Moody's Investors Service has downgraded India's sovereign rating by one notch citing concerns about a prolonged period of slow growth. While the Covid-19 pandemic has worsened economic conditions in India, it is not the sole cause for the downgrade, Moody's said in its release, adding that the outlook on India's rating remains negative.

Moody's Investors Service had the highest rating on India, having upgraded it in 2017. Fitch Ratings and Standard and Poor's rate India one notch below Moody's.

Following the review, Moody's rating on India stands revised to Baa3 from Baa2, with a negative outlook. It still remains investment grade.

The decision to downgrade India's ratings reflects Moody's view that the country's policymaking institutions will be challenged in enacting and implementing policies which effectively mitigate the risks of a sustained period of relatively low growth, significant further deterioration in the general government fiscal position and stress in the financial sector.Moody's Investors Service

Real GDP To Contract By 4% In FY21

The rating agency said the decision to downgrade has been taken in the context of the coronavirus pandemic, but was not driven by it. “Rather, the pandemic amplifies vulnerabilities in India's credit profile that were present and building prior to the shock, and which motivated the assignment of a negative outlook last year.”

The Indian economy is seen contracting in FY21 due to the impact of the Covid-19 virus on the economy.

Moody's said it sees real GDP in India fall by 4 percent this financial year. It added that growth had been slowing even before the pandemic and may remain significantly below potential for the foreseeable future.

India's real GDP growth has declined from a high of 8.3% in fiscal 2016 (ending March 2017) to 4.2% in fiscal 2019. Moody's expects India's real GDP to contract by 4.0% in fiscal 2020 due to the shock from the coronavirus pandemic and related lockdown measures, followed by 8.7% growth in fiscal 2021 and closer to 6.0% thereafter. Thereafter and over the longer term, growth rates are likely to be materially lower than in the past, due to persistent weak private sector investment,tepid job creation and an impaired financial system.Moody's Investors Service

Debt Burden To Be Higher Than Expected

Lower real and nominal GDP growth over the medium term will mean that the Indian government will find it tougher to reduce its debt burden, after a significant rise as a result of the coronavirus economic shock.

Prior to the pandemic, India's general government debt-to-GDP ratio was estimated at 72% for 2019-20. This is now likely to rise to 84% of GDP this year, Moody's said. “While it should stabilise at that point, it is unlikely to fall materially thereafter.”

India's debt-to-GDP ratio has always been higher than similarly-rated peer countries. Moody's, in its release said that India's debt-to-GDP ratio was 30 percentage points higher than the ‘Baa median'.

Although large private sector savings and long government debt maturities provide some stability and resilience to shocks to the cost of debt, interest payments comprised about 23% of general government revenue, the highest interest burden among Baa-rated peers and around three times the Baa median.Moody's Investors Service

Reacting To Moody's Downgrade

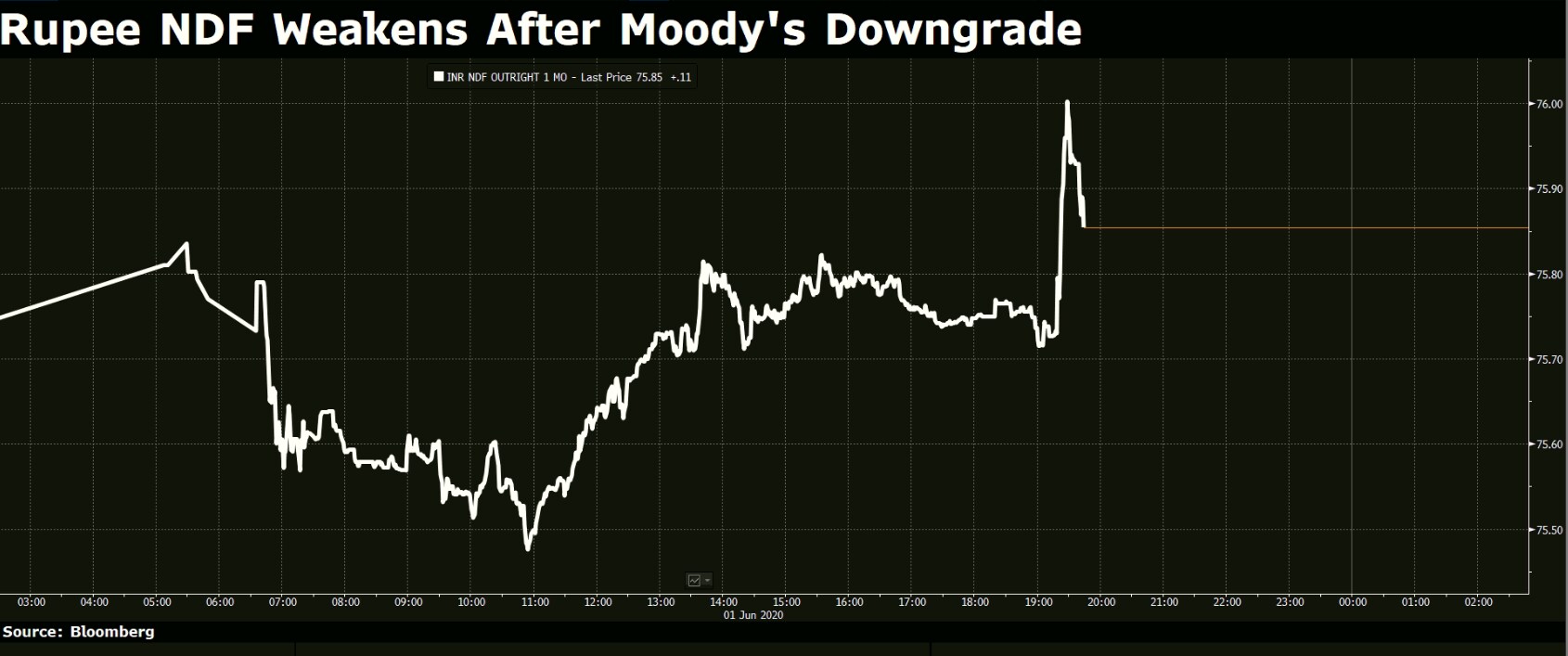

The sovereign rating downgrade by Moody's may not be a significant negative surprise for the Indian currency and debt markets.

In the minutes soon after the downgrade was announced, the rupee weakened in the non-deliverable forwards market. The local currency market may not see a sharp reaction when it reopens on Tuesday, said K Harihar, treasurer at First Rand Bank.

“The market had been expecting this downgrade for a while since the other two major agencies already have a Baa3 rating for India. Only Moody's had a higher rating, so we this as an expected adjustment. We do not expect any major movement in the bond or rupee market since India still retains an investment grade rating,” said Harihar.

In the bond markets, some impact could be seen on longer term yields, said Ajay Manglunia, head of institutional fixed income at JM Financial Products.

“The currency has not been under too much pressure, although on the bond side we could see some reversal of yields, which were falling in the recent weeks, in the immediate future but it will recover in time,” said Manglunia. Long term bond yields could edge higher by 10 to 15 basis points, he added.

However, what may remain a concern is the negative outlook that Moody's has maintained on India's rating. This could leave India open to another downgrade, which would take it down into junk territory.

“The negative outlook despite the rating downgrade could mean that if over the next 18 months, the rating agencies do not see signs of India's growth back to a sustainable 6.0-7.0% growth level, we risk being downgraded to Junk,” said Arvind Chari, head of fixed income at Quantum Advisors.

Moody's tends to be more “nimble” in changing ratings on the upside and downside, said Abheek Barua, chief economist at HDFC Bank. Apart from the short term view on the economy, there is a rationale for a downgrade even from a longer term viewpoint, said Barua.

“If one does not take the longer term view of the economy, there is a rational for a ratings downgrade and a negative outlook. There could be a change in outlook by the other agencies too but S&P has so far has created some leeway for India by appreciating and understanding the challenges in the Indian economy,” Barua said.

The ratings downgrade was not entirely surprising as it now takes the ratings to at par with those assigned by other ratings agencies, said Sameer Narang, chief economist at Bank of Baroda. “However, their assessment of the economic situation has made them continue with a negative outlook. Fiscal deficit expanded at 4.6 percent in the last fiscal year, materially higher than anticipated. Other ratings agencies may also consider changing their outlook to negative,” Narang said.

(Corrects an earlier version that misstated Sameer Narang's first name.)

Essential Business Intelligence, Continuous LIVE TV, Sharp Market Insights, Practical Personal Finance Advice and Latest Stories — On NDTV Profit.