- Asian stocks showed mixed performance after the S&P 500 hit a record on Fed rate cut hopes

- US payrolls to be revised down by a record 911,000, signalling economic slowdown

- Money markets expect three Federal Reserve rate cuts this year amid inflation data

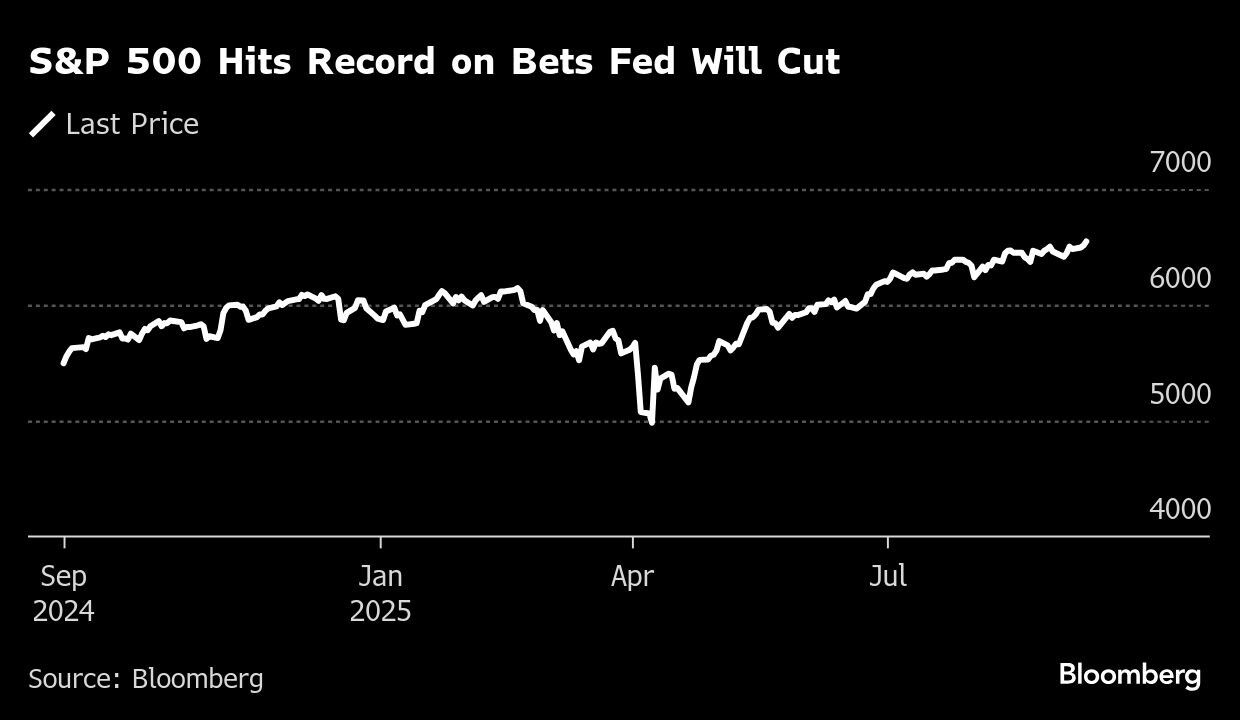

Wall Street traders drove stocks higher and bond yields lower as an unexpected decline in inflation reinforced bets the Federal Reserve will resume cutting interest rates in September.

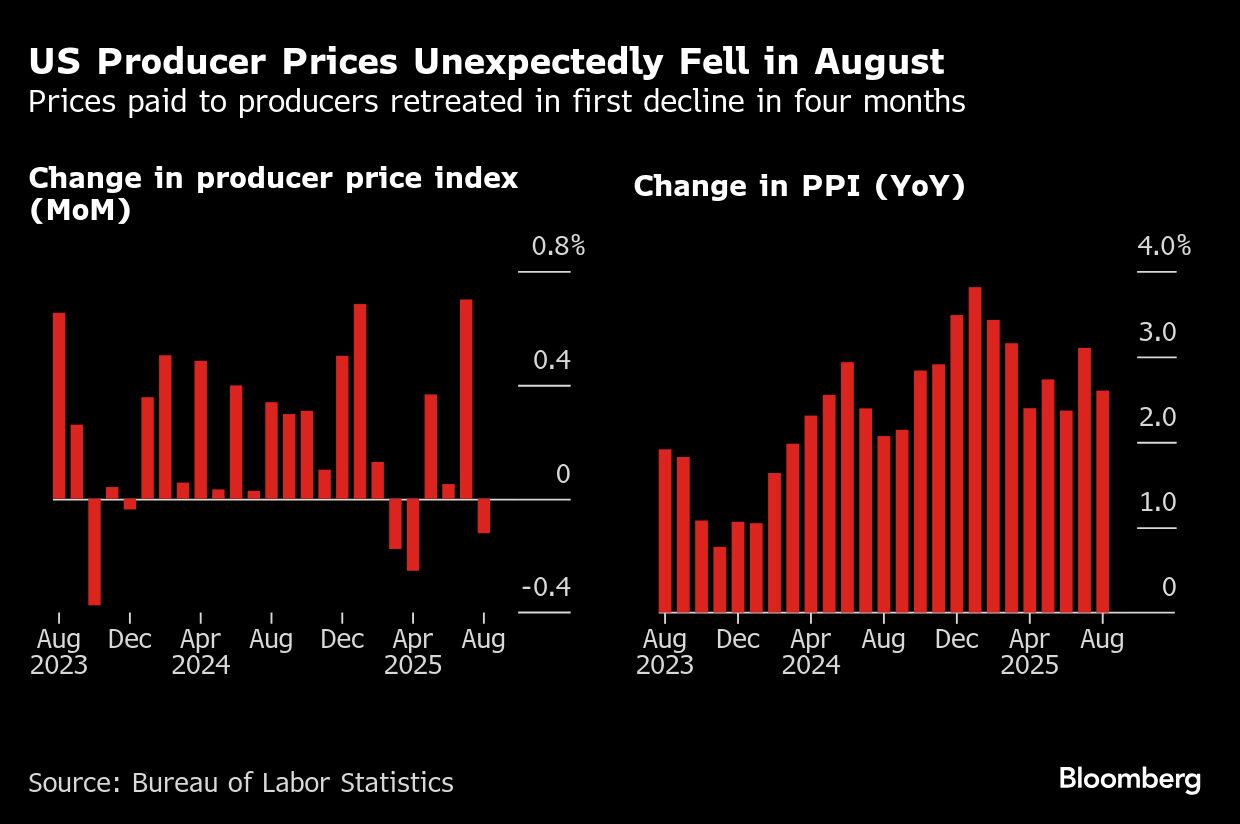

Just a week ahead of the Fed decision, the first drop in producer prices in four months soothed worries that elevated inflation would create a challenge for policymakers trying prevent a jobs downturn. The market reaction was sharp, and traders almost fully priced in three rate reductions in 2025.

The S&P 500 hit all-time highs, with tech leading the way. Oracle Corp. soared 40% on a solid cloud outlook and was set to vault past firms like JPMorgan Chase & Co. to become the 10th most-valuable member in the benchmark. Two-year yields fell three basis points to 3.53%. The dollar slid.

The producer price index decreased 0.1% in August from a month earlier and July's figure was revised down. From the year before, it rose 2.6%. Economists pay close attention to PPI as some components are used to calculate the Fed's preferred measure of inflation. President Donald Trump called for the Fed to make a “big” rate cut after the data.

“The worst-case scenario on inflation isn't playing out,” said David Russell at TradeStation. “The doves will be happy to see the year-over-year number back below 3%. Combined with the weak jobs data recently, this keeps us on track for rate cuts. However the speed and intensity might depend more on the big consumer index tomorrow.”

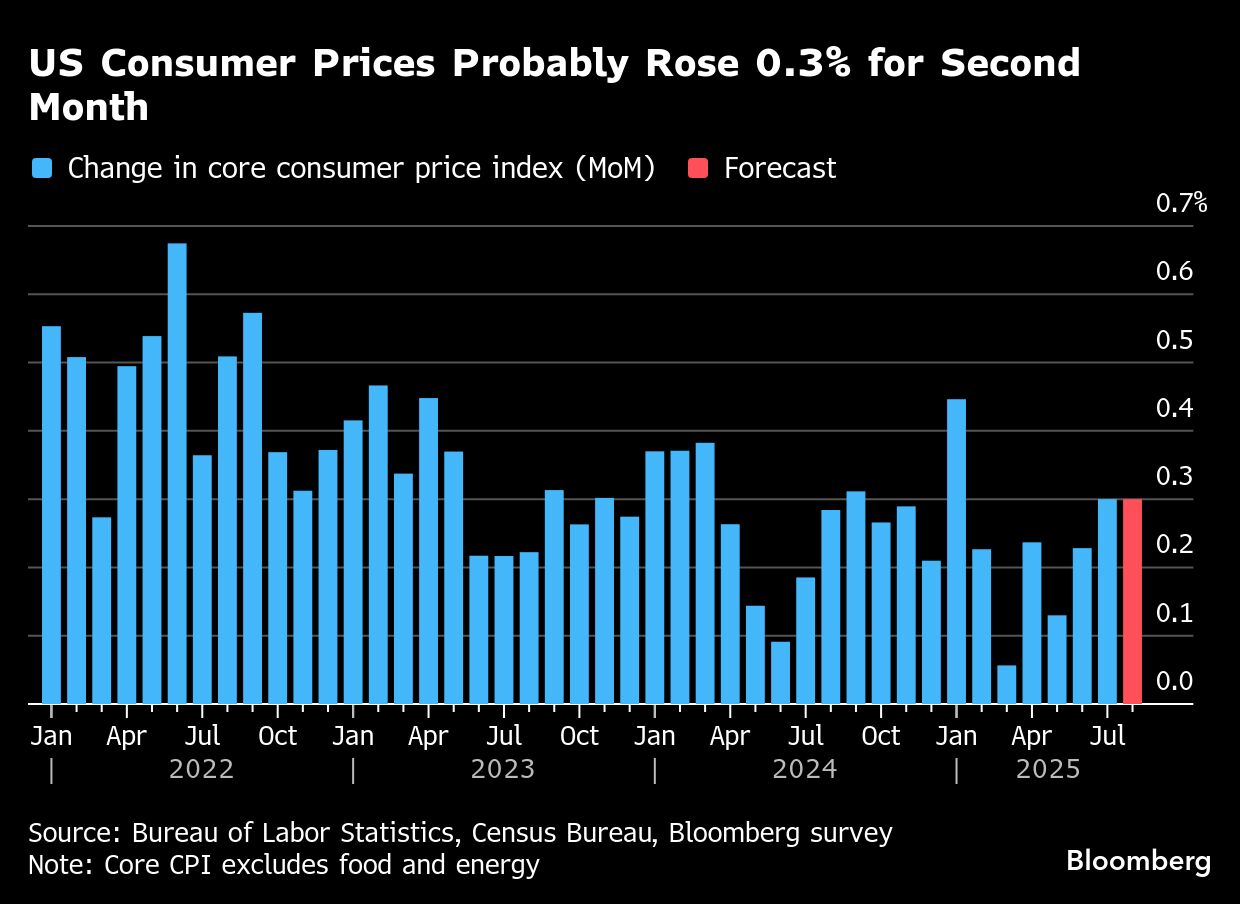

The extent to which companies pass the burden from tariffs on to consumers will be key in shaping the path for interest rates. In fact, attention will soon shift to consumer price data due Thursday. Forecasters expect another elevated advance in the core measure, which excludes food and energy.

“Tomorrow's CPI will carry more weight, but today's PPI print essentially rolled out the red carpet for a Fed rate cut next week,” said Chris Larkin at E*Trade from Morgan Stanley. “After last week's jobs report, though, the market was already expecting the Fed to begin an easing cycle, so it remains to be seen how much of a near-term impact this will have on sentiment.”

The downside surprise to the PPI in August was driven by a compression of trade margins, reversing their unexpected widening in July, and therefore overstates the softness of producer prices, according to Stephen Brown at Capital Economics.

“Nonetheless, the big picture remains that tariff effects are feeding through only slowly,” he said.

To Neil Dutta at Renaissance Macro Research, firms may be trying to stay competitive to maintain market-share. At the end of the day, tariff related pass-through has not been as much as anticipated, he noted.

“I think the Fed should cut 50 basis points next week — but I don't think they will,” Dutta noted. “The doves on the FOMC have a very strong case to make. The hawks will argue that the unemployment rate is still low, financial conditions are loose, and that there is still upward inflation pressure in front of us due to tariffs.”

The better-than-expected and relatively benign producer price report is both good news and bad news, according to Scott Helfstein at Global X.

“On the positive side, tariffs are not having a drastic impact on company supply chains in aggregate. Alternatively, the slowing in producer inflation could also signal a softening economy. The Fed is likely to take notice, but will still likely deliver a modest rate cut in September,” he said.

“Nothing in today's data should sway the Fed from cutting rates next week,” said Mark Streiber at FHN Financial. “Corporate profit margins surged after the pandemic, and were hovering near all-time highs before the tariffs were implemented. Tariffs have taken a bite out of those margins, but businesses certainly have the ability to absorb the blow.”

Jerome Powell.

If profit margins were tighter to begin with, Streiber noted, businesses likely would have shed employees already to save on costs.

Policymakers are largely expected to cut rates when they meet next week in an effort to counter a rapid slowdown in the labor market. Fed Chair Jerome Powell cautiously opened the door to a cut at the Fed's Jackson Hole symposium last month, and more recent data showed the hiring slowdown extended into August.

Disappointing employment data released Friday validated fears that the US labor market may be on the brink of a downturn and lifted expectations for how much the Fed will lower interest rates this year.

“PPI data is good news for the Fed and marginally raises the probability of three sequential cuts in September, October and December,” said Marco Casiraghi and Krishna Guha at Evercore.

A few more inflation prints would not settle the question of whether the Fed should look through the tariff shock, but risks have already moved into better balance and Powell is sensitive to downside risks to the labor market, they added.

“Core PPI declines further provide cover for a more accommodative monetary policy,” said Eric Teal at Comerica Wealth Management. “The stagnant job market will take precedence as the Fed prepares to reduce rates and stimulate the economy, although we continue to believe the consumer is significantly less rate sensitive than in the past. So more cuts are likely on the horizon.”

Consistently above-target inflation readings may limit its scope to deliver the more aggressive rate cuts that the jobs market side of the dual mandate prescribes, according to Matthew Weller at Forex.com and City Index.

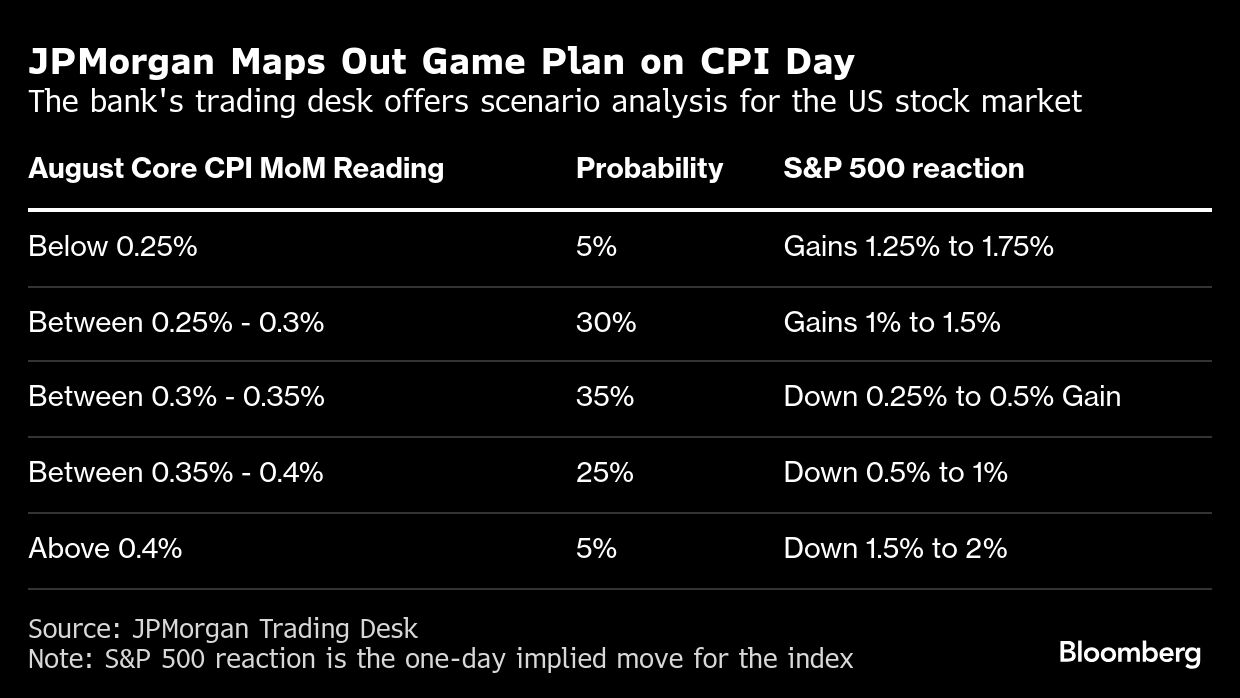

“In terms of a potential market reaction, a surprise drop in this week's CPI report could alleviate that tension and put a 50 basis-point rate cut firmly on the table,” he said.

Brown at Capital Economics says easing labor market conditions mean the Federal Open Market Committee is set to vote for a 25 basis-point cut next week — although “a rare triple dissent” in favor of a 50 basis-point move could steal the headlines.

“We expect the new Summary of Economic Projections to show only a slightly faster and deeper pace of easing than before, leaving the projected interest rate path above market pricing, he said.

The combination of a moderation in jobs growth and still manageable inflation should keep the Fed on track to cut rates, with a 25-basis-point cut expected in September to be followed by three additional consecutive cuts of the same size by January 2026, according to Ulrike Hoffmann-Burchardi at UBS Global Wealth Management.

Against this backdrop, she maintains her positive view on quality bonds and continue to favor medium duration Treasuries as part of a well-diversified portfolio. Falling rates should further support the rally in equities, with the S&P 500 expected to finish 2025 near 6,600 and reach 6,800 by end-June 2026. The gauge is currently above 6,500.

“This steady market rally shows that investors are increasingly forward-looking, pricing in a blend of policy accommodation, improving productivity dynamics, and the potential for fiscal support,” said Mark Hackett at Nationwide.

In many ways, investors are leaning into the idea that slower labor momentum doesn't necessarily derail corporate earnings or broader growth potential, but rather that supportive tailwinds will offset the recent wave of slowing economic data, as evidenced by easier financial conditions, he noted.

Consumer price data due Thursday will offer insights on the extent to which tariffs made their way to American households in August. Core CPI, a measure of underlying inflation excluding food and fuel, probably rose 0.3% for a second month, according to the Bloomberg survey median estimate.

A survey conducted by 22V Research shows investors expect an in-line inflation report tomorrow, with most respondents saying core CPI is on a Fed-friendly glide path.

Options traders are betting the S&P 500 will post a modest swing of nearly 0.7% in either direction following the CPI report, according to Stuart Kaiser, Citigroup Inc.'s head of US equity trading strategy. That's less than the average realized CPI day move of 0.9% over the past year, and below expectations for the next jobs report on Oct. 3. And Kaiser thinks the implied move is high.

Wall Street forecasters are rushing to boost their outlook for the S&P 500 amid prospects for Fed cuts, robust corporate earnings and renewed enthusiasm around artificial intelligence.

Deutsche Bank AG's Binky Chadha raised his year-end target to 7,000, saying half the estimated direct impact of tariffs has already flowed through into inflation. JPMorgan Chase & Co.'s Dubravko Lakos-Bujas warned of risks in the short-term from inflation, but said the gauge could rally to about 7,000 points by early next year amid easing policy headwinds, lower rates and record payouts.

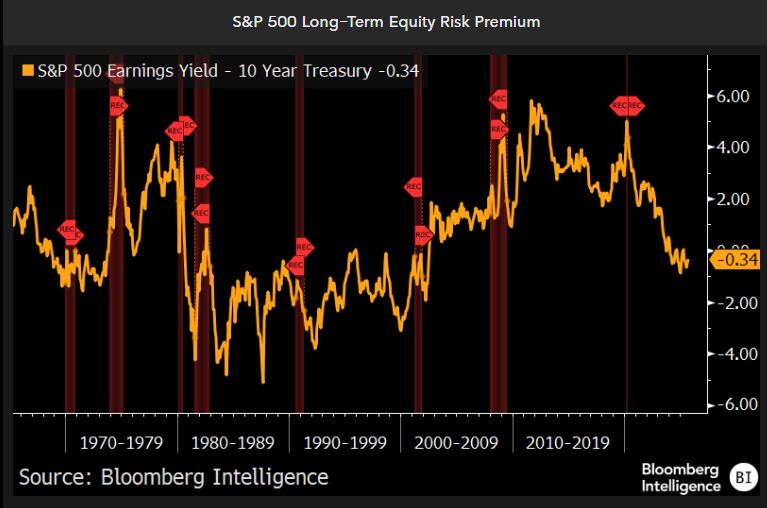

With stocks pressing to new highs, the equity risk premium has all but disappeared, hinting that large- and small-cap stocks are no more compelling than Treasuries or corporate bonds, according to Michael Casper and Christopher Cain at Bloomberg Intelligence.

The S&P 500 equity risk premium — the spread between the earnings yield on stocks and the yield on the 10-year Treasury — is negative and well below its long-term average. While the premium isn't a great predictor of forward returns, it still hints that stocks are expensive relative to bonds.

“To sustain multiples at such extremes, rates will likely have to fall — putting the onus on Fed Chairman Jerome Powell to deliver if stocks are going to continue to rally,” they said. “Past periods of negative risk premia have been met with mixed returns, in aggregate suggesting that stock gains could be poised to slow.”

Corporate Highlights

Oracle Corp. soared after the company gave an aggressive outlook for its cloud business, cementing the software maker's place in the race to support demand for artificial-intelligence computing.

Klarna Group Plc shares jumped in their opening trade, after the company and some of its backers raised $1.37 billion in an initial public offering that signals the market for new listings has room to run.

JPMorgan Chase & Co., Fifth Third Bancorp and Barclays Plc are among banks bracing for potentially hundreds of millions of dollars in combined losses from loans tied to subprime auto lender Tricolor Holdings, according to people with knowledge of the matter.

Tricolor Holdings, a used car seller and provider of subprime loans that focuses on undocumented immigrants in the US Southwest, filed to liquidate in bankruptcy.

GameStop Corp. jumped after the video-game retailer reported Hardware and Accessories net sales that beat the average analyst estimate.

Chewy Inc. sank after the retailer of pet products gave an outlook that failed to live up to high expectations.

Chip-design software maker Synopsys Inc. tumbled after the company warned that US export restrictions are contributing to a slowdown in China.

Delta Air Lines Inc. Chief Executive Officer Ed Bastian said that consumer confidence has rebounded following a “big impact” from tariffs and the economic upheaval earlier this year.

Uber Technologies Inc. customers will be able to book Blade's helicopter and seaplane services directly within the Uber app as early as next year, as part of an expansion of the ride-hailing company's partnership with Joby Aviation Inc.

Lyft Inc. is piloting autonomous rides in Atlanta with a safety driver on board, a long-planned launch meant to help it better compete against Waymo and Uber.

Following the success of its latest Starship test, SpaceX is readying a bigger version of the rocket that should be fully reusable next year, Elon Musk said.

Baker Hughes Co. plans to increase production of its high-performing, gas-fired power generation turbines as the artificial intelligence boom boosts electricity demand from data centers, Chief Executive Officer Lorenzo Simonelli said in an interview.

Brookfield Asset Management said it has already secured investors and deals for its new artificial intelligence infrastructure strategy, as it positions itself to gain from what it sees as a multitrillion-dollar opportunity.

Cenovus Energy Inc.'s top executive said the company doesn't plan to increase its takeover offer for oil sands producer MEG Energy Corp., despite a higher rival bid from Strathcona Resources Ltd.

Vimeo, the online video platform that has struggled to compete against the likes of YouTube and TikTok, agreed to a $1.38 billion, all-cash takeover by European mobile app developer Bending Spoons.

Merck & Co. is terminating its early drug research in the UK and pulling out of plans for a £1 billion ($1.4 billion) London research hub, marking the latest setback for the country's domestic pharmaceutical industry.

Novo Nordisk A/S is slashing its workforce by 11% and pledging to move faster to catch up with Eli Lilly & Co. in the obesity market. That may mean making the company more like its US rival.

A group led by BlackRock Inc.'s Global Infrastructure Partners unit has arranged a roughly $10 billion financing package for its planned investment in Saudi Aramco natural gas infrastructure, people familiar with the matter said.

Nio Inc. raised about $1 billion through a share sale, as the Chinese electric-vehicle maker takes advantage of a recent stock rally to fund its growth.

The S&P 500 rose 0.3% as of 1:29 p.m. New York time

The Nasdaq 100 was little changed

The Dow Jones Industrial Average fell 0.6%

The MSCI World Index rose 0.2%

Bloomberg Magnificent 7 Total Return Index was little changed

The Russell 2000 Index fell 0.1%

The Bloomberg Dollar Spot Index was little changed

The euro was little changed at $1.1703

The British pound was little changed at $1.3532

The Japanese yen was little changed at 147.34 per dollar

Bitcoin rose 1.8% to $113,541.14

Ether rose 1% to $4,346.46

The yield on 10-year Treasuries declined six basis points to 4.03%

Germany's 10-year yield was little changed at 2.65%

Britain's 10-year yield advanced one basis point to 4.63%

The yield on 2-year Treasuries declined three basis points to 3.53%

The yield on 30-year Treasuries declined six basis points to 4.68%

West Texas Intermediate crude rose 1.9% to $63.84 a barrel

Spot gold rose 0.4% to $3,642.42 an ounce

What Bloomberg's Strategists say...

“Preliminary August spending estimates point to a cooling from July's pace, hinting at emerging cracks in consumer momentum. Equity traders, however, will likely be inclined to look past this in anticipation of rate cuts.”—Tatiana Darie, Macro Strategist, Markets Live.

Some of the main moves in markets:

Stocks

Currencies

Cryptocurrencies

Bonds

Commodities

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.