Bitcoin began the week on the back foot following a prolonged selloff that has put the token on track for its worst month since 2022.

After regaining some ground over the weekend, the original cryptocurrency fell as much as 3.1% to dip below $86,000 on Monday. It was trading at around $85,700 as of 9:53 a.m. in New York.

While that's higher than the Friday lows of $80,553, traders see little cause for celebration. The wider crypto market is in a pronounced slump despite surging institutional adoption and a series of policy wins pushed for by US President Donald Trump, who has embraced the industry.

“Early trading today is showing slight weakness, but the moves are fairly small and within normal variations,” said Caroline Mauron, co-founder of Orbit Markets. Bitcoin is likely to trade in $80,000 to $90,000 range throughout the week, as the market looks for clues about the Federal Reserve's upcoming rate decision, she added.

In crypto options market, traders are building downside protections at lower levels even Bitcoin prices have seen a slight rebound in the last 24 hours. Demand for put options at the strike of $80,000 has surpassed those at $85,000, becoming the most popular contracts, according to Coinbase-owned crypto exchange Deribit.

Meanwhile, the Bitcoin funding rate - a key measure of crypto market sentiment - has turned negative in the last few days, according to CryptoQuant, meaning there is more demand for bearish bets in the perpetual futures market than bullish positions. That figure had been persistently positive even amid the market rout in recent weeks. The flip points to signs of deepening slump in digital assets as more traders bet against the largest cryptocurrency.

Without a turnaround, November will become Bitcoin's worst month since a string of corporate collapses rocked the crypto market in 2022, a wipeout that culminated in the downfall of Sam Bankman-Fried's FTX exchange.

Traders are watching $85,200 as a key support level after last week's breakdown, said Rachael Lucas, analyst at BTC Markets.“Technicals and macro headwinds are dominating over fundamentals right now, but history shows these liquidation flurries often precede bounces if no new shocks hit,” she added.

Despite a weekend rebound, Bitcoin remains about 30% below its record high last month, and it's unclear how long the recovery will hold without stronger tailwinds. Open interest in perpetual futures has yet to bounce back, lingering 36% below its October peak of $94 billion.

Investors have withdrawn more than $3.5 billion from a group of US-listed Bitcoin exchange-traded funds, vehicles that have emerged as a major driver of the token's price since their debut. A sustained reversal of those outflows has yet to emerge.

“Unlike prior crashes driven primarily by retail speculation, this year's downturn has unfolded amid substantial institutional participation, policy shifts, and broader macroeconomic headwinds,” Deutsche Bank AG analysts wrote in a note Monday.

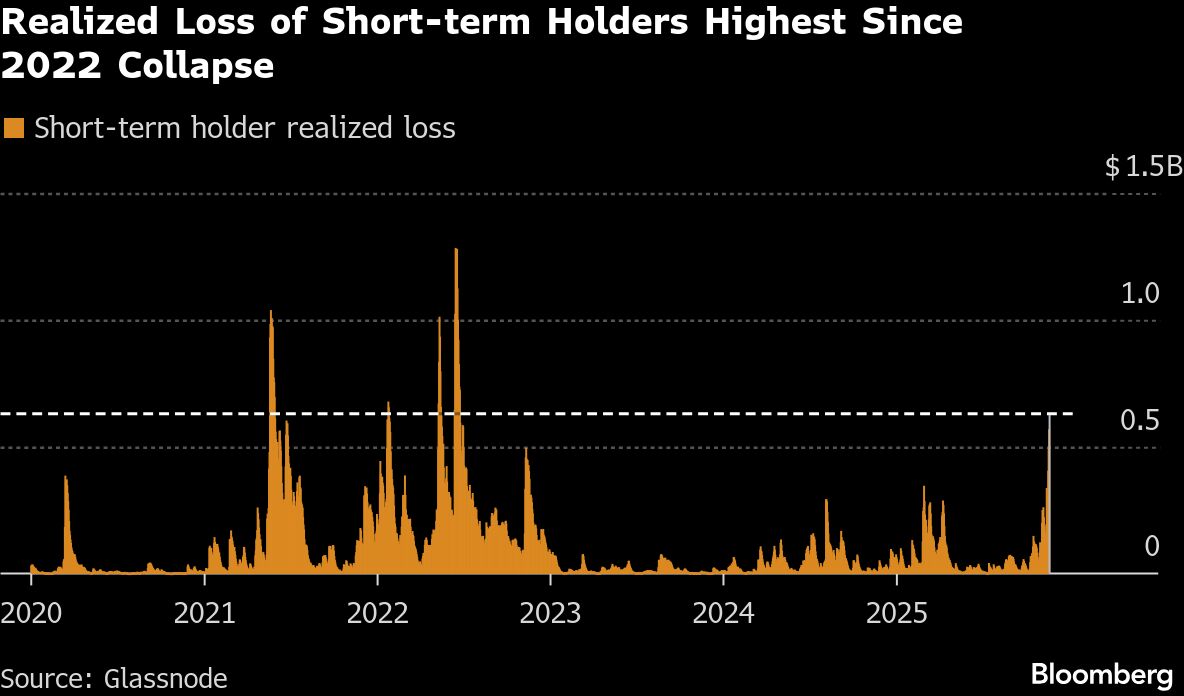

A recovery may also be restrained by the pressure on investors who entered the market at higher levels. Realized losses among short-term holders — wallets that have held Bitcoin for less than 155 days — have climbed to $630 million per day, the highest since the June 2022 meltdown, according to Glassnode.

“Such elevated loss realization highlights the heavier top structure built between $106,000–$118,000, far denser than previous cycle peaks,” analysts at Glassnode said in a research note. “Either stronger demand must emerge to absorb distressed sellers, or the market will require a longer, deeper accumulation phase before regaining equilibrium.”

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.