Data which showed that India's GDP growth has fallen to a fourteen-quarter low has sparked a debate about the underlying strength (or the lack of it) in the economy. At a very basic level, the data tells us that private investment in the economy remains absent, consumption has taken a hit perhaps due to temporary factors like demonetisation, and government spending could slow due to stretched finances.

But these numbers don't seem to tell the full story. Economists are linking the slowdown to factors like a decline in flow of credit to the commercial sector; they are also linking it to export slowdown and substitution of local manufacturing with cheaper imports. In addition, intangibles that remain up for debate include whether the shift to a formal economy has disrupted supply chains and eventually demand.

BloombergQuint brought together Sajjid Chinoy, chief economist at JPMorgan India, Praveen Chakravarty, visiting senior fellow at the IDFC Institute and Ajit Ranade, chief economist of the Aditya Birla Group to debate India's growth slowdown.

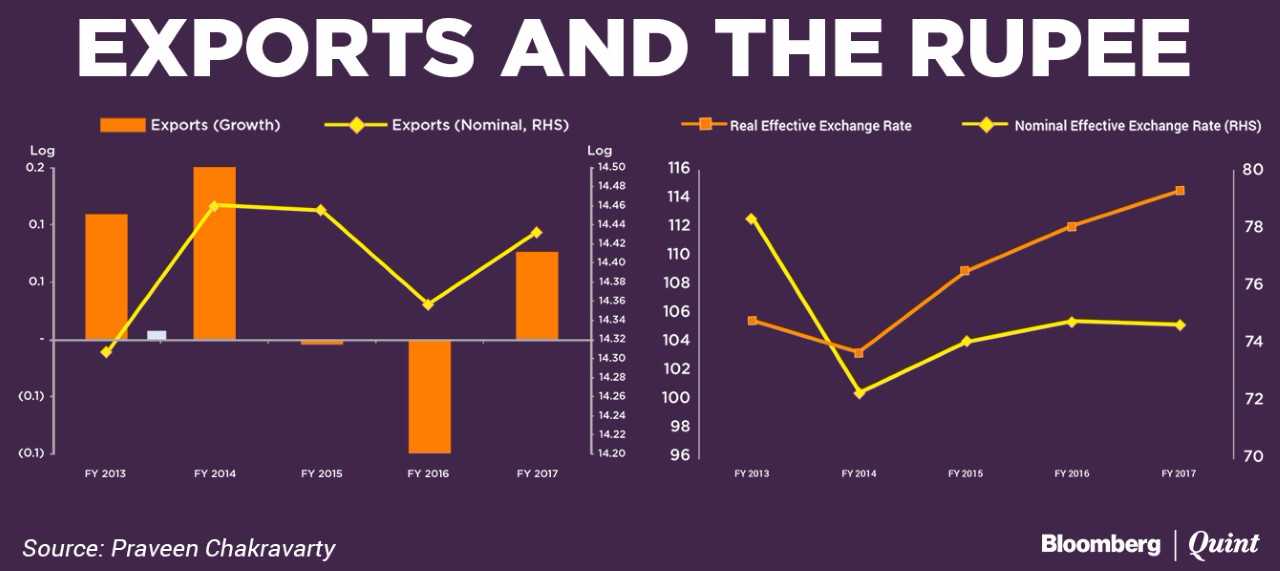

The Export Link

All three economists agreed that the slowdown in exports is a factor that is adding to the slowdown in GDP growth. Data compiled by JPMorgan's Chinoy showed that high GDP growth of 8.8 percent in the 2003-08 period had been accompanied by double-digit export growth. In contrast, exports have grown at a mere 3.1 percent between 2013-17, which explains part of the weakness in overall GDP growth. This, according to Chinoy is one factor behind the slowdown in growth, which began even before one-time shocks like demonetisation.

A sector of the economy which is 20 percent of the economy has experienced a slowdown of 15 percentage points. The import content of exports is about 25 percent. So, if I do the math, that alone shaves off 200 basis points from headline GDP growth. So the movement from 9 percent (growth) to 7 percent (growth) is explained by one factor – exports.Sajjid Chinoy, Chief India Economist, JPMorgan

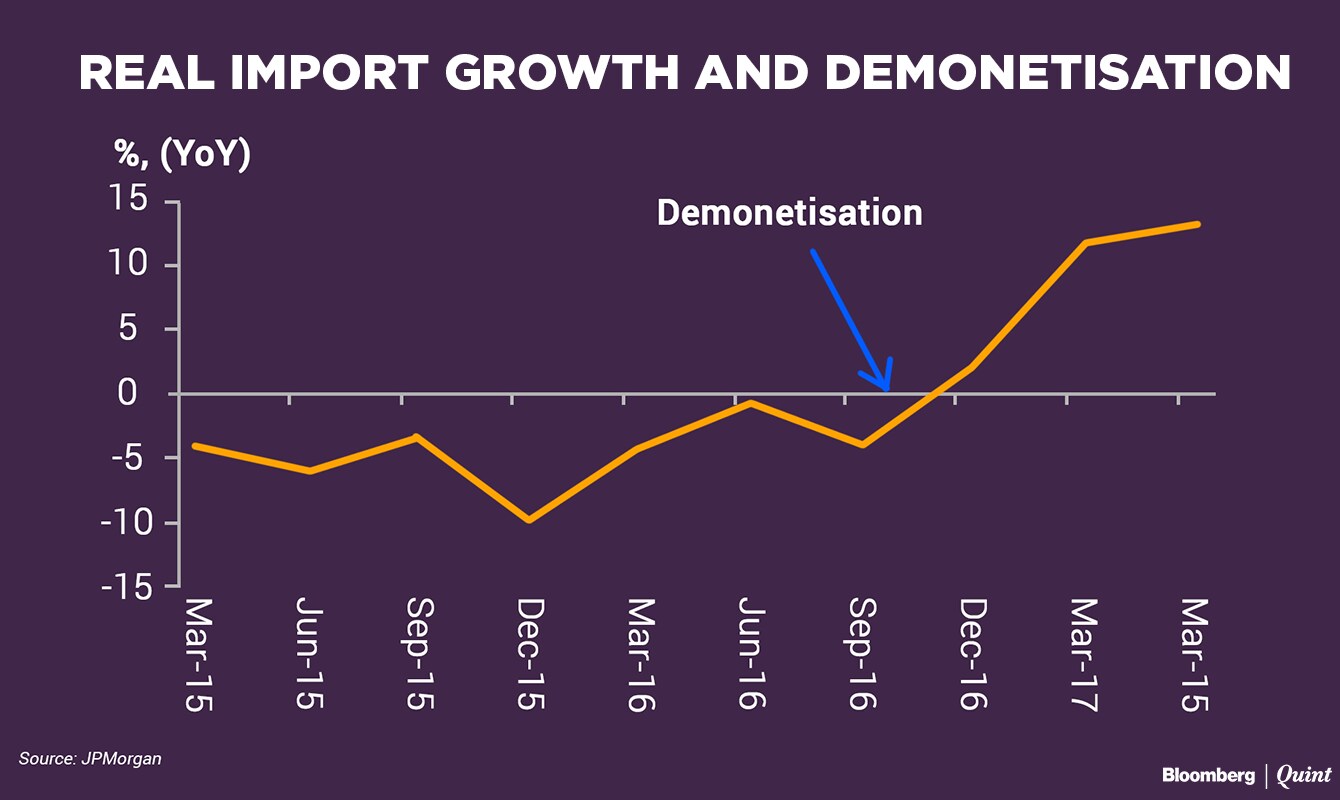

Demonetisation Disruption

While exports have slowed, imports (excluding gold and oil) have risen suggesting that Indian firms are losing business due to both lower outbound shipments and substitution of domestic orders with cheaper goods from abroad.

One reason for this, suggests Chinoy, could be the disruption in supply chains in the aftermath of demonetisation. The currency exchange program which took away 86 percent of the currency in circulation hit transactions temporarily but also impacted those who may not have been able to survive the loss of business.

“There is more and more evidence now that supply chains have been disrupted and there are permanent output losses. That is showing up in lower activity at home and higher imports from abroad,” said Chinoy while adding that net exports, shaved off 260 basis point from growth in the first quarter of the current year. Imports which were contracting before demonetisation have seen a surge in the quarters since, Chinoy pointed out.

Export Hit To Manufacturing

Ranade of Aditya Birla Group argued that slower exports and higher imports are impacting the manufacturing sector, which remains sluggish. Goods exports are highly correlated with manufacturing, said Ranade while adding that poor performance on the export front has translated into weakness in manufacturing.

The manufacturing sector grew at 1.2 percent in the first quarter of the current year.

Ranade blames the strong rupee for the weakness in exports. Chakravarty, while acknowledging that global growth may be a more dominant factor in export growth, questioned whether a relatively overvalued currency could have led to loss of market share in export segments such as textiles.

I definitely think that exchange rate is a very important factor which impacts not just exports but non-export related industry too.Ajit Ranade, Chief Economist, Aditya Birla Group

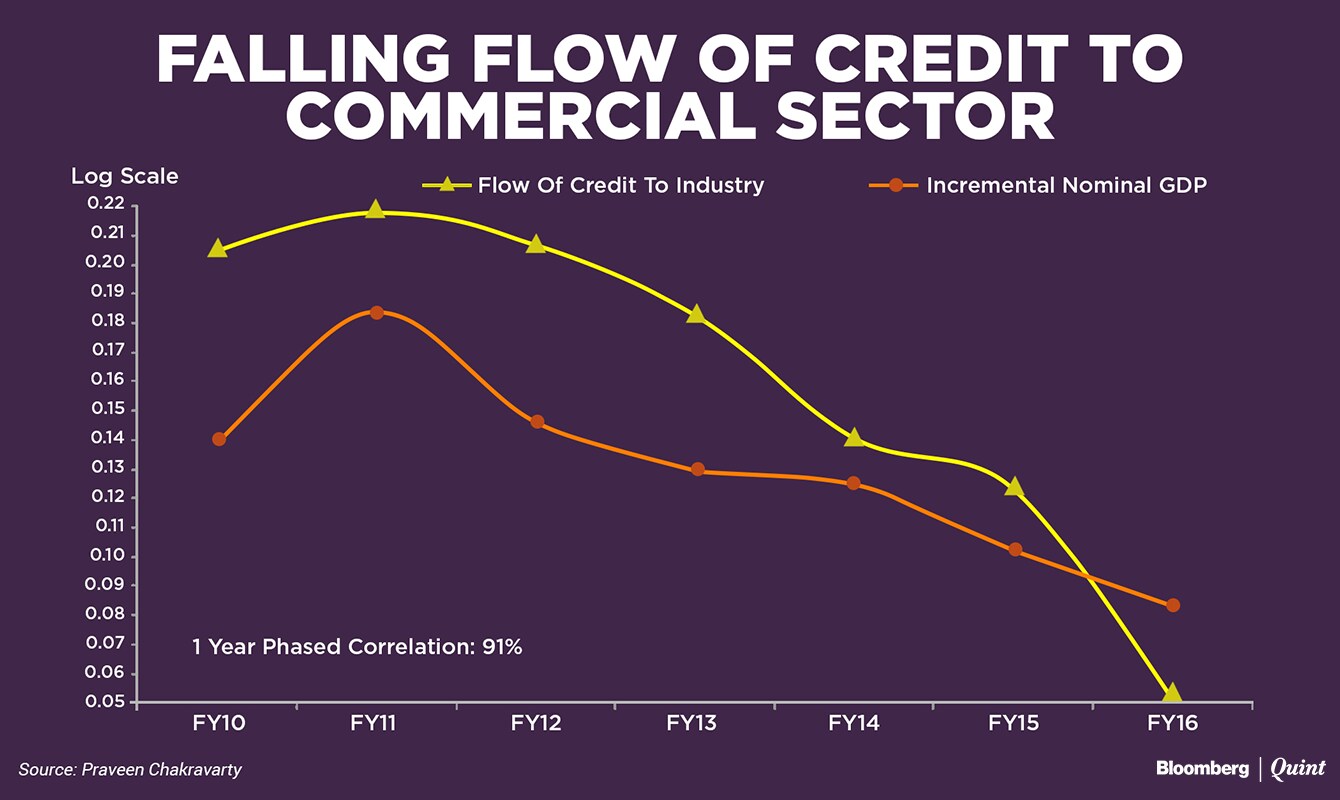

Slowing Credit Flow To The Economy

While the export slowdown has added to pressure points in the economy, the lack of private investment remains the biggest challenge. Private investment, as measured by gross fixed capital formation, as a percent of GDP, has fallen to 27.5 percent from over 30 percent a few years ago.

Low capacity utilisation continues to be blamed for the lack of fresh investment but Chakravarty points to the close correlation between nominal GDP growth and the flow of credit to the commercial sector. The flow of credit to commercial sector has been declining, shows RBI data compiled by Chakravarty. Given that, the slowdown in nominal GDP growth should come as no surprise, he said.

The argument being that credit will spur output. So using credit as the lead indicator, a one-year phased correlation works out to be 91 percent.Praveen Chakravarty, Visiting Senior Fellow, IDFC Institute

A single word describes this phenomenon, said Chinoy. “Deleveraging.” The process of deleveraging involves credit growth slowing more than nominal GDP growth, he explained.

India is facing what is being termed as a twin-balancesheet problem which refers to highly leveraged corporate balancesheets and, in turn, highly stressed bank balancesheets. Stressed loans, including restructured loans, on the books of Indian banks have risen to 12 percent of total loans, according to a presentation made by Reserve Bank of India Deputy Governor Viral Acharya on September 7. While the RBI and the government have been working to resolve bad assets, particularly through the new Insolvency Law, the process is a slow and grinding one.

This could continue to weigh on the economy, said all three economists.

No Easy Answers

With weak exports and the twin-balancesheet problem identified as two key trouble spots for the economy, BloombergQuint asked all three economists for their policy prescription, if any, to reverse the slowdown.

Ranade pointed to the currency as one area that needs focus. When asked what more the RBI can do about the currency against the backdrop of strong inflows, which have almost entirely been mopped up by the central bank, Ranade said that there are no easy answers but the issue warrants greater attention.

Chakravarty said that it is important to revive flow of credit to industry and added that perhaps policy makers could look at issues related to access to credit. “I'm not ready to give up on private investment just yet and wait for animal spirits to kick in,” he said. Chakravarty added that a signal, perhaps in the form of higher recapitalisation amount of Indian banks, could help.

According to Chinoy what will help most is “doubling down” on the asset resolution process. “This is an unpopular answer because this means that growth could get weaker before it gets stronger,” said Chinoy.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.