Life for several small and marginal farmers in India has come full circle. After having their loans waived by way of an amnesty scheme in 2008, they now find themselves in need of aid once more. Evidence from the 2008 loan waiver, however, suggests that any immediate relief from such a scheme may do little to help over the medium term.

The debate over a farm loan waiver has resurfaced after the Bhartiya Janata Party's (BJP) landslide victory in the recently concluded Uttar Pradesh assembly elections. During the election campaign, Prime Minister Narendra Modi had promised that farmers' loans would be waived if the BJP came to power in the state. Under pressure from Opposition parties, Maharashtra Chief Minister Devendra Fadnavis has also said he is willing to discuss a waiver of farm loans in the state.

The last nation-wide farm loan waiver scheme was launched by the Congress-led United Progressive Alliance government a year before the general elections in 2009. Under the scheme, called the Agricultural Debt Waiver and Debt Relief Scheme, the government waived off more than Rs 52,000 crore in loans held by 3.45 crore farmers, the Comptroller and Auditor General of India (CAG) said in a report released in August 2015.

The scheme was jointly managed by the Reserve Bank of India (RBI) and the National Bank for Agriculture and Rural Development (NABARD).

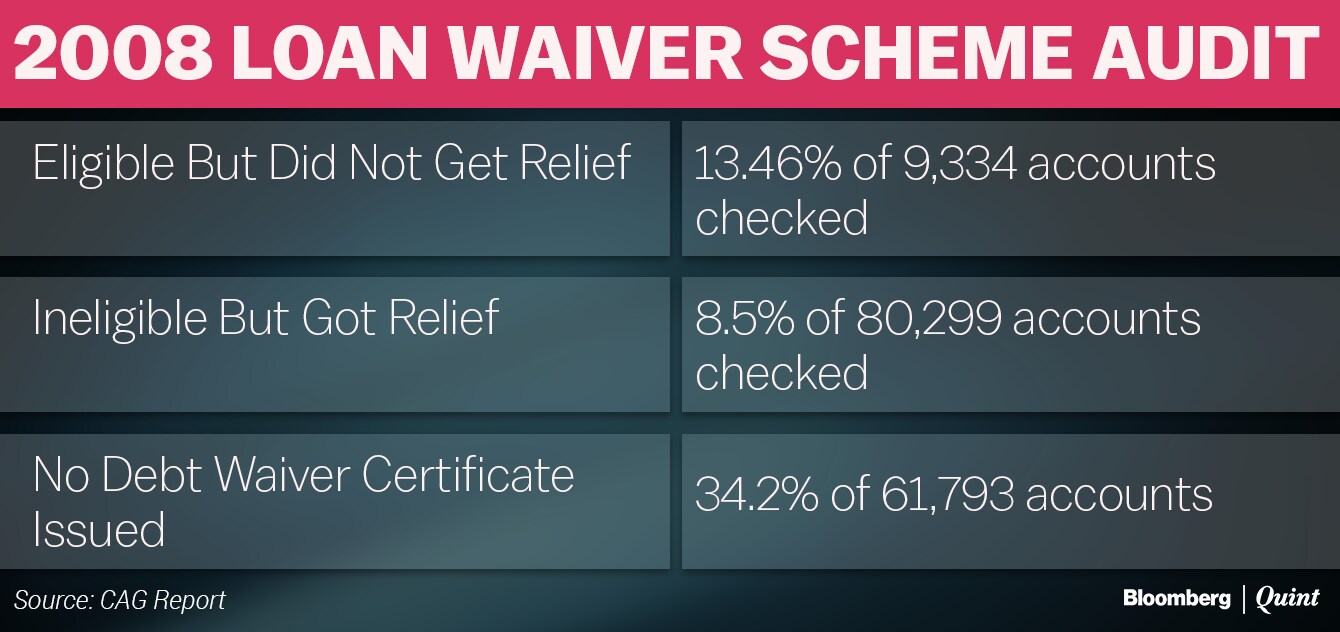

The CAG's audit of the scheme, which was conducted across 90,576 bank accounts in 25 states, found several lacunae.

The audit found that 13.5 percent of 9,334 accounts that were test checked were eligible for the waiver but were not included in the scheme. It also found that 8.5 percent of 80,299 accounts were ineligible for the waiver, but got the benefit anyway.

Further, in several cases, the CAG found that debt waiver certificates, which would entitle farmers to secure fresh loans, were not issued. “In 21,182 accounts (out of 61,793 checked accounts), i.e. 34.28 percent, there was no acknowledgement from farmers or any other proof of debt waiver or debt relief certificates to the beneficiaries,” the CAG said in its report.

N Srinivasan, who was chief general manager at NABARD when the 2008 scheme was conducted, said the scheme had not been designed well. In an article published by the College of Agricultural Banking in 2008, Srinivasan had pointed out that the waiver failed “the test of equity by a large margin”. He sticks by that analysis even today. In a phone conversation with BloombergQuint, Srinivasan said the design of a loan waiver scheme leaves a number of aspects unaddressed.

The waiver does not take into account the loans farmers have taken from the informal sector. There is also no distinction between voluntary and involuntary defaults, so it actually rewards those that have willfully defaulted. Additionally, the scheme does not take into account climatic conditions and fertility of soil. Farmers in certain areas face a higher risk of crop loss on account of weather conditions.N Srinivasan, Former Chief General Manager, NABARD

Unintended Consequences

Bankers have already weighed in on the ongoing debate, saying that farm loan waivers are an ineffective way of providing relief to farmers. They believe that waiving loans has a negative effect on credit culture.

Last week, Arundhati Bhattacharya, Chairman of State Bank of India, the country's largest bank, said, “We feel that in case of a waiver there is always a fall in credit discipline because the people that get the waiver have expectations of future waivers as well. As such, future loans given often remain unpaid.”

Also Read: Breach Of Privilege Notice Against SBI Chief For Farm Loan Waiver Remarks

According to RK Gupta, executive director at Bank of Maharashtra, loan waivers tend to impact credit discipline adversely even for borrowers who have the ability to pay. The bank focuses on lending to the state of Maharashtra, which has seen considerable agrarian stress across the drought-prone region of Vidarbha.

The farmers who were paying regular instalments stopped paying to the banks. They said, why should we be penalised for paying regularly?RK Gupta, Executive Director, Bank of Maharashtra

Poor credit discipline, in turn, makes banks reluctant to sanction fresh loans.

Srinivasan said that after the 2008 loan waiver, there was anecdotal evidence of a decline in lending to certain pockets. This, he said, is likely to happen again despite the RBI's mandate to lend to the agricultural sector as part of priority sector lending targets.

“For two-three years after waivers, there will be a lot of pushback from banks. They will find several reasons why they cannot lend,” he added.

A Band-Aid Approach

Srinivasan is of the opinion that a loan waiver is like a salve which attempts to cure a deep-rooted disease. Fiddling with the financial sector to cure real sector problems, like distress in the farm sector, is not advisable, he said.

“The rates of return, the profitability, the input-output ratio, they are all loaded against the farmer in several crops. So if he borrows money at interest and then applies it for production, he is likely to lose money once in five, six, or seven year cycle depending on the level of irrigation and soil fertility,” said Srinivasan.

Additionally, with farm credit having increased exponentially over the past five years, the quantum of loans that will need to be waived could be significantly higher than in 2008. Srinivasan believes this number could be as high as Rs 1.5 lakh crore. In Uttar Pradesh alone, the amount to be waived off could add up to about Rs 27,420 crore if the scheme is implemented for small and marginal farmers across all banks, said State Bank of India's Economic Research Department in a report on Monday.

Also Read: Maharashtra Budget Focused On Farm Sector But Stays Away From Loan Waiver

There are other ways to provide relief to farmers.

Banks are already offering relief to farmers on a case by case basis by way of rescheduling and restructuring of loans, said Gupta of Bank of Maharashtra.

Another alternative to a nationwide loan amnesty programme could be the launch of an insurance scheme as a social welfare project. The payout of this scheme would not cover revenue loss on account of crop damage but would provide subsistence in the event of crop loss.

“Compensation can't be related to crop damage. If there is a crop failure, that year there needs to be subsistence income. The farmer knows that if crops fail, his life is not affected. What he is losing is profit. If two years out of seven he loses his crop, he is guaranteed that his life is not in danger,” said Srinivasan.

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.