The National Company Law Appellate Tribunal approved UltraTech Cement Ltd.'s plan to acquire debt-laden Binani Cement Ltd., holding that the rival bid by Dalmia Group Ltd. was “discriminatory” to creditors of the stressed cement maker.

Why Was Dalmia Group's Plan Rejected?

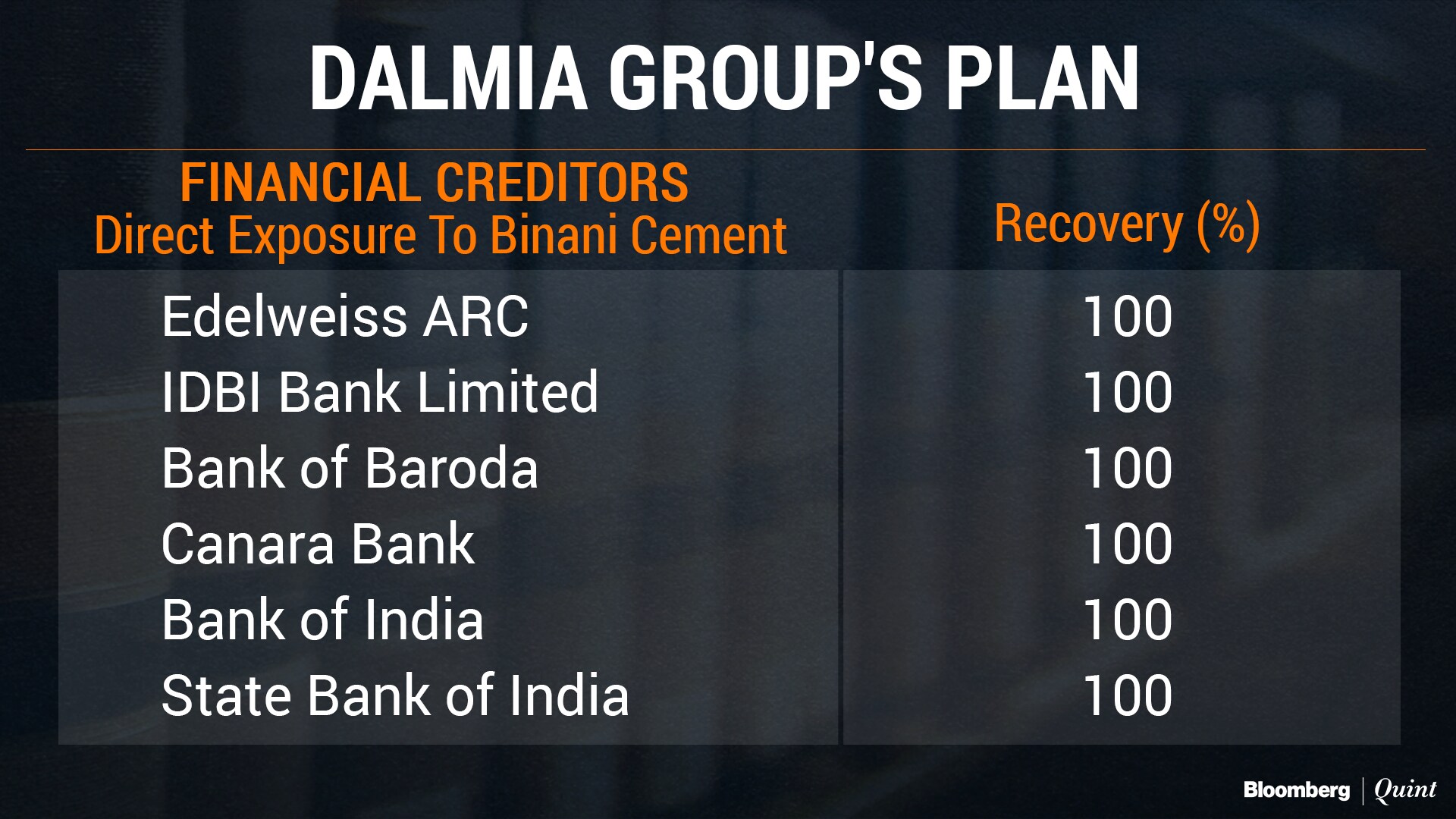

Dalmia Bharat-led Rajputana Properties had offered Rs 6,932 crore for Binani Cement, entailing a 100 percent recovery for financial creditors with direct exposure to Binani Cements. Four of the six financial creditors to whom Binani Cements was a guarantor were offered 100 percent of their claims. The remaining two—Export-Import Bank of India and State Bank of India Hong Kong—were offered 72.9 percent and 10 percent of their claims, respectively.

The NCLAT noted that Dalmia Group's plan discriminates between financial creditors based on whether they have direct exposure to Binani Cements or have been given guarantees by it. Even similarly situated financial creditors with guarantees from Binani Cement have been discriminated against, the appellate tribunal said, pointing to the amounts offered to Export-Import Bank of India and State Bank of India Hong Kong.

The Kolkata bench of the National Company Tribunal had also come to the same conclusion in May this year.

Dalmia Group's argument that the intent of the insolvency law is to bind minority financial creditors with the majority's decision was rejected by the NCLAT.

The way this order reads, it would terrify me as a lender, Nilang Desai, an insolvency partner at AZB told BloombergQuint. The order seems to suggest that all creditors—let alone the distinction between secured and unsecured—must be treated equally, he said.

When a lender comes into a company, it makes a credit call—if I'm going to lend Rs 100, what's my security? What do I get in the worst case scenario? For instance, if I have given a loan worth Rs 100 and my security is worth Rs 200 and someone else has given a Rs 100 loan against a security worth Rs 120 and assume the value of the respective securities falls to Rs 100 and Rs 50 respectively. If you have to treat both these secured creditors equally, what is the point of me having lent with a higher cover of security?Nilang Desai, Partner, AZB & Partners.

If this principle has to be followed, what is the point of making a credit call; just lend, Desai said.

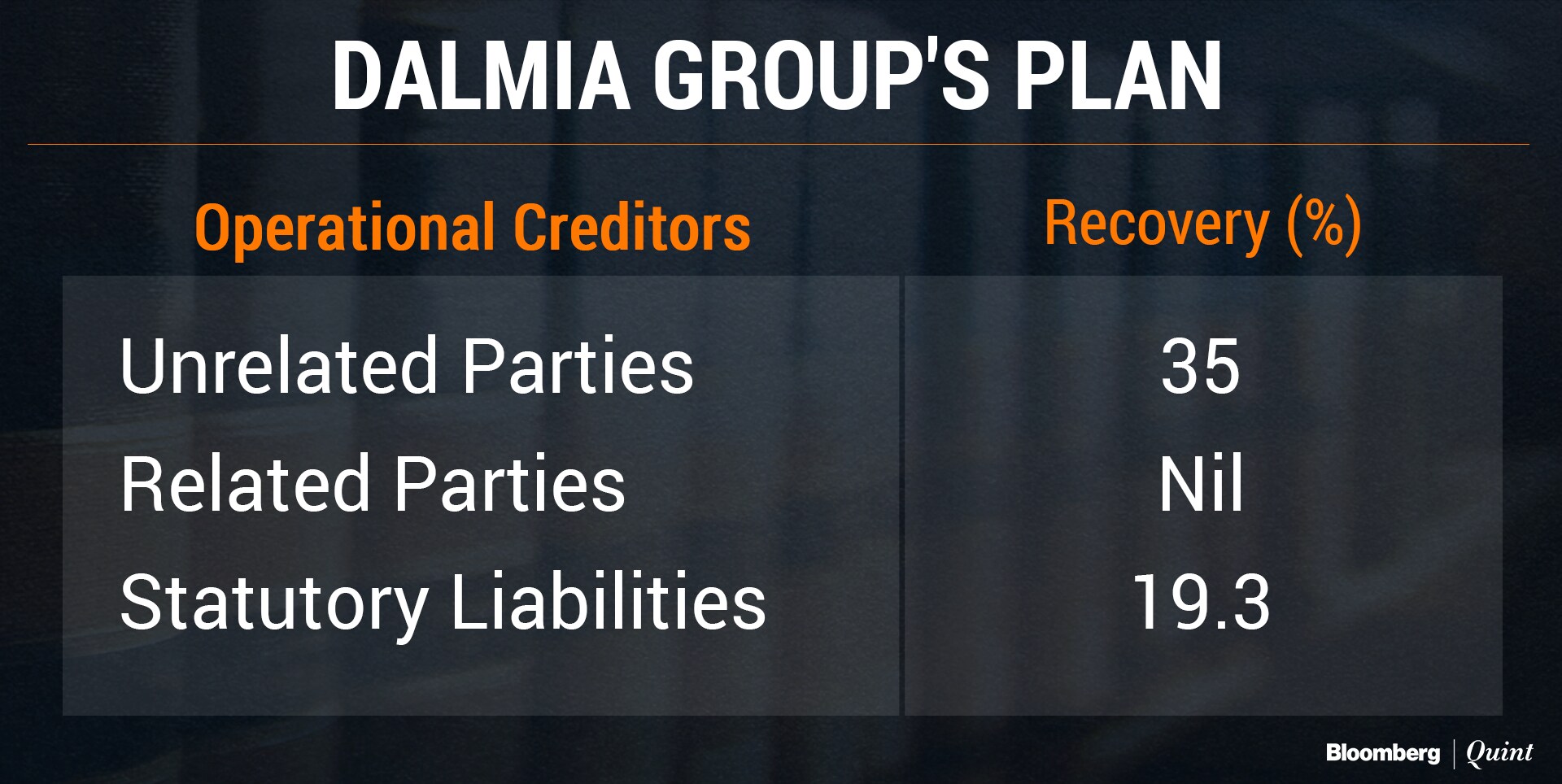

The appellate tribunal has applied the principle in the context of Binani Cement's operational creditors. It has rejected Dalmia Group's plan on the grounds of differential treatment between similarly situated operational creditors.

“...‘unrelated parties' have been provided with 35 percent of their verified claim which is about Rs 90 crore. However, ‘related parties' have not been provided with any amount.”

Desai explained that a lot of committee of creditors would look at the liquidation value of the distressed company and give operational creditors at least that value, and in some cases, even more. But now the NCLAT has said operational creditors need to be treated equally and fairly even without explaining what that means, it's extremely unhelpful, he pointed out.

The law assures operational creditors at least the liquidation value. Over and above that, you can more or less choose what you (creditors' committee) want to give. You can't discriminate between two paper delivery guys but let's say, one operational creditor supplied you coal and the other supplied paper. You may say that the one who supplied me coal is a lucrative supplier and pay him more.Nilang Desai, Partner, AZB & Partners.

None of these principles have been explained, he said.

Legal principles and clarity around them aside, the NCLAT seems to have focused on the commerce of it, Kumar Saurabh, an insolvency partner at Khaitan & Co., said.

The finer points will need to be debated as we go along. Non-discrimination is a well-recognised principle even under the Companies Act. Within secured creditors, can you distinguish based on the security—these things probably weren't even presented to NCLAT.Kumar Saurabh, Partner, Khaitan & Co.

The appellate tribunal concluded that in accepting Dalmia Group's resolution plan, the creditors' committee had failed to safeguard the interest of Binani Cement's stakeholders and had also ignored UltraTech's plan which had taken care of maximisation of the assets of the company.

Why Has UltraTech's Plan Been Accepted?

The NCLAT examined several clauses of the process document to point out that the creditors' committee had ample power to accept any plan before it's approved by the NCLT.

“Clause 1.6.1 [of the process document] provides that the committee of creditors have the right to accept or reject one or all plans prior to approval of the same by the Adjudicating Authority.”

Given that UltraTech had submitted its resolution plan on March 8, 2018, and the creditors' committee had voted on Dalmia Group's plan only on March 14, the revised plan of UltraTech should've been considered. The argument that UltraTech's offer was merely an email didn't find favour with the NCLAT. Dalmia Bharat had argued that since UltraTech was a late bidder, it's offer shouldn't be considered.

The fact that UltraTech's offer of Rs 7,950 crore gives a 100 percent recovery to financial and operational creditors and some amount of working capital to Binani Cement also weighed on NCLAT.

The NCLAT has concluded that these were two competing plans that have come within the timeline and the creditors' committee has all the powers to negotiate, Saurabh said. In the process of negotiation, if the value goes up and it leads to better recovery, then you can't cite process, he added.

If the process can be slightly modified to improve recovery, I think that has to be considered.Kumar Saurabh, Partner, Khaitan & Co.

Operational Creditors Can't Be Ignored

In upholding UtraTech's resolution plan, the NCLAT has spelled out certain principles that will impact the decisions of creditors' committees in pending and future cases. They are:

- The liabilities of all creditors who're not part of creditors' committee must also be met in the resolution.

- Financial creditors can modify the terms of existing liabilities, while other creditors cannot take the risk of postponing payment for better future prospects i.e. financial creditors can take a haircut and defer their dues, but the operational creditors need to be paid immediately.

- If one type of credit is given preferential treatment, the other type of credit will disappear from market. This will be against the objective of the IBC of promoting availability of credit.

- The IBC aims to balance the interests of all stakeholders and doesn't maximise value for financial creditors. Operational creditors must get at least a similar treatment compared to the dues of the financial creditors.

The financial creditors cannot disown the consideration for other stakeholders, Desai pointed out. But that doesn't mean that they have to take a haircut and pay the operational creditors, he added.

If there are two competing plans and one is paying operational creditors better value, the financial creditors must consider it. But looking after them doesn't mean they have to pay operational creditors out of their own pocket.Nilang Desai, Partner, AZB & Partners

Desai also said that the principle laid down by the NCLAT will act as a delayed Diwali gift for some of the pending cases as well. For instance, the Essar insolvency case, where a bunch of creditors have approached the NCLT on grounds that the resolution plan accepted by the committee of creditors doesn't take their dues into consideration.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.