(Bloomberg) -- Inflation is slowing the world over, but some of the biggest money managers say it's no time to ditch protection against rising consumer prices.

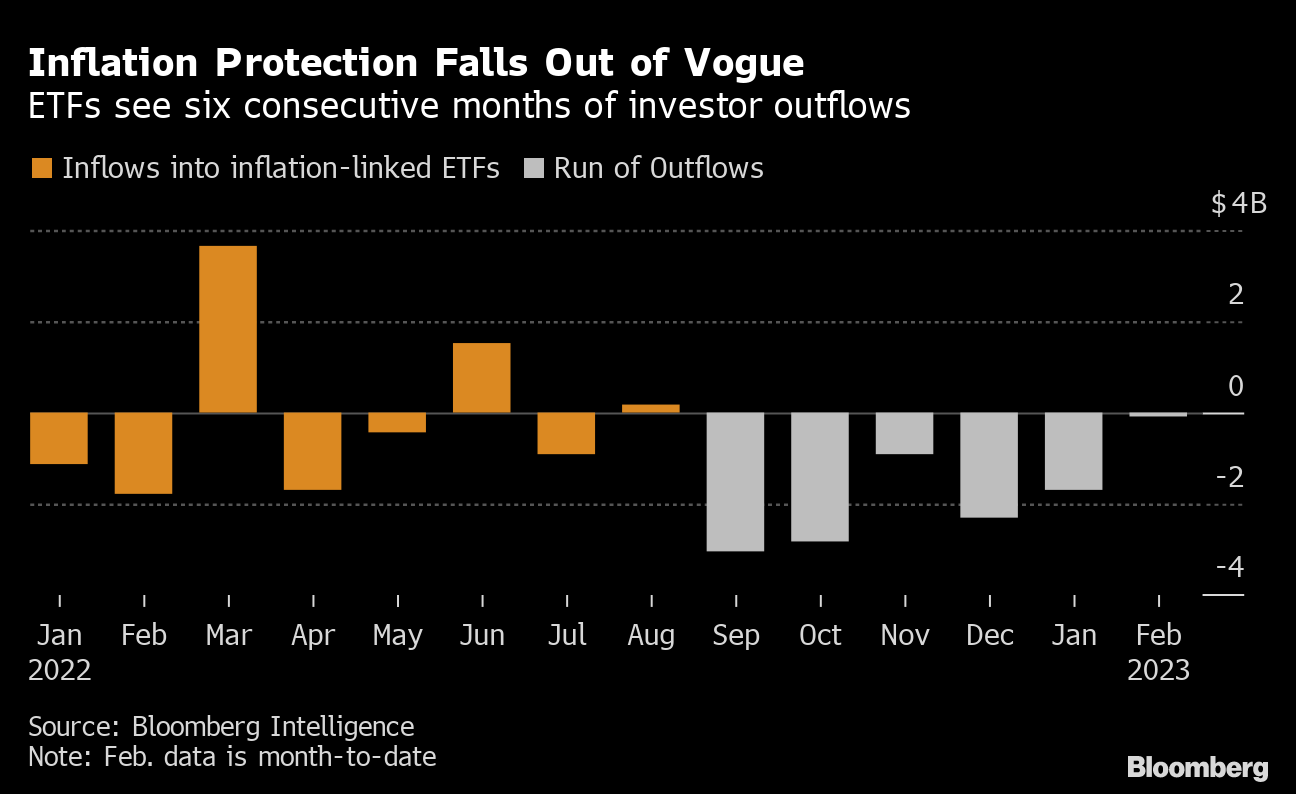

BlackRock Inc., AllianceBernstein Holding LP and Pacific Investment Management Co. warn the market may be too sanguine on the pace of price growth. Investors pulled money from exchange-traded funds tracking inflation-linked government debt for a sixth consecutive month in January, the longest streak in at least six years and a combined net outflow of $10.8 billion, data compiled by Bloomberg show.

They're not saying inflation won't slow — supply bottlenecks have eased and commodity prices have dropped. Their concern is the pace and magnitude of the deceleration traders are pricing in.

“People seem to see inflation coming down and think they don't need inflation protection anymore even if the rate is still high,” said John Taylor, director of Global Multi-Sector at AllianceBernstein. “They are underestimating the structural shifts that could lead to a higher inflation regime such as deglobalization and labor shortages.”

Medium-term inflation expectations in the U.S. — as shown by the gap in yields between regular five-year bonds and ones that are inflation-protected — have shrunk to 2.5% from last year's peak of 3.76%. A similar measure for global markets shows expectations are now below 2%, down from 3.12% in April — the highest in at least 10 years.

Tough Lesson

BlackRock is sticking with its recommendation that investors stay overweight inflation-linked bonds. AllianceBernstein recently increased its exposure to the US Treasury's Inflation Protected Securities, or TIPs. Pimco also bought U.S. index-linked bonds to hedge against the danger of higher-than-expected price growth.

Investors got a brutal schooling in the risks of underestimating inflation in 2022. Global stocks saw $18 trillion of value erased, while US government bonds posted their worst year on record as central bankers scrambled to hike rates and get ahead of spiraling prices after years of loose policy.

Wei Li, the chief investment strategist at BlackRock's research arm, is surprised at the extent to which investors are betting on growth picking up, inflation slowing, and policymakers switching to rate cuts later this year. Her base case is for a mild recession and persistent above-target price growth. The market, meanwhile, is assuming the kind of macroeconomic landscape that will turbo-charge risk assets, she said.

“Persistent inflation is not just a US phenomenon — It's happening across the developed market,” Li said in an interview.

Structural Shifts

To be sure, some of the market moves pointing to an inflation slowdown have faded. But the expected rate is still well below BlackRock's forecasts. The world's biggest asset manager sees the pace averaging around 3.5% over the next five years and settling below 3% beyond that as an aging population shrinks workforces, geopolitical fragmentation reduces economic efficiency, and nations move to a low-carbon industrial model.

“Our view on the structural shifts means inflation will be higher than what we got used to before the pandemic,” Li said. “The reversal of goods prices means getting inflation down from its June 2022 peak of 9.1% to around 4% will be the easy bit. Getting it to settle below 3% will likely be much harder.”

A closer look at the inflation prints coming in globally gives ground for caution.

Core inflation in Europe stuck at a record 5.2% in January and the unemployment rate is at an all-time low of 6.6% — figures which have ECB policy makers stressing the need to avoid a wage-price spiral. In the US, meanwhile, bets are growing for a more hawkish Fed after a surprisingly strong jobs report showed unemployment falling to 3.4%, the lowest rate since 1969.

Sticky, Stubborn

AllianceBernstein's Taylor says the UK is the next place to add a position in inflation-linked securities, though breakevens have room to extend their drop as investors react to cooling headline inflation. Economists see the headline rate easing for a third month to 10.3% in January in data due next week. Even at that level, inflation would still be close to a 41-year high and about five times the Bank of England's target.

As the inflation debate rolls on, Pimco's Alfred Murata recommends hanging on to TIPs and keeping in mind that some key price components will stay stubborn.

“Some key categories will remain ‘sticky,' including wage, shelter, and rent inflation,” Murata wrote in a note. “It will take longer for inflation to approach the Fed's 2% target. Yet, the market is pricing in a far more rapid drop in inflation – to slightly above 2% by summer.”

--With assistance from .

More stories like this are available on bloomberg.com

©2023 Bloomberg L.P.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.