Indian non-bank financiers, a favorite among asset managers until recently, have been hit by tighter financing conditions and an erosion of trust, both of which are leading to higher funding costs for the firms and may eventually crimp growth.

A perfect storm of sorts for Non-Bank Financial Companies has rolled in from a number of different directions. On the one hand, tighter liquidity and regulatory concerns may bring down the rapid growth in bank lending to NBFCs. On the other hand, defaults and sharp rating downgrades at Infrastructure Leasing & Financial Services Ltd. have led to a trust deficit.

The result, say analysts, will be slower growth and thinner margins.

The last couple years have been pretty good, said Suresh Ganapathy, head of financial sector research at Macquarie. NBFCs have benefited from the lower cost of funds, which allowed them to grow their balancesheets rapidly, he explained. However, over the last few months, liquidity has tightened and contagion risk from the defaults at IL&FS have slowly spread.

Investors are definitely taking a call when it comes to subscribing to relatively low-quality papers. There is a lack of trust or trust-deficit. Sometimes, that can cause a lot of problems and that is what we're currently seeing in the markets.Suresh Ganapathy, Head - Financial Sector Research, Macquarie

Wholesale Funding Squeeze

The most immediate concern for NBFCs emerges from the change in conditions in the debt markets. Tighter liquidity conditions, where the system is short of nearly Rs 1 lakh crore, have driven up rates across the board.

The increase in rates for shorter tenor corporate borrowings have risen notably over the last few weeks. Rates on short term 91-day treasury bills have moved above 7 percent, pushing up rates for corporate bonds as well.

")

In addition, the spreads charged for lower rated borrowers have also widened.

According to a CLSA report, the yield on 1-year A-rated corporate bonds has moved up from 8.7 percent to 10.7 percent between September 2017 and September 2018. The yield on BBB-rated corporate paper has risen from 9.9 percent to 11.9 percent over this twelve month period. Meanwhile, the yield on AAA-rated corporate paper has risen from 6.9 percent to 8.6 percent.

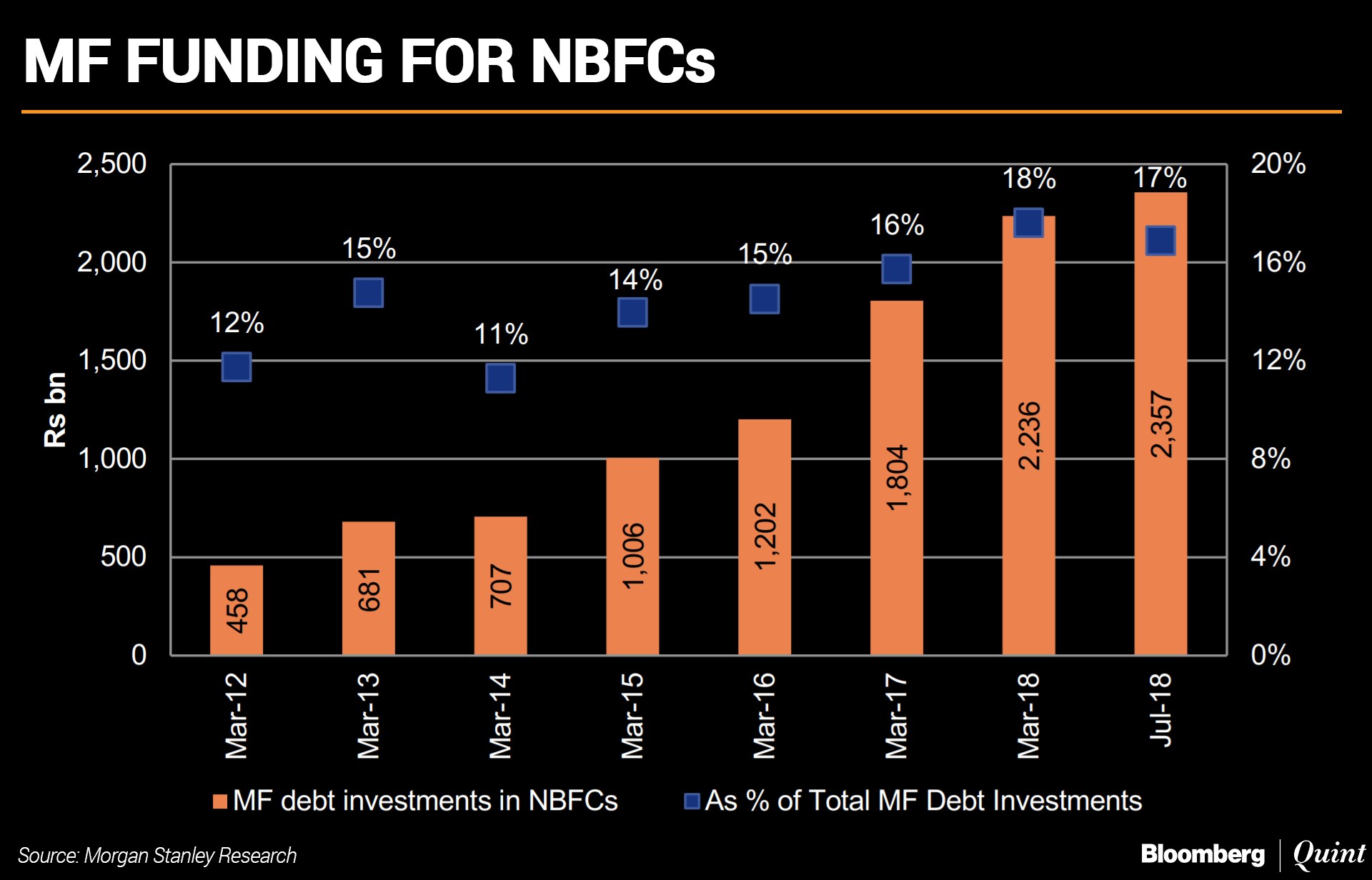

Apart from the cost of funding, the supply of funding in the wholesale market is also expected to reduce. “A significant source of funding to NBFCs in recent years has been mutual funds, which has almost doubled in the last two years. This is likely to slow,” said Morgan Stanley in a report on Monday.

According to data from the research house, mutual fund investment in debt securities of NBFCs stood at Rs 23,570 crore as of June 2018. This was 17 percent of the total debt investment by mutual funds.

Morgan Stanley does not believe that wholesale funding for NBFCs has dried up, but acknowledges that volumes in the corporate bond market have fallen due to higher costs. For the first time since 2014, corporate bond issuances are negative for the quarter ended June 2018, the Morgan Stanley report noted.

CLSA, however, felt that availability of funds will also be a challenge, atleast for lower rated NBFCs. “A potential risk aversion among investors in debt funds (retail/corporate) can result in investors preferring quality over yields for their debt funds,” said CLSA in its report on Sunday. “This along with rising risk aversion by asset managers may lead to market shifting only towards best rated paper.”

Slower Bank Funding

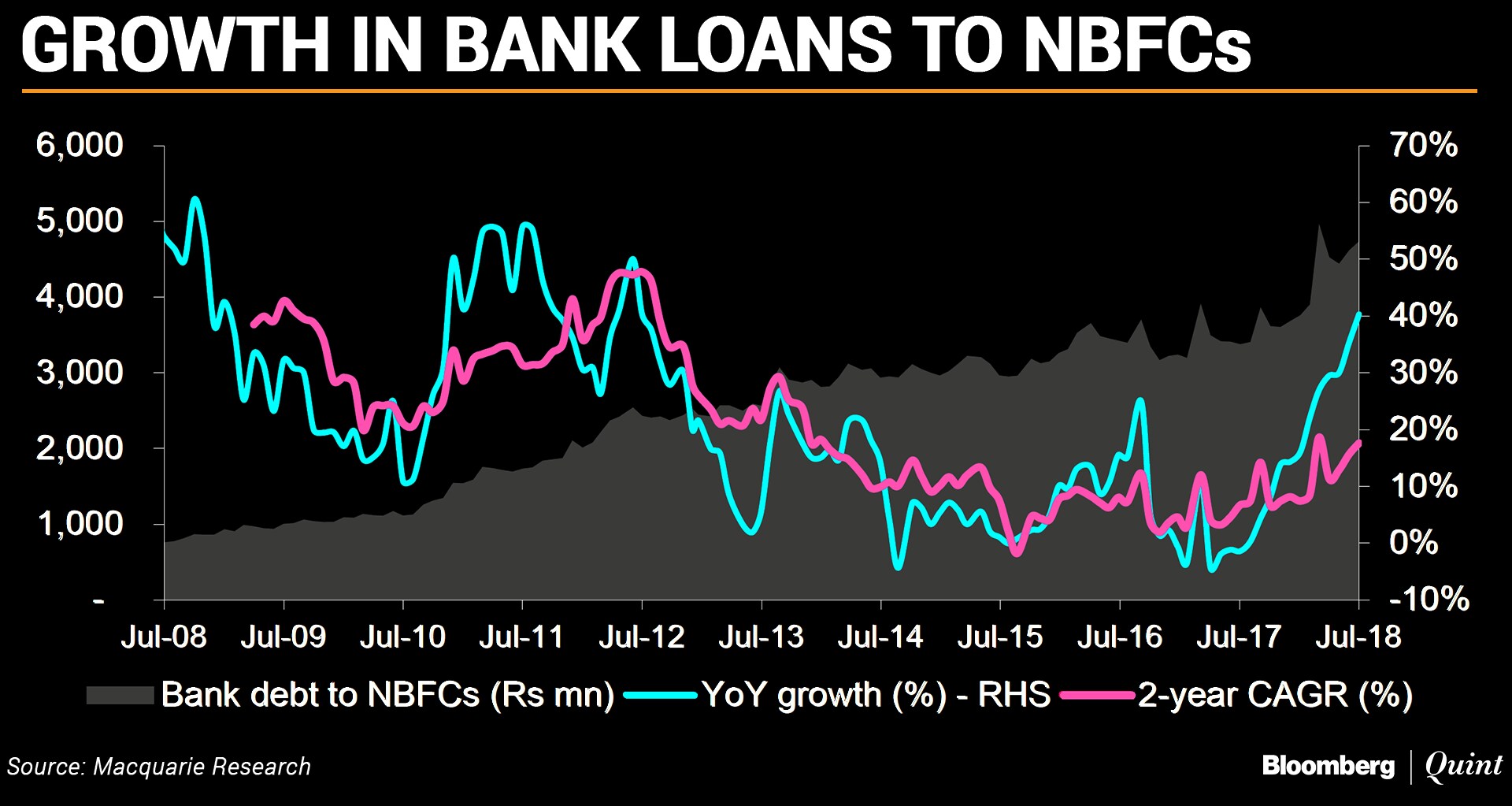

The problem is being compounded by concerns that banks will go slow on lending to NBFCs. Liquidity conditions have tightened and the regulator is believed to have frowned upon the rapid growth in bank lending to these firms over the last one year.

Data from Macquarie shows that bank lending to NBFCs has been growing at a rate well above the 2-year compounded annual growth rate in recent months. This has helped NBFCs grow their aggregate loan book to Rs. 24.1 lakh crore at the end of fiscal year 2018 from Rs. 15 lakh crore at the end of fiscal year ended 2015.

According to Macquarie, their interactions with NBFCs and housing finance firms suggests that the RBI has asked banks to review their exposures to these companies.

If bank debt also becomes costly/unavailable, then it may ruin the investment case for most NBFCs dependant on wholesale borrowings.Macquarie Research

Most NBFCs may be unable to raise deposits from the public in times of a crunch, said Macquarie. If mutual funds see redemption pressure , it could further add to liquidity tightness and make NBFC access to short term liquidity very difficult, it added.

No Cause For Panic, Says Industry

In a conversation with BloombergQuint on Monday, SBI chairman Rajnish Kumar denied that there was any freeze in bank funding to NBFCs. He, however, acknowledged that growth rates in lending to NBFCs could moderate due to changing liquidity conditions.

The pace at which NBFCs were growing may see some moderation now, added Raman Aggarwal, chairman of the Finance Industry Development Council, a self regulatory organisation for NBFCs. However, there is no significant cause for concern for several reasons, he adds.

In 1997, the RBI had mandated all NBFCs to create a separate reserve fund, with not less than 20 percent of their profits. This has helped the sector maintain an inherently strong balance sheet, says Aggarwal. He adds that even stress tests conducted by the RBI showed that NBFCs managed to retain capital adequacy of over 20 percent as opposed to a requirement of 15 percent.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.