The degradation and eventual collapse of natural ecosystems could make it harder for countries like India to repay their debt, driving credit rating downgrades and a sharp increase in the cost of borrowings.

That's the crux of research done by a team of economists from British universities, led by academics from the University of Cambridge.

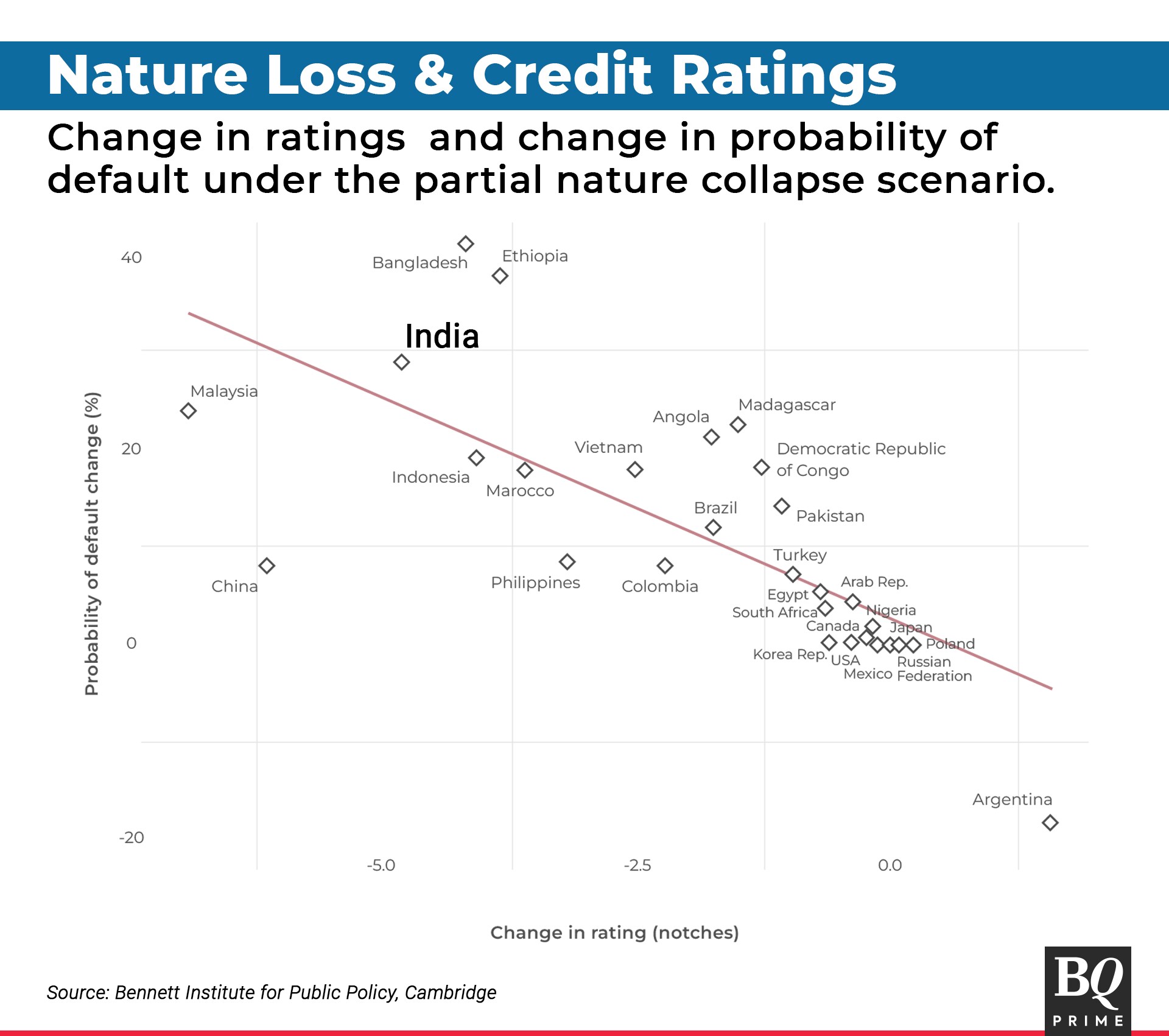

According to the study, in the event of a "partial ecosystem collapse", India's probability of defaulting on sovereign debt repayment will rise 29%. The country may see downgrades up to four notches on a 20-notch rating scale. At the same time, it could add between $5.24-18 billion in annual interest repayments.

Climate change's economic impact has been scientifically established. But this is the first such research that focuses on ecological damage and translates it into the impact on government finances. The researchers make the case that biodiversity loss can do as much economic damage, if not more, than climate change. And they want countries and credit rating agencies to take note.

"Sovereign debt is the thing we run to when there is a crisis," the lead author Matthew Agarwala, economist at Bennett Institute for Public Policy, Cambridge, told BQ Prime in an interview.

"What we are showing is that sovereign debt could actually be a source of a crisis if ecological loss is not addressed."

To be sure, India will not be the only one affected. Nature loss is likely to trigger credit rating downgrades and increase default probability for most countries covered.

Agarwala's team ran simulations using the World Bank's partial nature collapse scenario where there is loss in marine fisheries, widespread conversion of forests to savannas, and fall in wild pollination. The World Bank estimates a $2.7 trillion loss of global GDP in 2030, in such a scenario.

That spells trouble for India. If GDP shrinks, so does the tax revenue. There is less money available for the government to service existing debt and credit downgrades would mean the cost of borrowing new debt is also higher. India already spends nearly half of its revenue towards interest payment on borrowings.

"In order to service this more expensive debt, there are a few things governments will do," said Agarwala. "They can raise taxes. They can cut public spending. Or they can print more money and have some inflation. All three have a direct impact on the incomes of regular people."

And unlike past financial crises, the central tools of monetary policy will not aid in case of nature loss, Agarwala said. "You cannot print more nature. You cannot write-off the loss of rainforests. The dead fish cannot receive a cheque from the IMF," he said. "This is the kind of debt we cannot inflate away."

(Source: Unsplash)

For this reason, the researchers are calling for sovereign credit rating agencies like S&P, Fitch and Moody's to start incorporating the risk of nature loss in their ratings scale.

Agarwala said that most of the credit risk analysis is retrospective, and that needs to change for the risk from biodiversity loss to be properly assessed.

"Climate science clearly tells us the future will not be anything like the past. We are coming up for big changes," he said. "The difference between what we have tried to do and what rating agencies do is the difference between a doctor's diagnosis and a coroner's autopsy."

Agarwala said that it is "wickedly and brutally unfair" that India, whose ecological footprint is significantly smaller than that of Western nations, will not only face the brunt of the biodiversity loss, but also the economic consequences, such as credit downgrades. Much-needed finance for restoring India's ecosystems and mitigating emissions will cost more to borrow.

"There's a lesson to be gleaned from here: the world is unfair and if we don't address the biodiversity crisis, it is going to get a lot more unfair," he said.

"We need stronger conversation on the global forums to deliver finance for conserving biodiversity hotspots in developing countries. That burden shouldn't fall on a rural farmer in Rajasthan."

Edited excerpts from the interview:

Why was it important for you to establish this link between biodiversity loss and credit ratings?

Matthew Agarwala: The reality is that climate science and environmental science, every single week, warn us of new risks that arise from the degradation of ecosystems and the warming of the planet.

If we take science seriously, then there is one group of people on the planet who ought to be best-placed to identify that risk, price it and manage it. And that's financial managers—investment funds, central banks, finance ministries, stock markets.

The problem is that the kinds of risk we convey in scientific papers, related to the economic consequences of say fisheries collapsing or wild pollinators disappearing and their knock-on effects is not translated well into financial metrics. It is not very helpful to me as an investor to know that Brazil's agriculture production may fall over two years. What I want to know is what is the financial risk.

And the standard way of trying to assess this is looking at an individual company, and say that particular one might face a risk. The problem is environment change doesn't hit individual companies alone. It aggregates up, it is a macroeconomic problem. If we only look at granulars, saying this particular company, in this sector, in that country, we can identify some of that and that's important to do. But the macro effect is magnified, it intensifies and grows up. Because there is a ripple effect.

If a farm suffers, then so does the industry that provides the farm with seeds and fertilisers, so does the shipping and transport industry, so does the food processing industry, so does the food servicing industry, so does the household disposable income because food prices rise and there's less money to spend on other things. The macro effect, everything is connected.

We wanted to look at the sovereign effect. The standard way of looking at the sovereign effect will be looking at it historically and assessing how climate change and some biodiversity loss has reduced GDP. And we see that makes it harder for companies to service their debt and there is an effect, either through a downgrade in ratings or an increase in bond yields. They have to pay more to borrow.

But the problem with looking in this way at the world is that it is backwards. We are looking at what happened in the past. That's a risk measure that is only backward-looking. If you only tell me after the fact something happens that it was risky, it doesn't help me make decisions today about going forward.

Everything climate science tells us is that the future will not be like the past. We are coming up for changes. So, relying on the past to simulate the future is not acceptable scientifically. We wanted to look at forward-looking risk assessment, taking in the latest, cutting-edge scientific models.

We are not taking predictions or forecasts, but rather simulations under a range of scenarios. And when we have these simulations, we are able to give a forward-looking risk measure. The difference between what we have tried to do and what rating agencies do is the difference between a doctor's diagnosis and a coroner's autopsy report. And risk analyses are meant to be like doctors and not coroners.

Why does this matter? Why should we care about sovereign debt? It is a long walk to go from Brazilian bees to India's debt position.

Here's the way I describe this: when economies perform poorly, it is more difficult for them to service their debt. When GDP shrinks, so does the tax revenue. When tax revenue shrinks, the money available for governments to service existing debt falls. It also means that it is more expensive to borrow and issue new debt. The market will require a higher interest payment.

In order to service this more expensive debt, there are a few things governments can do: they can raise taxes—that affects regular people. They can cut public spending—and that affects regular people. Or they can print more money and have some inflation—and that, too, affects regular people.

What is different about the kind of debt we are talking about and the kind of debt that has driven crises in the past, is that ecological debt is real debt. You cannot print more nature. You cannot inflate the Amazon rainforest. The dead fish will not receive a cheque from the IMF. The central tools of monetary policy we would use, in order to address a crisis, are not effective against the laws of environmental wealth, of natural capital.

And that's a major concern. This is the kind of debt we cannot inflate away.

Credit rating agencies have been criticised for slow reaction to crisis in the past, and more recently, with the Covid-19 pandemic too. Are they late to the party again?

Matthew Agarwala: In some ways, they are really late to the party. And in other ways, they have shown up at the wrong party.

They've jumped in on the ESG market, which at the moment is not getting them any points. The sovereign credit rating has a clear question behind them, the question it is trying to answer is what is the ability and willingness of this sovereign to service its debt. You might think we are better or worse at answering the question, but at least we know the question.

When it comes to ESG, nobody can tell what the question is. Loads of people have answers. Every ESG rating agency says my answer is better than other answers. What's the question? Nobody knows.

I think it is a problem because there's no clear systematic link between the scientific research that is coming out and ESG measures that we are having now.

With our work, there's a direct link. You can see it from the environmental science to economic modelling to credit rating. And it is so direct and transparent that if you give me a different scientific model that yields different results, I can integrate it instantly into the same.

We've created a tool. What's most important is not just the results but a demonstration that we can integrate scientific information about environmental risk into financial indicators of risks without compromising the science. If we can do it, then why should markets not expect it to be done by other much bigger agencies?

Is there a risk of inconsistent rating outcomes if credit rating agencies start incorporating biodiversity loss in the same way?

Matthew Agarwala: The law in Europe and North America, they require the rating agencies to publish the ratings methodology and make it available. It is not some locked-up proprietary equation.

Their methodology is based on some bits of hard data, which are established facts, some bits of soft data with the analysts' interpretation and communication with the country. Although the method is published, it may not result in everyone getting the same answer. It's a method, not an equation.

What I think is the bigger concern is that the big three are not giving us enough diversity in their risk assessments. They are all telling us the same things and are missing out on the same kinds of risks, in the same way. There's not a lot of depth, diversity, and they all seem to get the same things wrong in the same way systematically.

We need a change in the way we understand with and engage with sovereign debt markets. The rating agencies ought to be part of that but it depends on whether they are really willing to innovate.

If nature loss has an economic impact, then wouldn't this already be baked in to credit ratings to some extent?

Matthew Agarwala: This is what some of the rating agencies claim when we have meetings with them. That we already factor this in, because if climate change affects GDP, that would be a key variable.

Well, okay, but that's still a backward-looking thing. The autopsy report. We are not dead yet, maybe we can still have a diagnosis report.

Because then, what is the rating for? If you wait until after a crash and then they come and say that thing that just crashed, it crashed. Who cares? They're behind the story.

What can you tell me ahead of time? What kind of scenarios can you tell me? What are the risks I am exposed to? How am I gonna ensure that the pensions I am managing aren't exposed to climate or biodiversity loss that we can cover?

Isn't it harsh that developing countries like India, whose natural assets will already be most impacted, will also have to bear the brunt of costly borrowings and the increased risk of default?

Matthew Agarwala: It's bad news. It is wickedly unfair that India with a per capita ecological footprint, which is so much smaller than the U.K. or France or Canada or the U.S., is simultaneously one of the most at risk for heatwaves, floods, droughts, biodiversity loss, and has some of the least adaptive capacity. It is brutally unfair.

And I think there's a lesson to be gleaned here: the world is unfair and if we don't address the biodiversity crisis, it is going to get a lot more unfair.

One of the good things about biodiversity is that it is more locally controlled. Not exclusively locally controlled. Climate change will affect it. But for the most part, the management of ecosystems is quite tightly centered around the physical location of those ecosystems. This means India does have more direct control over the future of its ecological assets. They have more control over their own environment than they do on the global climate. So, India has agency here. It is not just at the whims of the Western world.

India has agency, especially around fisheries, land use or forestation. It is also important for India to push a much stronger conversation about biodiversity loss at global forums. About how we will deliver the finance mechanisms for the developing world, where so many of the biodiversity hotspots reside, to invest in maintaining and protecting them. That burden shouldn't fall on a rural farmer in Rajasthan.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.