Nomura initiated coverage on Afcons Infrastructure with a ‘buy' rating. The brokerage has set a target price of Rs 561. The initiation is broadly based on the long history of timely project completion and consistent profitability.

The brokerage notes that the company has shown consistent financial performance. Its conservative approach has helped the company to minimalise its financial risk.

The infrastructure, engineering and construction company known for timely completion of intricate projects, according to the brokerage, distinguishes itself from peers. The execution of complex and multi-faceted projects across industries allows the company to further leverage more opportunities. This also reduces competition and calls for better contract terms, according to Nomura.

The company's CAGR led by robust order book momentum is also cited as a strong positive. This was earlier held back by restrictions on non-fund banking limits but the easing of these has brought in order inflow worth Rs 253 billion, according to the brokerage.

The company's sharp focus on margin sustainability has also been highlighted by Nomura. The robust risk mitigation framework is paired with prudent accounting principles. This, according to Nomura, allows the company to constantly deliver profitability. The brokerage also expects reduction in interest costs and normalisation in tax rate.

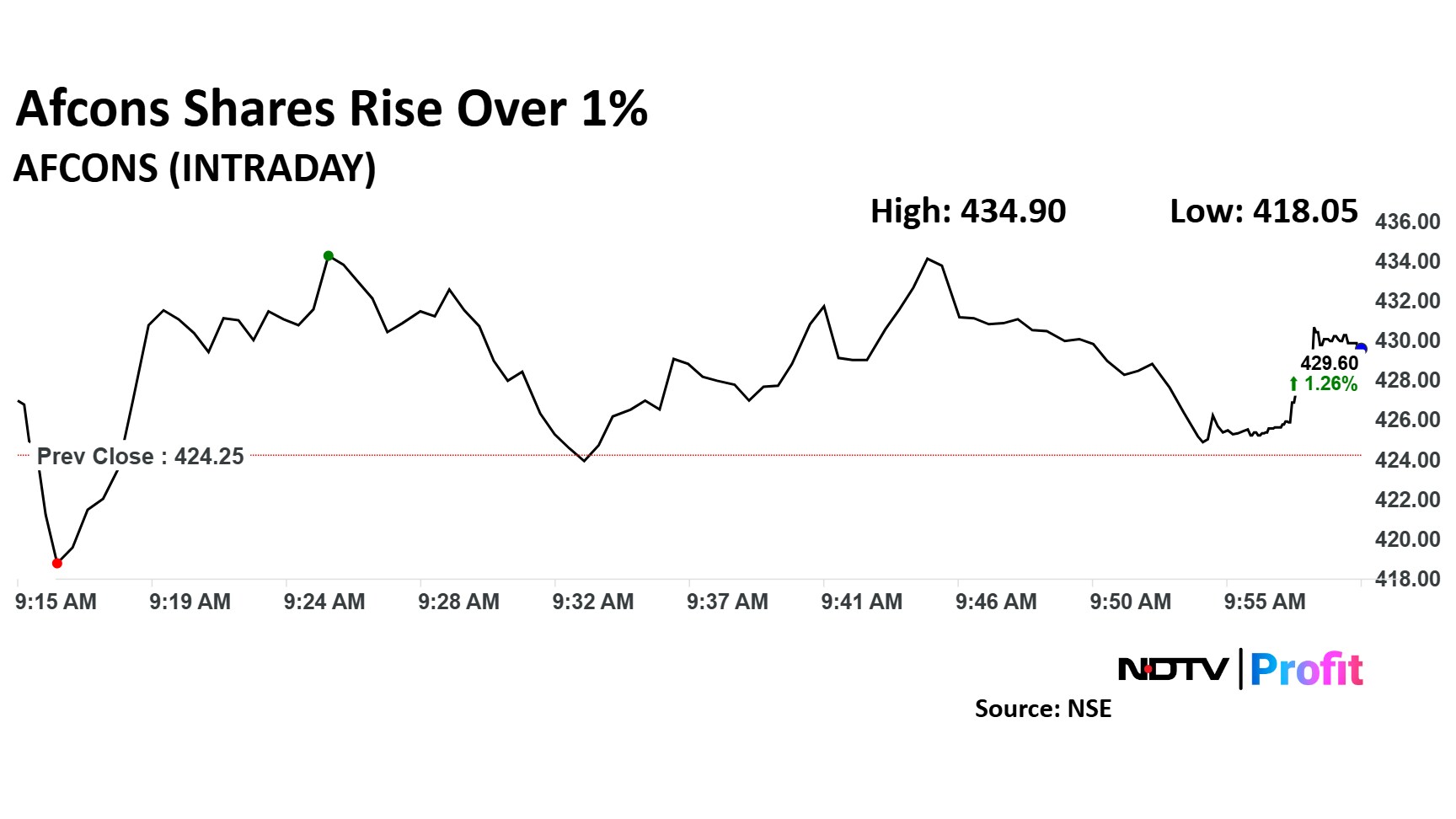

Afcons Share Price

Afcons stock rose as much as 2.51% during the day to Rs 435 apiece on the NSE. It was trading 0.68% higher at Rs 427.15 apiece, compared to an 0.75% decline in the benchmark Nifty 50 as of 10:00 a.m.

It has fallen 22% in the last 12 months. The relative strength index was at 54.18.

All four of the analysts tracking the company have a 'buy' rating on the stock, according to Bloomberg data. The 12-month analysts' consensus target price on the stock is Rs 596.75, implying an upside of 39%.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.