The Reserve Bank of India has decided to permit a one-time restructuring of loans, amid the ongoing Covid crisis which is hitting businesses hard.

Announcing a review on monetary and credit policies on Thursday, RBI Governor Shaktikanta Das said a window under the June 7 stressed asset resolution framework will be provided which will enable lenders to implement a resolution plan, without a change in ownership.

“...it has been decided to provide a window under the June 7th Prudential Framework to enable lenders to implement a resolution plan in respect of eligible corporate exposures - without change in ownership - as well as personal loans, while classifying such exposures as standard assets, subject to specified conditions,” RBI Governor Shaktikanta Das said in his statement on Thursday.

In addition to the provision for restructuring of large corporate loans and personal advances, stressed MSME borrowers will also be allowed to restructure their debt provided they were classified as standard on March 31, 2020. This window will be available till March 2021.

Watch this conversation on the restructuring scheme with Abizer Diwanji of EY

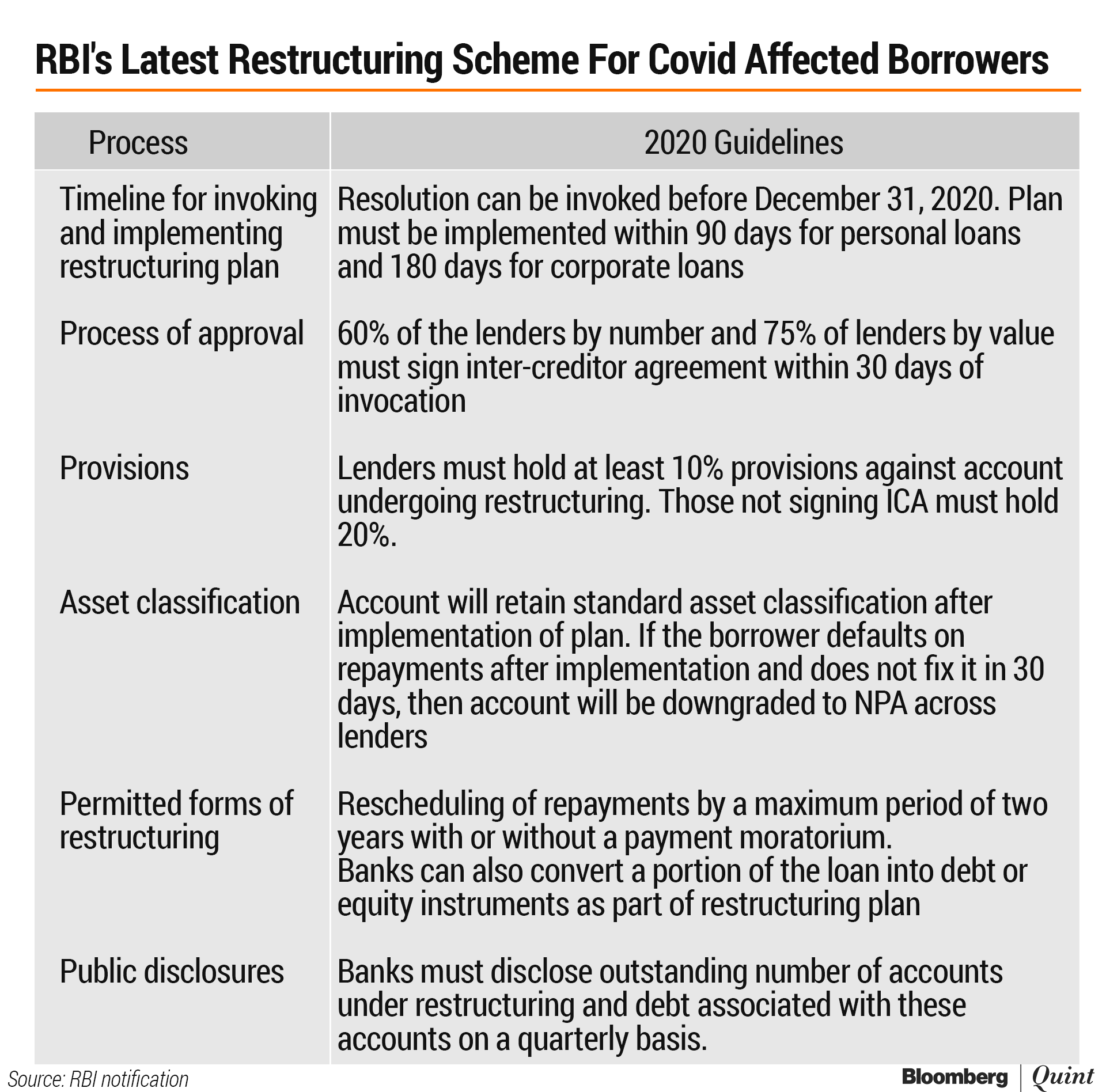

What Restructuring 2.0 Will Look Like?

According to the RBI, lenders must ensure that this restructuring scheme is only available to borrowers which are facing stress on account of Covid-19. The framework shall not be available for exposures to financial sector entities as well as central and state governments, local government bodies and any body corporate established by an act of parliament or state legislature.

Eligibility Criteria

- Accounts which were in default for not more than 30 days as of March 1 will be eligible for such restructuring. All other stressed accounts will have to follow June 2019 framework for resolution.

- A committee headed by KV Kamath will be set up make recommendations to the RBI on the required financial parameters, along with the sector specific benchmarks to be factored into each resolution plans.

- This committee will also validate the resolution plans for accounts with cumulative debt of Rs 1,500 crore and above.

- The committee shall check and verify that all the processes have been followed by the parties concerned as desired without interfering with the commercial judgments exercised by the lenders.

- For cases where the aggregate debt is over Rs 100 crore, the lending institutions will have to obtain an independent credit evaluation for the resolution plan from a recognised credit rating agency.

Timeline & Process For Restructuring

- One-time restructuring plan may be invoked any time before December 31, 2020 and must be implemented within 180 days of invocation.

- Lending institutions are required to sign an inter-creditor agreement ahead of the restructuring. Lenders who do not sign inter-creditor agreements within 30 days of invocation of resolution plan shall attract 20% provisions.

- In a multiple banking or consortium lending arrangement, if 60% of the lenders by number and 75% by value do not sign the ICA, then the invocation would be considered as lapsed. The one time restructuring scheme can then not be invoked for such cases again.

- Lending institutions may allow for extension of the residual tenor of the loan, with or without payment moratorium, by a period not more than two years.

- In cases where a loan is converted into other instruments, such debt instruments with terms similar to the loan, shall be counted as part of the post-resolution debt.

- Conversion to any other non-equity instrument will lead to the value of that portion of debt being written down to Re 1.

- In cases where there are multiple banking or consortium banking arrangement, all disbursements made to the borrowers by the banks and payments made by the borrowers to banks shall be routed through an escrow account maintained with one of the lending institutions.

Asset Classification & Provisions

- The account will continue to retain standard asset classification after implementation of the plan.

- Lenders shall have to keep additional 10% provisions against post resolution debt.

Monitoring

The RBI has prescribed a clear monitoring period for accounts which are restructured under this scheme. This period begins from the date of implementation till the point in time when the borrower pays back at least 10% of the residual debt.

- In case a borrower is in default with any of the lending institutions during the monitoring period, a review period of 30 days gets triggered. If the default is not resolved within this review period, the account is classified as NPA by all lenders involved.

- Lenders can write back half of the provisions held against restructured accounts after the borrower pays back at least 20% of the residual debt. The remainder of the provisions can be written back after another 10% of the residual debt is repaid, without the account slipping into NPA.

Disclosures

- Banks will be required to publish disclosures with respect to the number of accounts where a one time-restructuring plan is implemented and the outstanding loans to such accounts, on a quarterly basis starting March 31, 2021.

- They will also be required to disclose the quantum of loans which were classified as standard after the restructuring plan, but later slipped to NPA during the monitoring period, on a half yearly basis starting September 30, 2021.

- A disclosure format has been prescribed by the RBI

Restructuring Allowed For Retail Loans

As part of its announcements, the regulator said that a one-time restructuring scheme shall also be applicable for personal loans. The framework for restructuring such loans which have been impacted by Covid-19 shall be as described here:

- All loans extended by lending institutions to individual borrowers shall be covered under this framework. Lenders will not be allowed to restructure loans they have granted to their own personnel or staff, under this framework.

- Accounts classified as standard and not in default for more than 30 days as on March 1 shall be eligible for restructuring.

- The invocation of the resolution plan can be done at any time before December 31, 2020 and will have to be implemented within 90 days of such an invocation.

- Lending institutions may allow rescheduling of payments, conversion of any interest accrued, or to be accrued, into another credit facility, or, granting of moratorium, based on an assessment of income streams of the borrower, subject to a maximum of two years.

SME Loan Restructuring

The RBI also permitted a one-time restructuring scheme for micro, small and medium enterprise accounts. Such a scheme would only be applicable to MSMEs with outstanding debt worth up to Rs 25 crore.

The regulator said that restructuring plans for such MSMEs will have to be implemented before March 31, 2021. For accounts which are restructured under these guidelines, banks will have to set aside additional provisions worth 5%, over and above what they already hold.

The one time restructuring scheme was originally announced in January 2019 and then extended again in February 2020. The regulator said that the guidelines are being extended further to provided additional support to MSMEs owing to Covid-19 and to harmonise restructuring guidelines across borrower categories.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.