(Bloomberg) --Treasury yields climbed and stocks wavered after the latest jobs report showed a moderating — yet healthy labor market — that will likely make the Federal Reserve hold rates steady for now.

The yield on 10-year Treasuries advanced five basis points to 4.48%. The S&P 500 was little changed. The Bloomberg Dollar Spot Index fluctuated.

Nonfarm payrolls increased by 143,000 last month after a revised 307,000 gain in December. The unemployment rate was 4.0% — the survey used to produce the number incorporated separate revisions to reflect a new population estimate at the start of the year, which makes the figure incomparable to prior months. Meantime, hourly wages climbed 0.5%.

Wall Street's Reaction:

Bret Kenwell at eToro: Strong wage growth is good for workers and should be viewed as a positive for consumer spending. However, Wall Street has watched this gauge closely over the last few years, worrying that too strong of wage growth could push inflation higher.

Outside of the headline result, the latest jobs report is not cause for alarm. While some investors may worry about implications for inflation or rate cuts, make no mistake about it: It's better to have a strong economy and labor market than a deteriorating environment. Remember, stocks tend to do well amid mild inflation.

Ellen Zentner at Morgan Stanley Wealth Management: A lower-than-expected January payrolls number was more than offset by upward revisions to November and December's totals and a downtick in the unemployment rate. Those who'd hoped for a soft report that would nudge the Fed back into rate-cutting mode didn't get it.

Jason Pride at Glenmede: Tighter labor market = wage pressures. A hot average hourly earnings print is another sign of a tighter labor market and points to the potential for resulting inflationary pressures.

The Fed has already been pushing out expectations for its next rate cut, and this report probably justifies that approach, if not nudging them to push out expectations even further.

Florian Ielpo at Lombard Odier Investment Managers: Not as cold as you'd think. This report is not a game-changer for investors: the job market remains strong, which is positive for future profits and signals that short-term rates could remain higher in the US than elsewhere for a longer period.

Charlie Ripley at Allianz Investment Management: Either way you spin it, the Fed should feel quite cozy sitting tight the rest of winter knowing that it was the right decision to hit the pause button on rate cuts.

Seema Shah at Principal Asset Management: Today's jobs report has likely taken a March rate cut off the table. Aside from a slightly disappointing headline payrolls number, the broader picture is still one of labor market resilience and sustained wage pressures. This simply gives the Fed little reason to cut policy rates immediately.

Jeffrey Roach at LPL Financial: This morning's report may be considered a Goldilocks report – not too hot and not too cold. In general, labor demand last year was softer than originally reported but that trend temporarily reversed in November and December. An unemployment rate at 4% is considered very low, giving the Fed reason to keep fed funds unchanged in the near term.

Mark Gibbens at BOK Financial: The report showed a domestic labor market that keeps on dancing to a positive tune. On the negative side of the ledger was average hourly earnings. This level of growth in wages should keep rate cuts by the Fed on the back burner for now.

Jeff Schulze at ClearBridge Investments: The January jobs report missed consensus expectations but strong positive revisions to the prior two months and a drop in the unemployment rate make this a more solid print than the headline numbers suggest at first glance. One fly in the ointment is the pickup in average hourly earnings, however, we believe part of the upside is due to mix-shift distortions resulting from extreme weather, and wages are still running at a pace consistent with the Fed's 2% target on a year-over-year basis.

This release should keep the Fed in wait-and-see mode.

Importantly, today's labor data reaffirms the resilient macro narrative that has emerged over the past several quarters following fears of a slowing labor market last summer. While a knee-jerk reaction could put modest upward pressure on long-term bond yields and, in turn, pressure equity market valuations, this release should support risk assets over the intermediate term as a solid labor market and economic backdrop help validate embedded earnings expectations.

David Russell at TradeStation: The Fed meeting was a non-story and so is the jobs report. Aside from the payrolls miss, unemployment, wages and revisions were strong. This keeps the Fed on hold and focused on the price side of its mandate. It's consistent with a strong economy with the potential of lower rates later in the year, but not decisive one way or the other.

Bryce Doty at Sit Investment Associates: Today's employment report probably keeps the Fed on hold for probably one more meeting. While jobs weren't exceptional my any means, a lower unemployment rate and a strong increase in wage growth means the labor market is still healthy.

Expect yields to drift higher as investors digest the details. However, we doubt this report is strong enough to push yields back up to the recent high.

Mark Hamrick at Bankrate: While inflation has remained elevated, the still solid job market provides a solid underpinning for Americans to focus on their financial goals. Affordability challenges abound given elevated prices and interest rates.

The Federal Reserve has another round of inflation and employment data to mull before the next scheduled announcement on March 19. It is seen remaining patient before making another interest rate move having recently opted to stand pat.

Stephen Brown at Capital Economics: Decline in unemployment rate and healthy payrolls to keep Fed on the sidelines.

Fawad Razaqzada at City Index and Forex.com: Overall, the non-farm payrolls data was mixed-to-positive. The strong wages growth point to inflationary pressures, suggesting no imminent rate cuts should be expected,

Glen Smith at GDS Wealth Management: While Friday's jobs report was weaker-than-expected, the prior two months saw significant upwards revisions in the number of jobs created, so we don't expect Friday's report to derail the Federal Reserve's patient stance when it comes to rate cuts. We would need to see multiple weaker jobs reports in a row in order for the Fed to cut interest rates sooner.

Friday's weaker-than-expected jobs report for January should be viewed through the lens of the blowout jobs report from December, which saw a significant upward revision. It's understandable that job growth slowed slightly in January after a significant hiring boost towards the end of 2024.

Lindsay Rosner at Goldman Sachs Asset Management: Mixed items here. Weak headline NFP with a miss to the downside, however a positive prior revision and an unemployment rate that ticked down to 4%. This month's release was impacted by one-off factors including wildfires in California and a cold snap in other parts of the country. We think the Fed is likely to be cautious about reading too much into today's report.

Corporate Highlights:

Amazon.com Inc. warned investors that it could face capacity constraints in its cloud computing division despite plans to invest some $100 billion this year, with most of the money going toward data centers, homegrown chips and other equipment to provide artificial intelligence services.

Apple Inc. plans to unveil a long-anticipated overhaul of the iPhone SE in the coming days, a move that will modernize its lower-cost model in a bid to spur growth and entice consumers to switch from other brands.

Pinterest Inc. posted strong holiday-quarter revenue and gave an upbeat forecast for sales in the current period, a sign that its advertising business continues to grow despite increased competition from much larger rivals in the social networking space.

Expedia Group Inc. posted better-than-expected gross bookings in the final months of 2024, reflecting resilient demand for travel during the winter holiday season.

Cloudflare Inc., a software company, reported fourth-quarter results that beat expectations.

Nikola Corp. is exploring a possible bankruptcy filing, according to people familiar with the matter, following a tumultuous period in which the electric truck maker has swung between stock-market darling and scandal-plagued enterprise.

Porsche AG is falling further off track from lofty targets set during its splashy stock listing two years ago, with costs mounting from executives having misjudged how eager sports-car buyers were to go electric.

Some of the main moves in markets:

Stocks

The S&P 500 was little changed as of 9:30 a.m. New York time

The Nasdaq 100 was little changed

The Dow Jones Industrial Average was little changed

The Stoxx Europe 600 was little changed

The MSCI World Index was little changed

Currencies

The Bloomberg Dollar Spot Index was little changed

The euro was little changed at $1.0385

The British pound rose 0.2% to $1.2459

The Japanese yen fell 0.2% to 151.76 per dollar

Cryptocurrencies

Bitcoin rose 2.9% to $99,587.95

Ether rose 2.8% to $2,785.1

Bonds

The yield on 10-year Treasuries advanced five basis points to 4.48%

Germany's 10-year yield advanced one basis point to 2.39%

Britain's 10-year yield was little changed at 4.49%

Commodities

West Texas Intermediate crude rose 1% to $71.32 a barrel

Spot gold rose 0.7% to $2,875.02 an ounce

This story was produced with the assistance of Bloomberg Automation.

Asian stocks fell Friday after muted moves on Wall Street as traders awaited US jobs data that will help illuminate the path ahead for interest rates.

Shares in Japan, Australia and South Korea opened lower, while equity futures for Hong Kong also fell. Declines in Tokyo partly reflected a stronger yen, which extended gains against the dollar into a fifth day Friday to trade around the highest level since early December. Prime Minister Shigeru Ishiba will meet with US President Donald Trump on Friday.

The S&P 500 closed 0.4% higher, while the Nasdaq 100 added 0.5% on Thursday. Shares in Amazon.com Inc fell in after-hours trading following earnings results that showed projected profits for the current quarter below analysts' estimates. The shortfall indicates the company continues to ramp up spending to support artificial intelligence services.

Treasuries were slightly lower across the curve Thursday. An index of the dollar tracked against a basket of currencies was little changed.

The moves signal a dose of calm ahead of nonfarm payroll figures due later Friday that will refocus traders away from the drama over tariffs earlier in the week that initially rattled financial markets. Friday's jobs report is expected to show 175,000 new roles added to the US economy. A weak print could boost expectations for further Federal Reserve cuts, while a stronger-than-expected number may have the opposite effect.

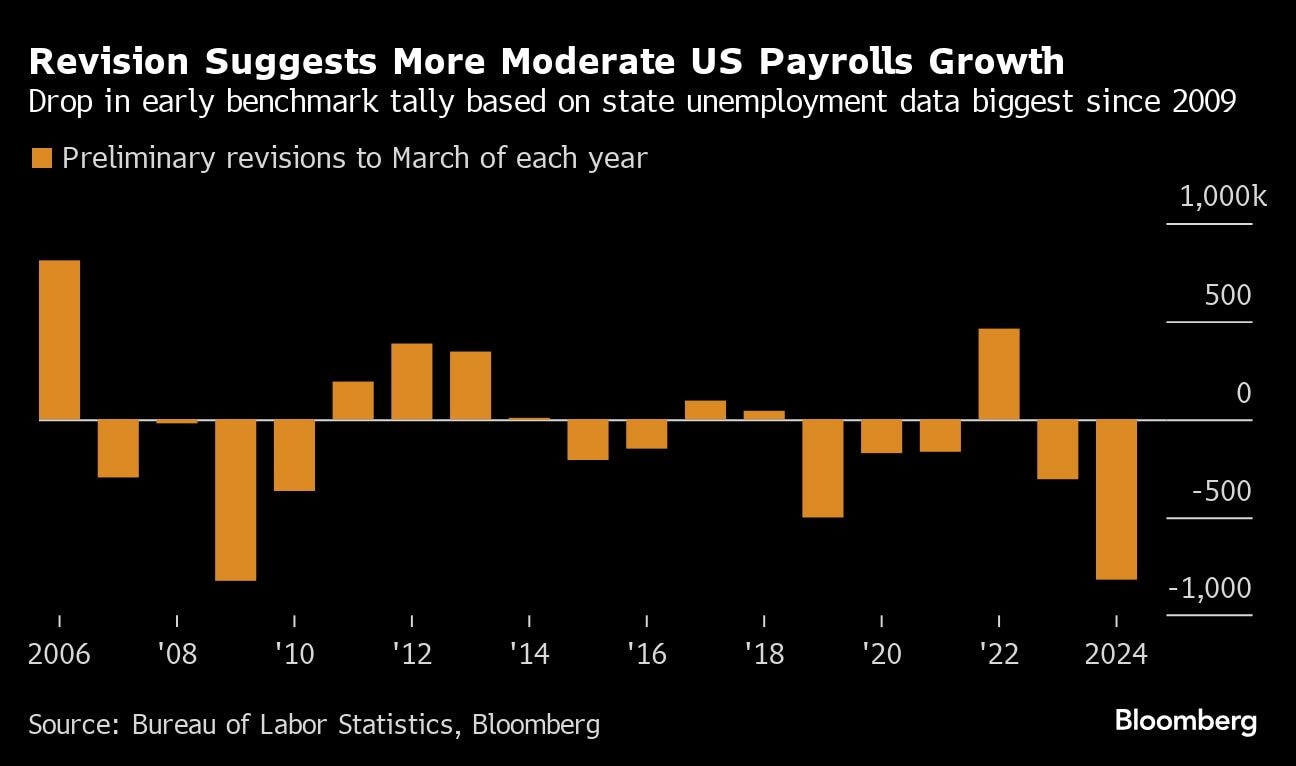

Separate jobs data released Thursday showed initial jobless claims picked up while labor productivity remained robust. In addition to the employment print Friday, Wall Street will be closely watching a revision to job growth. Economists predict that will be substantial, but probably not as bad as initially estimated.

Fed Chair Jerome Powell said last week officials want to see more progress on inflation and would be looking for “serial readings” showing price pressures moving in the right direction.

For now, traders still see the Fed's next move as a cut — although likely not until mid-year. Treasury yields hit 2025 lows this week.

In commodities, gold was steady after retreating from a record high Thursday, its first decline in six sessions. Oil fell as Trump's renewed pledge to drive down the price of crude overshadowed his push for tighter Iranian sanctions.

Key events this week:

US nonfarm payrolls, unemployment, University of Michigan consumer sentiment, Friday

Fed's Michelle Bowman, Adriana Kugler speak, Friday.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.