Credit growth in the Indian banking system is now at its highest in over a decade. But is this revival helping India's 64 million micro, small and medium enterprises?

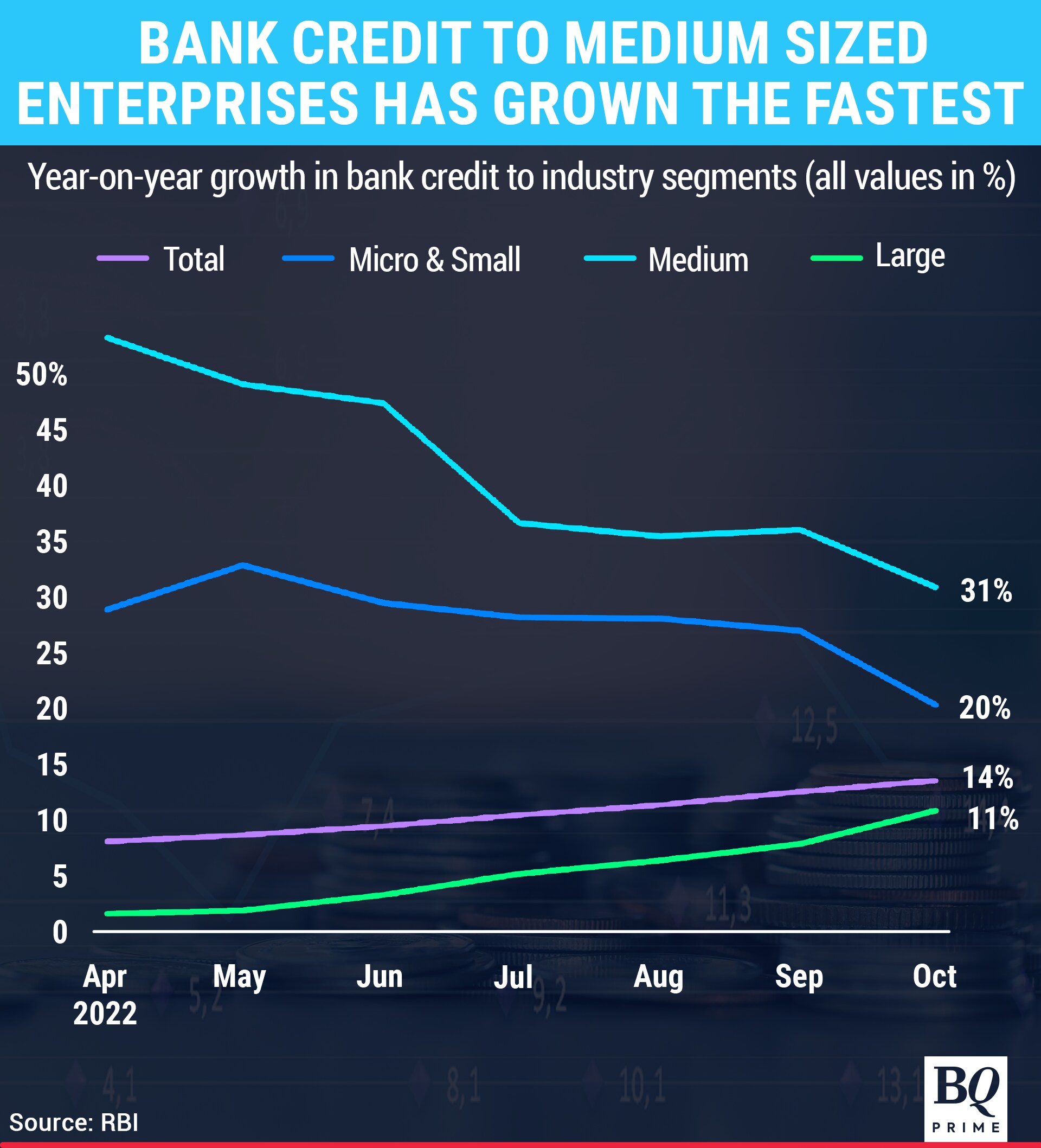

Bank credit sanctioned to such businesses jumped 26% year-on-year in October, according to Reserve Bank of India data. Even, non-banking financial companies have expanded their loans to such enterprises as well. A total of 11.6 lakh new-to-credit MSMEs availed credit in FY22, according to data from TransUnion CIBIL.

“Most of the entities are targeting MSMEs for their growth aspirations as far as assets under management are concerned,” Karthik Srinivasan, group head of financial sector ratings at ICRA, told BQ Prime.

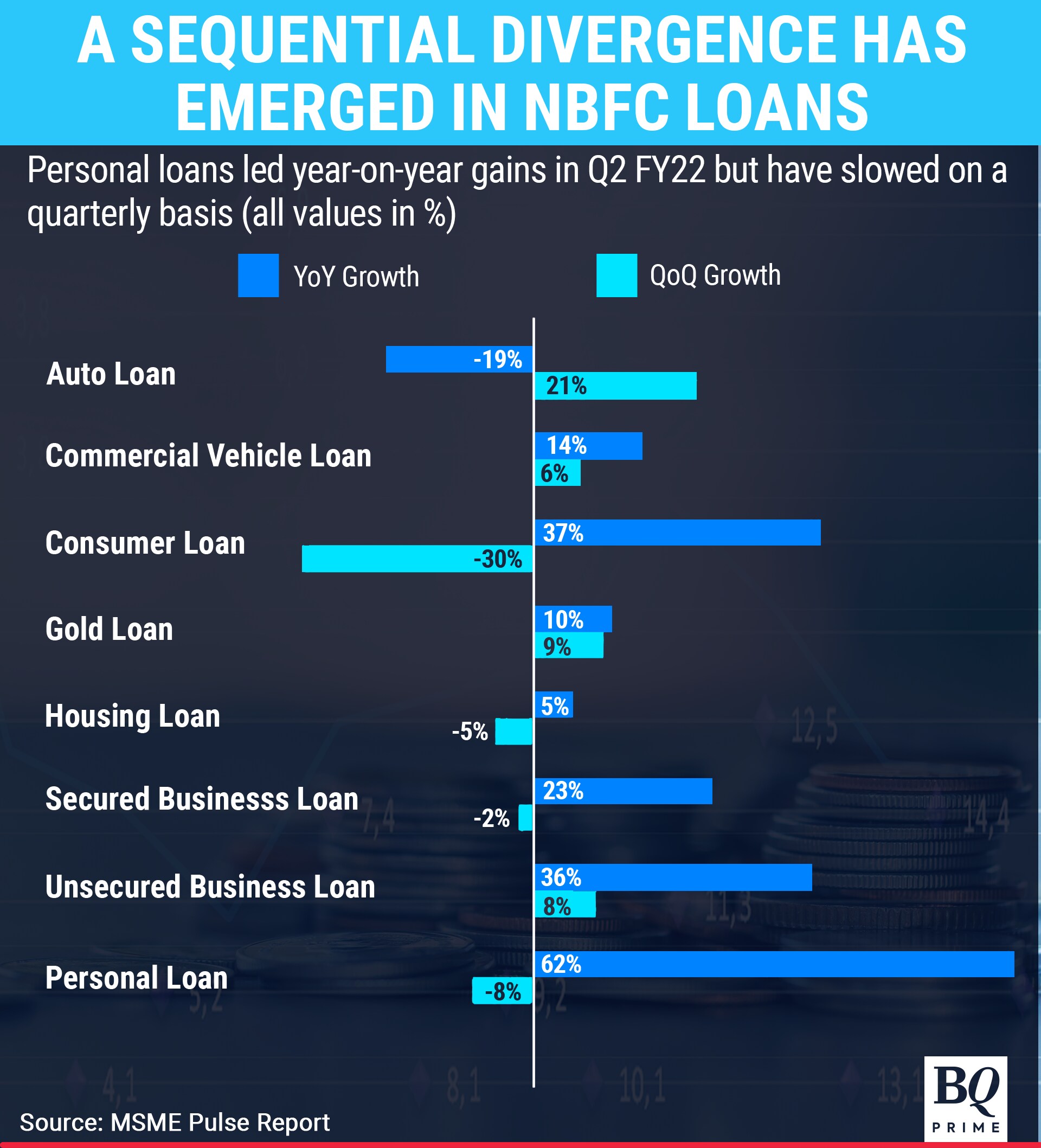

Secured and unsecured business loans granted by NBFCs also jumped by 23% and 36% year-on-year in the second quarter of FY23, according to data from the Finance Industry Development council, an industry body for NBFCs.

This growth in bank lending to MSMEs over the past year has been second only to retail credit.

While banks have the upper hand on the retail lending side, NBFCs seem better suited to servicing the credit needs of small enterprises, according to industry executives.

“Banks have so much more business that is easier to underwrite and that just walks in through the door,” Jairam Sridharan, managing director of Piramal Capital and Housing Finance, told BQ Prime.

Serving small businesses—especially ones that have cash-heavy operations—can end up being uneconomical for banks since the ticket sizes are tiny compared to the effort, he added. “For a bank, it might just not be worth the time,” he said.

But as enterprises get larger and develop more complex needs—foreign exchange services, for instance—banks invariably become better suited to service them.

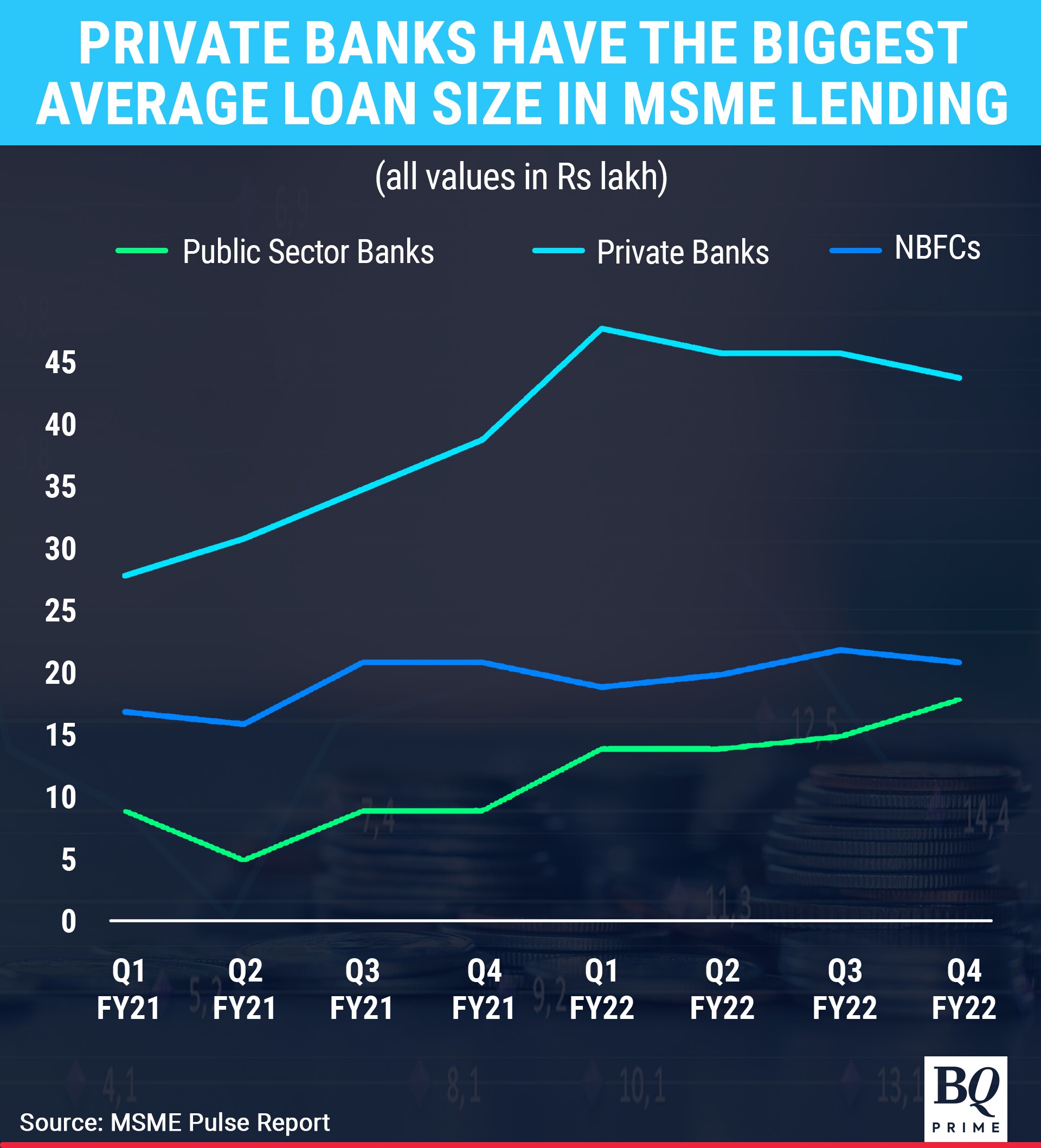

The average ticket size for a loan made to a medium sized enterprise stood at Rs 1.4 crore in the final quarter of FY22, according to the Small Industries Development Bank of India's MSME Pulse report. Loans to small and micro-sized businesses, on the other hand, had an average ticket size of Rs 59 lakh and Rs 9 lakh, respectively.

“Banks may have slightly higher costs from the point of view of infrastructure, etc., but they also have a lower cost of funds,” Manish Kothari, business head of commercial banking at Kotak Mahindra Bank, told BQ Prime.

Unless an entity is using technology to fine tune their underwriting or generate leads, there is not much of a difference in the cost for banks and NBFCs, he said. Instead, the difference, according to Kothari, lies in risk appetite and the lender's specialisation in a particular segment or geography. “NBFCs, invariably you will find, do take higher risks,” Kothari said.

Being concentrated in a specific cluster can also allow NBFCs to distribute their offerings more deeply, he said. “NBFCs also end up focusing more on the smaller companies because the pricing is better,” Kothari added.

Even though quarterly loan disbursements to MSMEs have doubled over the last two years, loan approval rates for the medium-risk tier segment have decreased for public sector banks and NBFCs, according to the MSME Pulse report.

Approval rates for private banks have remained unchanged at around 30-35%. Sticky approval rates amid a high credit demand environment could also indicate that lenders are yet to significantly change their risk appetite in the segment.

Although India has over 6.4 crore MSMEs, only 25 million have ever been granted credit from institutional lenders, according to TransUnion CIBIL data.

Of the Rs 3.25 lakh crore worth of credit issued to MSMEs in the final quarter of FY22, 78% went to medium and small enterprises and the remaining to micro enterprises, according to the report. This is despite the fact that microenterprises—at 6.3 crore in total, according to CII data—far outnumber the 3.35 lakh medium- and small-sized enterprises.

The micro sector also employs 97% of people in the industry, according to the Ministry of MSME's 2021-22 annual report.

Even though micro-sized firms are seemingly ubiquitous, such as corner retail shops, individual dairy units, and others, a lack of growth and limited collateral may inhibit lenders from underwriting them.

The firm landscape in India is dominated by small firms that do not grow with age. Around 94.6% of firms have fewer than 5 workers, according to a 2021 World Bank program appraisal document.

Keeping Pace Or Growing Beyond

The credit demand from smaller enterprises has been driven both by working capital credit and longer-term loans for capacity expansion.

“We are increasingly seeing [capital expenditure], especially in the micro segment,” Sridharan said. This is especially true for enterprises removed from the export sector, which is seeing a slowdown, he added.

The split between working capital and capex-oriented loans for MSMEs is about 50/50, with term loans inching higher recently, according to Raman Aggarwal, independent director at FIDC. The growth in demand for working capital was also pushed up by increases in commodity prices, which have somewhat cooled now.

But even if inflation returns to normalcy, it isn't expected to dent the demand for working capital in a marked way. “Inflation going down or commodity prices generally cooling is not something which will impact working capital as much as compared to how the economy grows,” Kothari said.

Cash Flow Shake Up

Among the biggest impediments to lending to small businesses is a lack of adequate collateral.

While discounting the invoices of a small business that supplies a AAA-rated corporation is easier given that their cash flows have an implicit backing, such determinations are harder to make about other businesses. But that might change if lenders start incorporating cash-flow based factors in their determinations.

RBI's decision to add GST data to the account aggregator framework is a step in that direction.

“It's like making something officially available that was otherwise accessed directly or indirectly because the whole issue previously came with it,” Aggarwal said. Without significant changes to the underwriting techniques, though, the GST integration will stay limited to simply formalising data flow.

The launch of the open credit enablement network is expected to further embolden cash flow-based lending, but it's still early days on that front. “This is clearly a change that has already started to happen, but for it to become meaningful, it may take another four or five years,” Kothari said.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.