The Reserve Bank of India's prompt corrective action framework for non-bank finance companies is unlikely to hurt major lenders but may weigh on capital and growth of smaller NBFCs and microfinance companies.

The banking regulator has released a new framework intended to take early action against weakness building across NBFCs. The framework will kick-in starting October 2022, based on March 2022 financials. Just like in the case of banks, risk thresholds have been laid down and NBFCs breaching these will face restrictions till the institutions course-correct.

Only a handful of large non-bank lenders are currently in breach of the triggers laid down by the RBI. To be sure, the financials of these lenders and others may vary by March 2022.

In a report on Wednesday, Phillip Capital said that none of the major NBFCs under its coverage, with the exception of Mahindra & Mahindra Financial Services Ltd., will be impacted by the guidelines.

M&M Financial Services has a net non-performing asset ratio of 6.4% which is higher than the RBI's risk threshold of 6%. Analysts at Motilal Oswal believe that M&M Financial Services intends to bring down its net NPA ratio to below 4% by March 2022.

According to an assessment by ICRA Ltd., at least three large NBFCs, with an asset size of over Rs 25,000 crore will be in breach of the RBI's net bad loan threshold. The rating agency did not specify the names of these companies.

As per publicly available data, Tata Motors Finance Ltd., which had an asset size of over Rs 33,000 crore at the end of the second quarter, reported a net NPA ratio of 7.03%. Hero FinCorp Ltd., with an asset size of Rs 26,817 crore, reported a net NPA ratio of 6.16%, as of Sept. 30.

Queries were sent to M&M Finance, Tata Motors Finance and Hero FinCorp on Wednesday to ask whether these companies will step up provisions to reduce their net NPA numbers. Replies are awaited.

The new norms are applicable to all deposit taking NBFCs and non-deposit taking NBFCs which fall under the middle, top and upper layer, according to the RBI's classification. The middle layer consists of NBFCs with an asset size of Rs 1,000 crore and above, while the upper layer consists of at least the top 10 NBFCs. The top layer is kept empty for now, as per the regulatory guidelines.

NBFCs not accepting or not intending to accept public funds, government companies, primary dealers and housing finance companies will be exempt from the framework.

Smaller NBFCs, MFIs May Face The Heat

The new framework may pose a challenge for smaller NBFCs which fall in the middle layer, and microfinance companies. This, as the RBI has recently tightened bad loan recognition rules as well.

On November 12, the regulator tightened asset classification norms and said that all lenders must mark NPA and other defaulting loans through a day-end reconciliation process as opposed to a month-end rule that was currently being followed. This is likely to push up reported bad loans of NBFCs.

Coming atop that, the corrective action rules may be a challenge.

According to Raman Aggarwal, area chair-NBFCs at Council for International Economic Understanding, there are about 150-200 lenders which will qualify for the middle layer classification. The RBI's net NPA threshold combined with the recognition norms are the biggest threat for this group, he said.

"You have to see this from the customer's point of view too. Small businesses opt for NBFC financing because it is more flexible than a bank loan. Tighter recognition will impact this customer base," Aggarwal said.

Currently, most mid-level NBFCs review their books once a month and mark accounts in default. A daily recognition cycle will lead to more accounts becoming NPA. Once they are tagged as NPA, the borrowers will be unable to secure any other financing, which will effectively show up on the lender's balance sheet and they would face regulatory action, he said.

The challenges for micro lenders may be even more acute. Many of them see sudden spikes in bad loans due to events such as floods, droughts and political interventions like farm loan waivers. A stringent corrective action rule could lead to business restrictions even on account of such events.

"There are about 15 microfinance companies which would be subjected to the thresholds of PCA. On their own, these entities have maintained strong asset quality and are well provided for. However, with the RBI's new asset classification norms, some may suffer," said P Satish, executive director, Sa-dhan, a microfinance industry body.

Satish, however, added that companies which do go under restrictions may be able to use the time to improve their businesses.

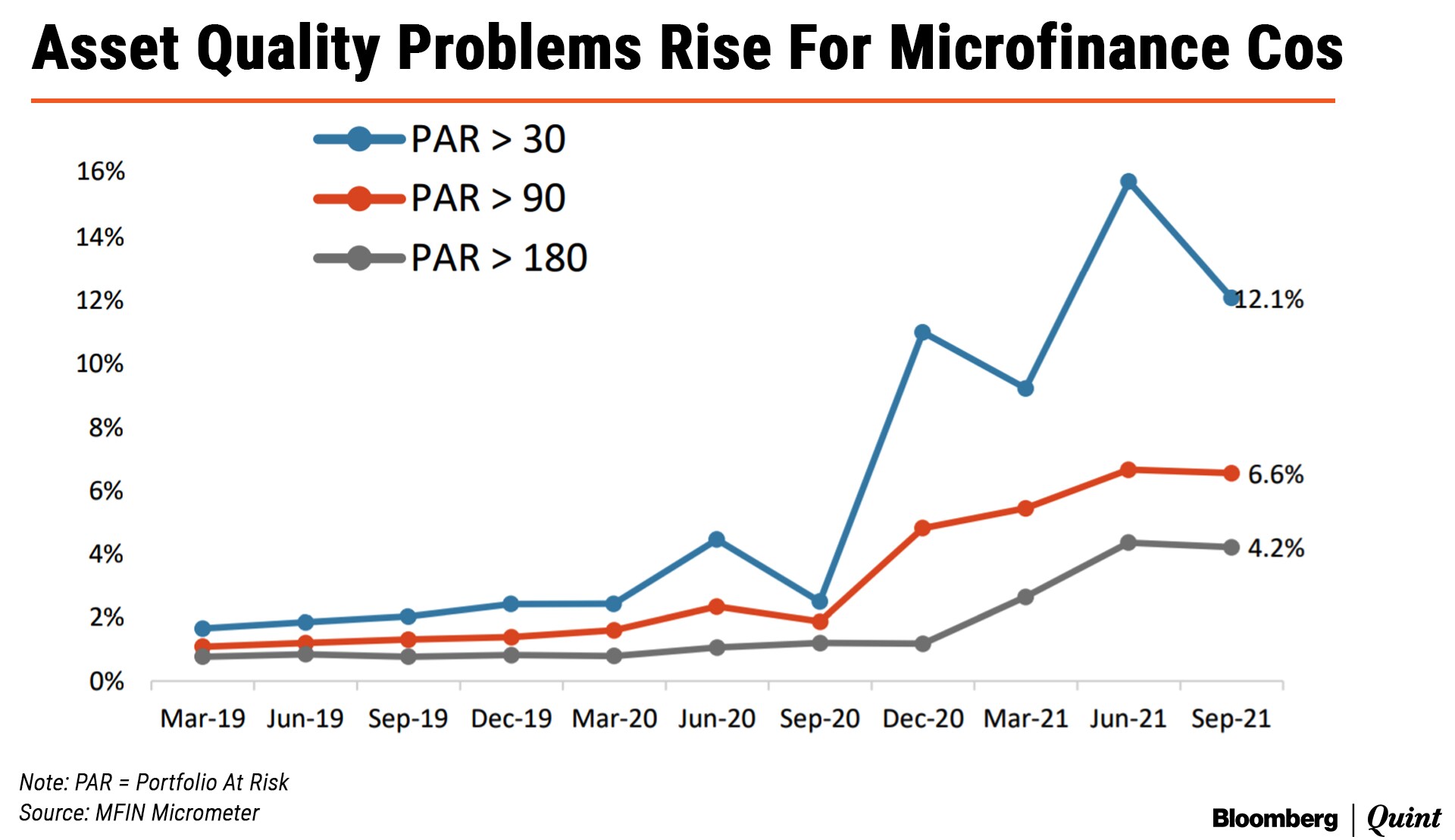

According to data released by Microfinance Institutions Network on Wednesday, in case of NBFC-MFIs, the portfolio in default for more than 30 days had risen to 12.1% as of Sept. 30, compared with 2.5% a year ago. The portfolio in default for over 90 days stood at 6.6% for this segment. MFIN reviews self-reported data from 55 NBFC-MFIs.

Correct In-Principle

While the regulator has introduced scale-based regulation for non-bank lenders, its corrective action framework does not make the distinction between large and small lenders.

According to Ashvin Parekh, managing partner, Ashvin Parekh Advisory Services, the size of the governed entity should not matter, when talking about stability. The ratios prescribed by the regulator are applicable to each NBFC, irrespective of its size.

"Effectively these guidelines talk about the financial stability of the entity. If the entity is unable to adequately provide for bad loans, it goes to the solvency question. And if solvency is in question, the entity would be able to repair its financial position in a corrective action framework," Parekh said.

Especially since smaller NBFCs depend on bank financing, they are also agents of public money. So they have a responsibility to maintain strong controls over their solvency, Parekh said.

In case of microfinance companies, there are evergreening concerns at the grassroot level, which can be addressed through the tighter recognition norms prescribed by the RBI, Parekh said. "If microfinance companies are resorting to evergreening to appear financially stable, then a corrective framework would be a good for the industry," Parekh said.

Alok Prasad, a senior banker and veteran of the microfinance industry, says that the corrective action framework should be seen as a way for the regulator to control potential systemic risks in the sector.

"The regulator has just added one more weapon to its armoury, only to be used when absolutely necessary. The RBI will adopt objective parameters for its use, as has been the case for banks," Prasad said.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.