On Monday, the Reserve Bank of India announced a Rs 50,000 crore liquidity facility for mutual funds.

The announcement came amid fears that redemption pressure will force funds to sell debt securities at large discounts. The RBI was willing to step in and offer a temporary liquidity facility which would stall such fire sales. But given that the central bank lends directly only to banks, the liquidity was offered to mutual funds via the banks.

Immediately, questions emerged if banks, deeply risk averse amid a weakening economy, will channel the relief to mutual funds. “I don't see them taking lower-rated corporate debt as collateral, which has been lacking in liquidity,” Arvind Chari, head of fixed income at Quantum Advisers, said in a note.

The second round of targeted long term repo operation designed to provide relief to non-bank lenders had already failed to see the pick-up for precisely that reason. And the first such long term funding facility had mostly been invested in top rated corporate and public sector names.

As such, the concerns that reluctant lenders will stall relief to those who may need it, in this case mutual funds, was valid. But so is the risk aversion among lenders.

Burdened with an already elevated level of bad loans—a legacy of imprudent lending nearly a decade ago—banks are not willing to take the risk of a further deterioration in asset quality. Some increase in bad loans is inevitable given the weakness in the economy and lenders are trying to keep this in check.

“You can beat them (banks) on the head to lend now or you can beat them on the head with a bigger stick 10 years later for the NPAs. My sense is that the central bank should respond on liquidity and not on solvency,” Manish Sabharwal, who sits on the RBI's central board, said in an interview as part of a broader conversation.

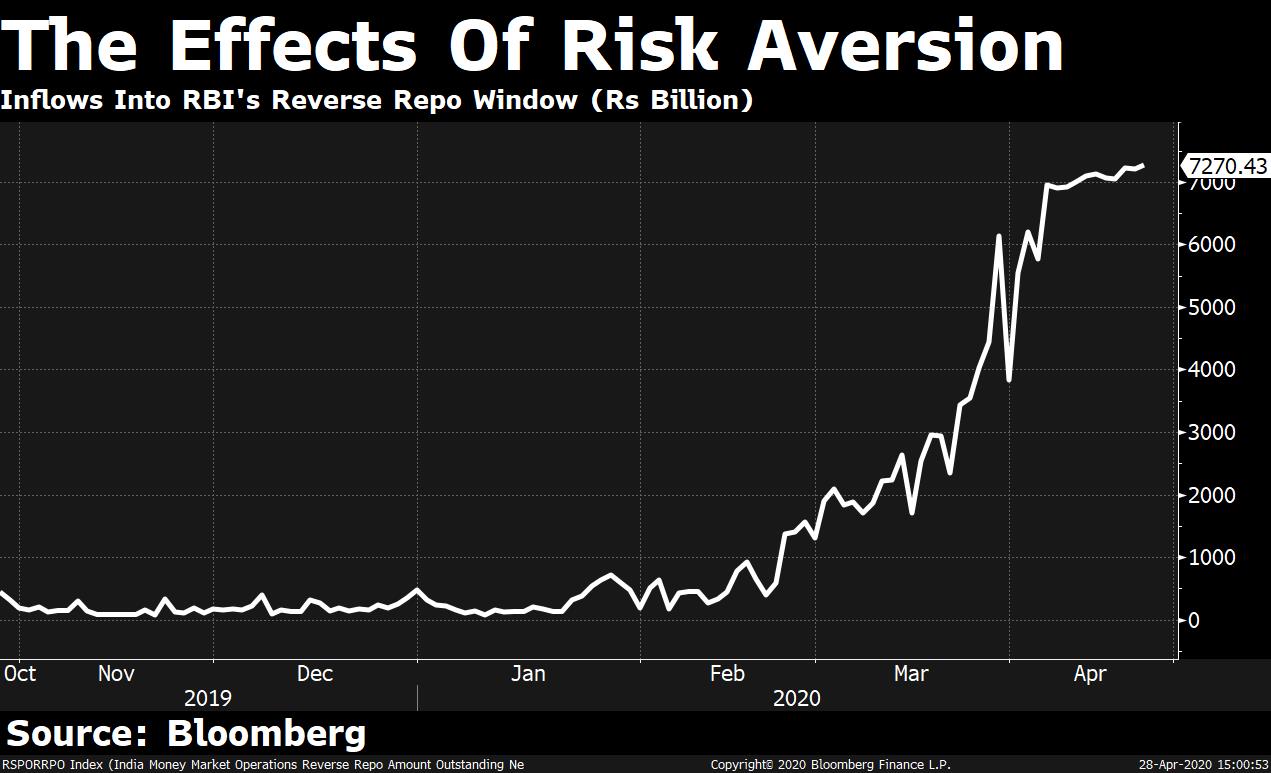

The extent of risk aversion seen across banks is perhaps best encapsulated in this one data point.

So much so, that the RBI may now need to a open a new window, known as the Standing Deposit Facility, through which is accepts excess bank reserves at much lower rates without offering collateral in return.

The Bankers' Perspective

Four senior bankers, who spoke to BloombergQuint on conditions of anonymity, said it is unfair to expect banks to do the heavy lifting at a time like this.

A senior banker from State Bank of India said that more than lenders, there is risk aversion among borrowers, who prefer to stay away from large borrowings at this time. Transmission requires a lender and a borrower, he said.

Speaking specifically about the mutual fund liquidity window, this banker said that funds are preferring to sell their holdings rather than using them as collateral to raise liquidity. This shows that there was an issue with underwriting and the risk was not priced in adequately. Banks will pick up such paper only selectively and you wont see massive purchases, this banker said.

According to the chief executive of a large public sector bank, the banking system is currently flush with liquidity but low-risk avenues for investment and lending are limited. This has prompted bankers to adopt a wait-and-watch approach.

Banks have to take considerable credit risk while lending in a highly uncertain economy, the public sector banker said. Given the experience of the last lending cycle, bankers have become more cautious in the current cycle, this banker said.

As per the RBI's December 2019 Financial Stability Report, gross NPAs for banks stood at 9.3 percent of total assets in September 2019. They could rise to 10.5 percent in a ‘severe stress' scenario where GDP growth falls to 3 percent. The Covid-19 crisis could, however, lead to a contraction in the Indian economy, some economists fear. This would mean that bad loans could rise even further.

In fear of this, banks have tightened lending standards across the board.

Take, for instance, the widely-criticised decision by some banks to not extend an RBI-permitted moratorium to NBFCs. According to the head of wholesale lending at a private sector bank, the decision was taken to avoid the contagion risk within the financial system. The banker spoke on condition of anonymity.

Similarly, when the RBI offered Rs 50,000 crore in liquidity to NBFCs, with half of it reserved for smaller NBFCs and microfinance institutions, banks only picked up half of the funds on offer.

“That the banks bid only for 50 percent of the Rs 50,000 crore on offer by RBI at a 3-year attractive rate of 4.4 percent under the repo window indicates that credit risk is the biggest issue. Despite attractive borrowing rates (incremental 3-year term deposit rates are at 7 percent), banks are unwilling to borrow and lend to NBFCs,” Macquarie analyst Suresh Ganapathy said in a report on April 24.

Also Read: Structural Changes Needed In Mutual Funds And Credit Markets

Breaking The Cycle

While the reasons behind the risk aversion may be justified, so are concerns that reluctant lenders could hamper the flow of relief to the economy.

How then does the central bank overcome this problem?

Bankers suggest a few options.

A former chairman of State Bank of India said that government could take on some of the credit risk associated with loans given out during this time. This person also suggested that the government could provide equity support to some key industries. A special purpose vehicle, like the Specified Undertaking Of The Unit Trust of India, or SUUTI, could be used to hold equity of companies to which the government provides emergency loans.

By recapitalising these entities, the government would reduce the risk in lending to them.

The private sector banker quoted above said that providing additional capital, particularly to government-owned banks, could be another way to ease risk aversion. At this time, with banks fearing increased defaults most banks have moved into capital conservation mode.

The RBI could also widen the securities it accepts as collateral at its repo window.

"Given the asymmetric distribution of liquidity across the financial system, and heightened risk aversion on the part of banks—evident in the TLTROs—perhaps the next step would be for the RBI to consider broadening its repo operations to accept corporate paper—financial and non-financial—with appropriate haircuts to reflect the credit risk,” said Sajjid Chinoy, chief India economist at JPMorgan. This would ensure that parts of the system that need liquidity, but cannot get it through banks, would have means to access liquidity.

In the case of small businesses, because SME balance sheets are likely to be hit, a risk-averse banking system may not be willing to lend to them. A partial loan-guarantee may therefore be important to incentivise and back-stop bank lending to SMEs, Chinoy said. “The RBI has thus far been very proactive, and emerging market central banks will have to keep innovating as the shock unfolds,” he added.

Also Read: India Considers Proposal to Guarantee $39 Billion of Small-Business Loans

RBI Governor Shaktikanta Das, in an interview to Cogencis this week, acknowledged the problem but stopped short of offering a solution.

Responding to a question on the weak response to the targeted repo operations directed at NBFCs, Das said the auction results convey a telling message “which is that banks are not willing to take on credit risk in their balance sheets beyond a point.”

“We are reviewing the whole situation and based on that, we would decide on our approach,” Das told Cogencis.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.