin pressure, which was higher than expected in the second quarter of the current fiscal, may likely continue due to the high-cost inventory, which will only ease out after the current quarter for most companies. One can also argue that this is not a new phenomenon.

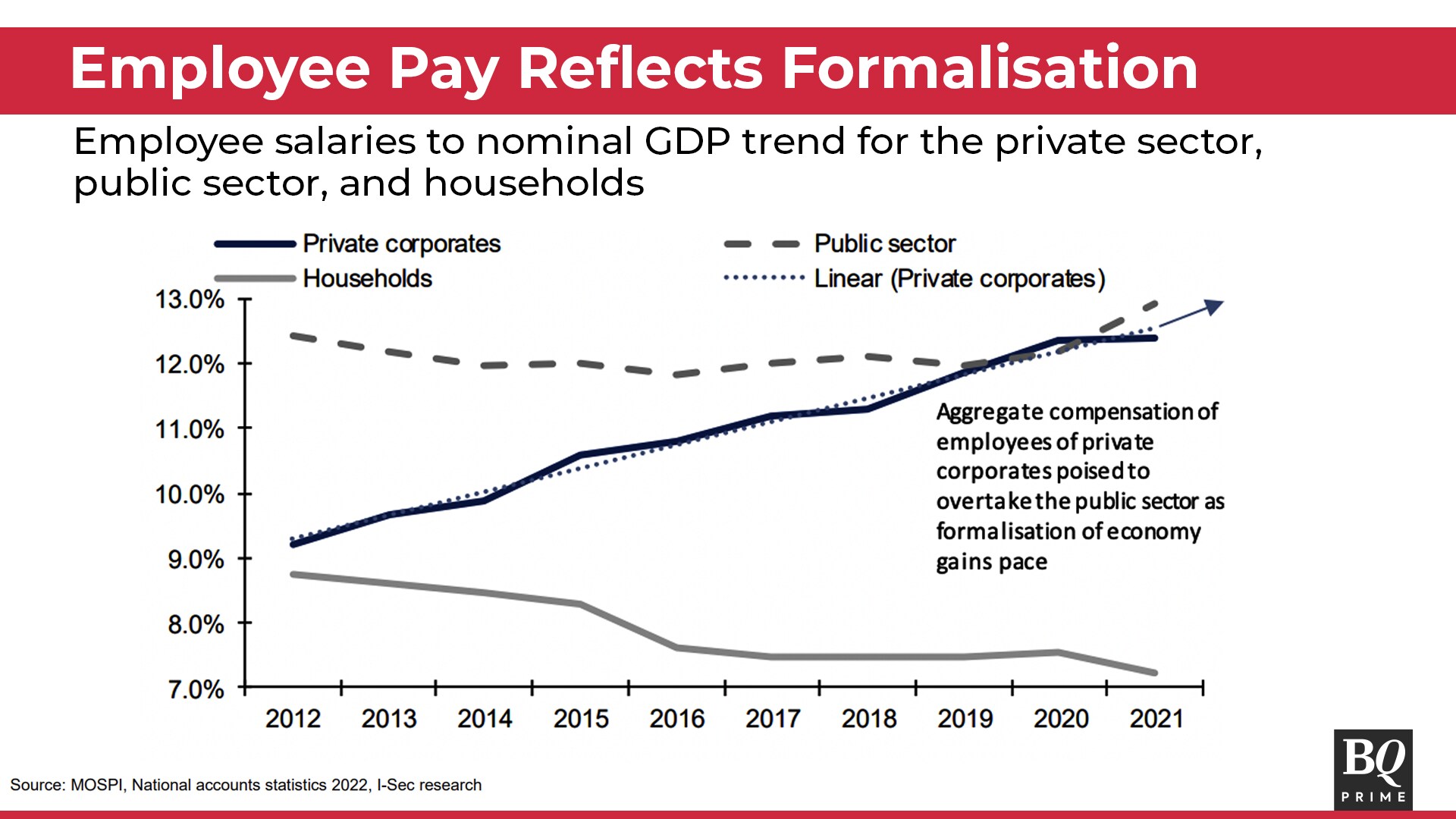

Compensation Of Employees To GDP Ratio

In a May note, ICICI Securities Strategists Vinod Karki and Niraj Karnani point out that the compensation of employees to GDP ratio for the private sector rose rapidly from 9.2% in FY12 to 12.4% in FY21. This effectively means that the share of the formalised, higher discretionary spending has risen in the period.

As a result, the analysts advocate that faster-than-nominal GDP expansion of compensation for the private corporate sector employees is a clear sign of formalisation of the economy and improving productivity, which, along with the significantly high per capita income of this segment, is positive for the gross savings rate and discretionary consumption within this segment.

What can change this? Well, for one, the government's support for the rural space is consistent, and therefore, if the economy were to turn, then the sustenance pattern may quickly turn into something more, which may have a very large impact on sales of FMCG, two-wheeler companies, and other companies.

If indeed the capex cycle sees a revival, and if the global beeline for manufacturing in India picks up steam, one can hypothesise that the rural and small-town consumption patterns may change. Yes, once again, it will depend on the economy. For now, though, the K stands tall, and investment decisions should be made accordingly.

If formalisation means discretionary spends will stay higher for the decade, then it may well mean that the expensive discretionary names will do much better than betting on the relatively cheaper bottom of the pyramid dependent names.

Niraj Shah is an Executive Editor at BQ Prime.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.